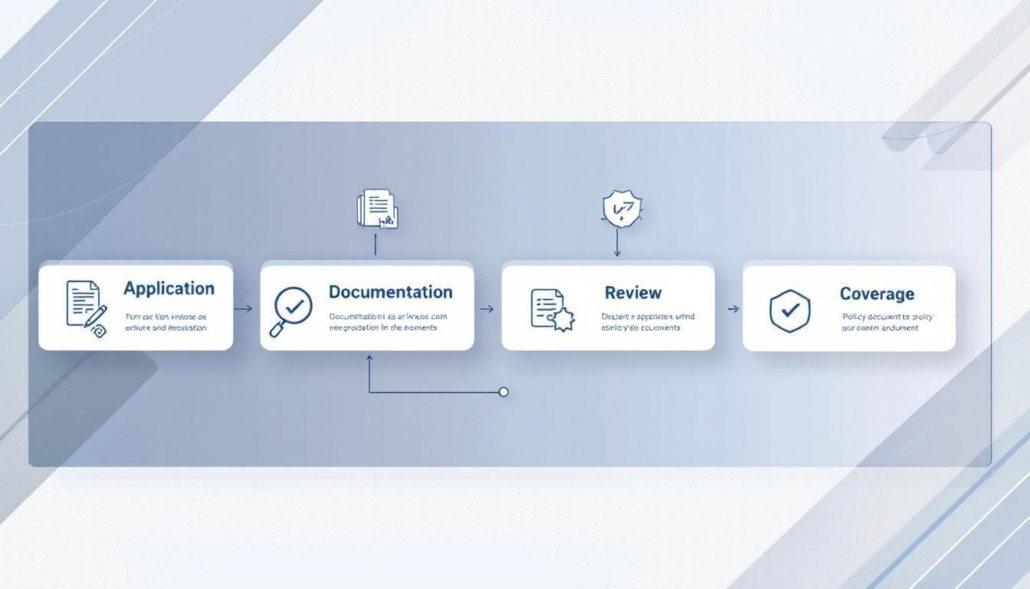

Boat Insurance Filing Steps: From Application to Coverage

Getting boat insurance right takes more than just signing paperwork. The boat insurance filing steps matter because mistakes early on can cost you later-either through gaps in coverage or overpaying for protection you don’t need.

At North Point Insurance Group, we’ve helped countless boat owners navigate this process smoothly. This guide walks you through each stage, from gathering your boat details to understanding your final policy.

Gathering Your Boat Information and Documentation

What You Need to Collect Before You Apply

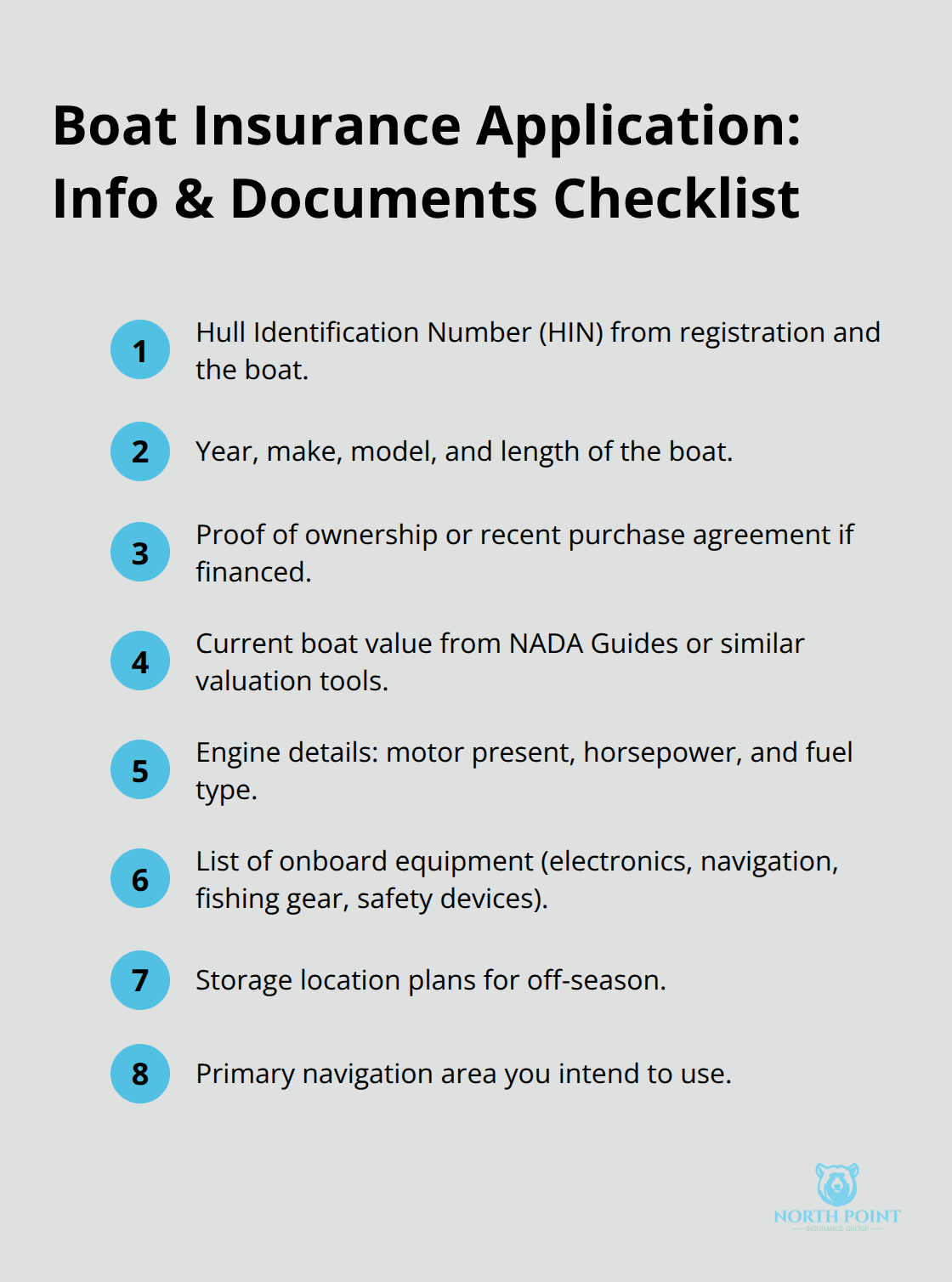

Starting your boat insurance application requires you to collect the right information upfront, which saves time and prevents coverage gaps later. You’ll need your boat’s hull identification number (HIN), which appears on the registration and the boat itself, along with the year, make, model, and length. If you financed the boat, lenders require proof of ownership or a recent purchase agreement, so have that ready.

The insurer will also want to know the boat’s current value, which you can find through NADA Guides or similar marine valuation tools, and whether it has a motor, how many horsepower, and what fuel type it uses.

Equipment adds significant value to your boat and affects your coverage. List any electronics, navigation systems, fishing gear, or safety devices you have onboard, since these items increase your boat’s total insured value and may qualify for separate coverage or discounts.

How Your Boating Habits Shape Your Coverage and Cost

Your boating habits directly shape which coverages you actually need and what you’ll pay. If you operate the boat only within 50 miles of a protected home port, your premium will be lower than if you plan coastal navigation across multiple states. The more days per year you spend on the water, the higher your risk profile-insurers typically ask whether you boat seasonally, monthly, or year-round.

Your experience matters significantly to underwriters. They want to know how many years you’ve been boating, whether you’ve completed a boating safety course, and if you have any prior claims or accidents. If other people regularly operate your boat, disclose that, since some carriers charge more if multiple operators are involved or if you plan to rent the boat out.

Location and Storage Decisions That Affect Your Premium

Geographic location plays a substantial role in your premium. Boats moored in hurricane-prone areas or high-theft regions typically cost more to insure. Be straightforward about where you store the boat during off-season months, whether that’s in the water, on a trailer at home, or at a marina, because storage conditions affect risk assessment and your premium.

The more honest and detailed you are about your actual usage patterns, the more accurate your quote will be and the fewer surprises you’ll face when a claim arises. With your boat information and usage patterns documented, you’re ready to move forward with the application itself.

Completing Your Application Accurately

Answer Every Question Completely and Honestly

The application form is where vague answers create real problems down the road. Insurers ask detailed questions about your boat, experience, and usage patterns specifically because they need accurate information to calculate risk and price your coverage fairly. When you rush through the form or provide approximate answers, you set yourself up for claim denials or coverage disputes later. Take time to answer every question completely and honestly, even if some questions seem repetitive or overly specific.

If a question asks about the number of days you boat annually, pull up your boating logs or calendar to give a real number instead of estimating. If you’re unsure what a question means, contact your agent for clarification rather than guessing. Insurers compare your application answers against claim documentation, and inconsistencies between what you stated during application and what they discover during claims investigation can result in coverage being denied or reduced.

Organize Your Information Before You Start

The application process typically takes 15 to 30 minutes if you have your information organized, so the upfront investment in accuracy pays dividends later. Gather your boat’s registration, proof of ownership or the purchase agreement, and recent photos of the hull and interior showing the boat’s condition before you sit down to complete the form. This preparation prevents you from leaving questions blank or providing incomplete answers while you search for details.

Strengthen Your Application With Supporting Documentation

Submitting supporting documentation strengthens your application and speeds up approval. Include documentation of any safety equipment installed, such as fire extinguishers or GPS systems, since these items demonstrate responsible boat ownership. If you completed a boating safety course through the U.S. Coast Guard or a similar organization, include your certificate, as many insurers offer premium discounts for safety training.

Photos matter more than you might think-clear images of your boat from multiple angles help the underwriter assess condition and value without requiring an in-person inspection for smaller vessels. Have your HIN visible in at least one photo. If your boat has recent upgrades or equipment additions, provide receipts or invoices showing what was installed and when, since these details affect your boat’s current value and may qualify for additional coverage or discounts.

Documentation Reduces Processing Time and Accelerates Coverage

The stronger your documentation package, the faster underwriters issue your policy and move you toward active coverage. Having documentation ready when you file reduces processing time significantly. This organized approach means you move quickly from application submission to understanding your actual coverage details and policy terms.

Understanding Your Coverage and Policy Details

Your policy document contains specific language that determines what gets paid and what doesn’t, so reading it thoroughly before claims arise matters far more than most boat owners realize. You should focus on three core sections: physical damage coverage (which pays for repairs or replacement of your hull, engine, and onboard equipment), liability coverage (which protects you if you injure someone or damage their property), and medical payments coverage (which covers injuries to you and your passengers).

Physical Damage Settlement Options Shape Your Payout

Physical damage comes in two settlement options-Agreed Value, which pays replacement cost for a total loss without depreciation, or Actual Cash Value, which pays the fair market value of your boat at the time of the loss. Agreed Value costs more upfront but protects you better when your boat is newer or has recent upgrades. The difference matters significantly: on a $100,000 boat with a total loss, ACV might pay $75,000 after depreciation, while Agreed Value pays the full $100,000 minus your deductible.

Deductibles Directly Affect Your Premium and Out-of-Pocket Costs

Your deductible directly affects your premium-raising it from $500 to $2,500 can reduce your annual cost by 15% to 25%, though you need to confirm you can actually afford that out-of-pocket amount if a loss occurs. Deductibles vary by loss type as well: standard deductibles apply to most claims, but theft or lightning losses often carry separate deductibles of 5% to 10% of your hull value. Named storm deductibles typically run 10% of hull value, meaning a $200,000 boat could involve a $20,000 deductible for hurricane damage.

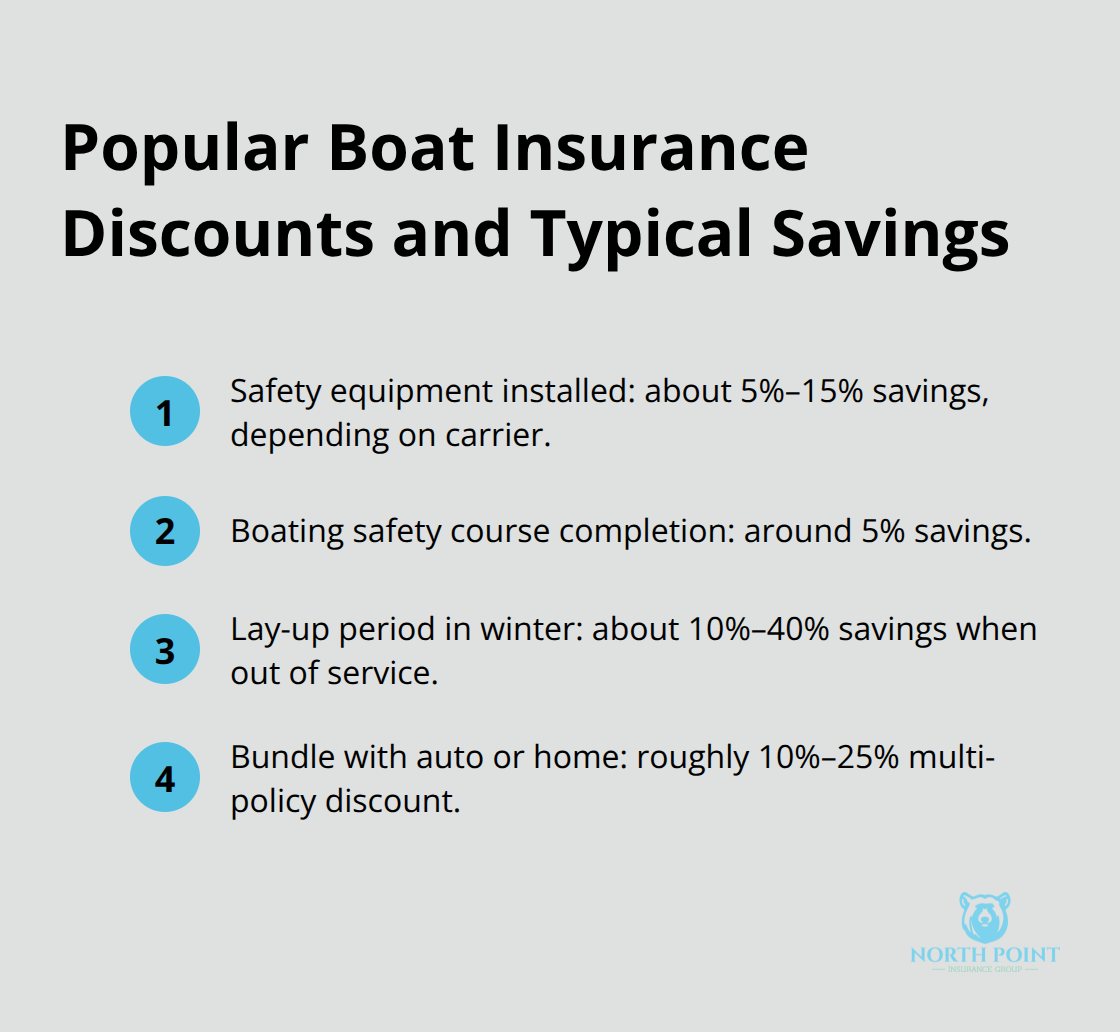

Discounts Require You to Ask Your Agent Directly

Discounts exist across most carriers, but you have to ask for them or they won’t appear on your quote. Safety equipment discounts apply if you have automatic fire extinguishers, GPS systems, or anti-theft devices installed-these can lower your premium 5% to 15% depending on the carrier. Boating safety course completion typically earns a 5% discount, and lay-up discounts apply when your boat sits out of service for extended periods, sometimes reducing premiums by 10% to 40% during winter months.

Bundling your boat policy with auto or home coverage through the same carrier usually qualifies for a multi-policy discount of 10% to 25%.

Navigation Area and Additional Endorsements Impact Your Rate and Coverage

Geographic restrictions also affect your rate: narrowing your navigation area to where you actually boat rather than insuring statewide coverage lowers your premium substantially. Before your policy activates, ask your agent explicitly which discounts apply to your specific situation and whether additional endorsements-like personal property coverage for onboard belongings or emergency towing and assistance-make sense for your boating style. The answers you receive will shape both what you pay and what you’re actually protected for when something goes wrong.

Final Thoughts

You’ve now walked through the complete boat insurance filing steps, from gathering your boat’s details to understanding the specific coverages and deductibles that protect you on the water. The application process itself is straightforward when you prepare properly, but the real value comes from taking time to answer questions accurately and organizing your documentation before you submit. Rushing through this stage creates problems later, whether that’s claim denials, coverage gaps, or disputes about what your policy actually covers.

Once your policy activates, review your policy document within the first week to confirm all the details match what you discussed with your agent. Check that your boat’s value is correctly stated, your deductibles are what you agreed to, and your coverage limits align with your actual boating habits. If you notice any discrepancies, contact your agent immediately to request corrections before a claim arises, and keep your documentation organized and accessible in a secure location (either digitally or in a physical file).

If you make upgrades or add equipment to your boat, notify your agent so your coverage stays current with your boat’s actual value. This ongoing communication prevents underinsurance and helps claims move faster if something happens. Contact North Point Insurance Group today to discuss your boat insurance needs and get a quote tailored to your situation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.