What Affects Auto Premiums: Key Drivers to Know

Your auto insurance premium isn’t random. It’s calculated based on specific factors that insurers measure and weigh differently.

At North Point Insurance Group, we’ve seen firsthand how small details-from your age to where you park at night-shift your rate up or down. Understanding what affects auto premiums helps you spot opportunities to pay less and make smarter coverage choices.

Demographic and Personal Factors That Impact Your Rate

Age and Driving Experience

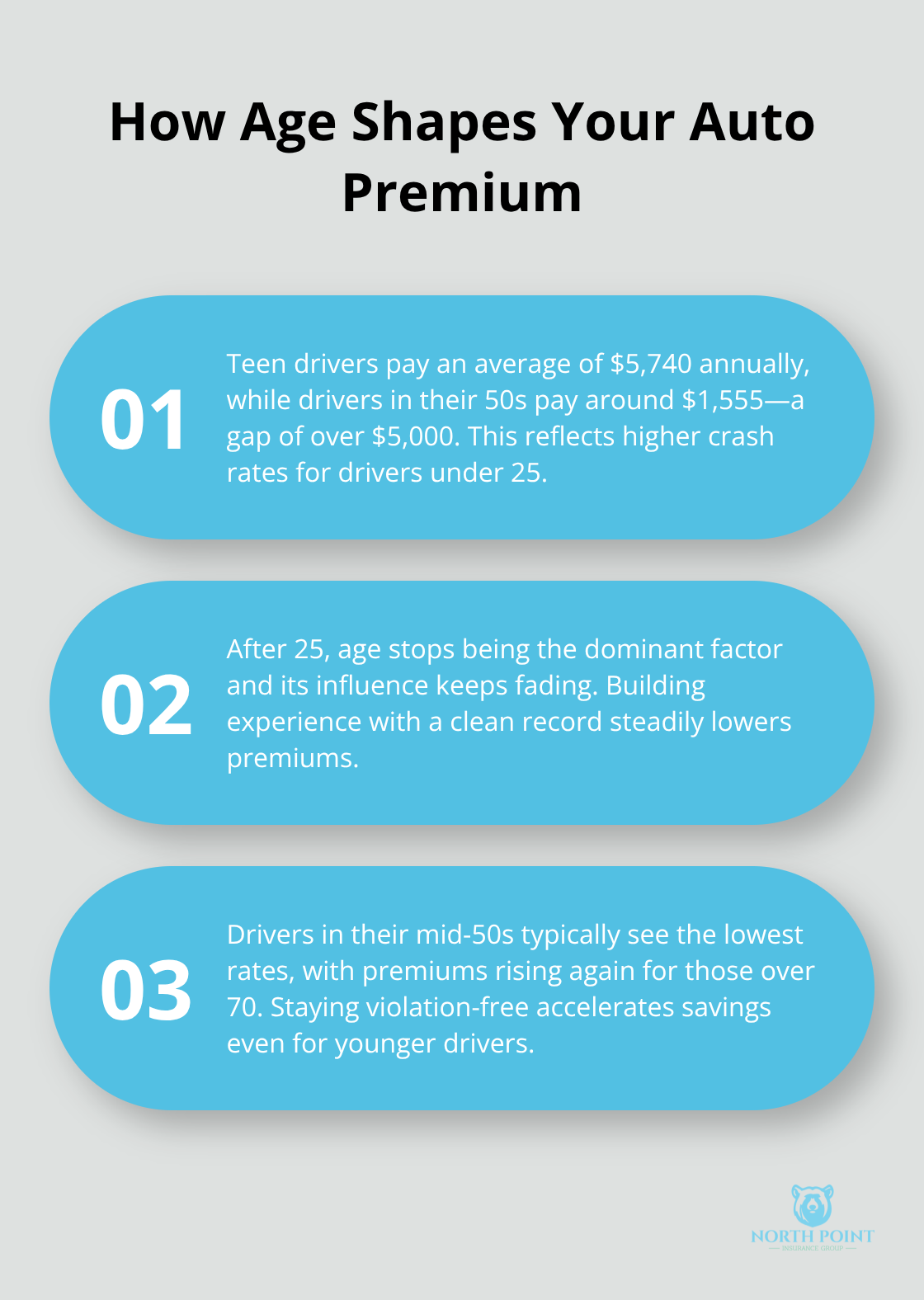

Age stands as one of the most powerful predictors of your auto insurance premium. Teen drivers pay an average of $5,740 annually, while drivers in their 50s pay around $1,555-a gap exceeding $5,000 per year. This dramatic difference reflects real accident data: drivers under 25 have substantially higher crash rates. However, age stops being the dominant factor after 25, and its influence continues to fade. Drivers in their mid-50s typically see their lowest rates before premiums climb again for those over 70. If you’re young, your age alone doesn’t lock you into high rates forever. A clean driving record in your early years becomes your fastest path to lower premiums as you gain experience.

Credit Score and Financial History

Your credit score matters far more than many drivers realize. Poor credit versus excellent credit can add over $1,500 annually to your premium, making it one of the heaviest financial levers insurers pull. However, not every state allows insurers to use credit scores-California, Hawaii, and Massachusetts restrict or ban the practice entirely. If you live in a state where credit scoring applies, improving your credit profile directly improves your insurance costs. Check your credit report for errors through major bureaus, dispute any inaccuracies, and focus on paying bills on time and reducing outstanding debt.

Marital Status and Household Composition

Marital status and household composition play secondary roles compared to age and credit, but they can still influence your rate. Some insurers offer slight discounts for married drivers or households with multiple vehicles on one policy. The real opportunity lies in bundling: combining your auto policy with home or renters insurance often yields meaningful savings that dwarf any marital-status adjustments. When shopping for coverage, ask about multi-policy discounts explicitly, as they frequently represent the largest savings available to you. Your vehicle choice and driving habits interact with these personal factors to shape your final premium.

Driving Record and Vehicle Characteristics

How Your Driving Record Shapes Your Premium

Your driving record is the single most actionable factor you control. A ticket, at-fault accident, or DUI doesn’t just add a few dollars-it restructures your entire premium. According to the Insurance Information Institute, six months with no violations costs around $1,103 annually, but a DUI jumps that to $2,133, and an at-fault accident lands you at $3,836 annually. Most insurers look back three years when pricing, meaning violations older than that typically stop hurting you. One bad decision on the road can cost you an extra $1,000 per year for years.

If you’ve had violations, your fastest path to lower rates is time and a clean record going forward. Some insurers offer accident forgiveness programs that prevent a single at-fault claim from raising your premium, though these usually apply only to first incidents or require you to maintain clean driving for a set period.

The Vehicle You Drive and Its Safety Features

The vehicle you drive matters as much as how you drive it. A luxury sedan or sports car costs substantially more to insure than a used Honda Civic because repair and replacement costs are higher, and insurers factor in those expenses directly into your premium. Safety features and theft risk also shift your rate significantly. The Insurance Institute for Highway Safety tracks which vehicles cost less to insure based on repair costs, safety performance, and theft data-checking this before you buy a car reveals the true insurance cost of ownership.

Annual Mileage and Parking Location

Annual mileage acts as a powerful lever on your premium. Drivers logging under 7,500 miles annually pay roughly $10 per month less than those driving 15,000 miles or more, according to The Zebra’s rate analysis. Low-mileage discounts exist specifically because less time on the road means lower accident exposure. If you commute short distances or work from home, that behavior directly justifies a lower premium.

Where you park also matters-keeping your car in a secured garage or off-street location reduces theft risk and can lower your comprehensive coverage costs. This simple choice protects your vehicle and your wallet. Your location and the coverage choices you make next determine whether you pay more or less than your neighbors for the same driving habits.

Location, Coverage Choices, and Discounts Shape Your Premium

Where You Live Affects Your Rate

Your ZIP code determines far more about your rate than you might think. Michigan drivers pay around $193 monthly due to no-fault personal injury protection requirements, while Alabama drivers average $149 for identical coverage-a $528 annual gap driven purely by state regulation and local risk factors. Urban areas with higher traffic density, theft rates, and medical costs push premiums upward compared to rural regions. Even within the same city, your neighborhood’s accident frequency and claim history influence pricing. Before moving or buying a home, check insurance costs for that ZIP code; it’s one of the few factors you can anticipate before committing.

How Deductibles and Coverage Limits Control Your Cost

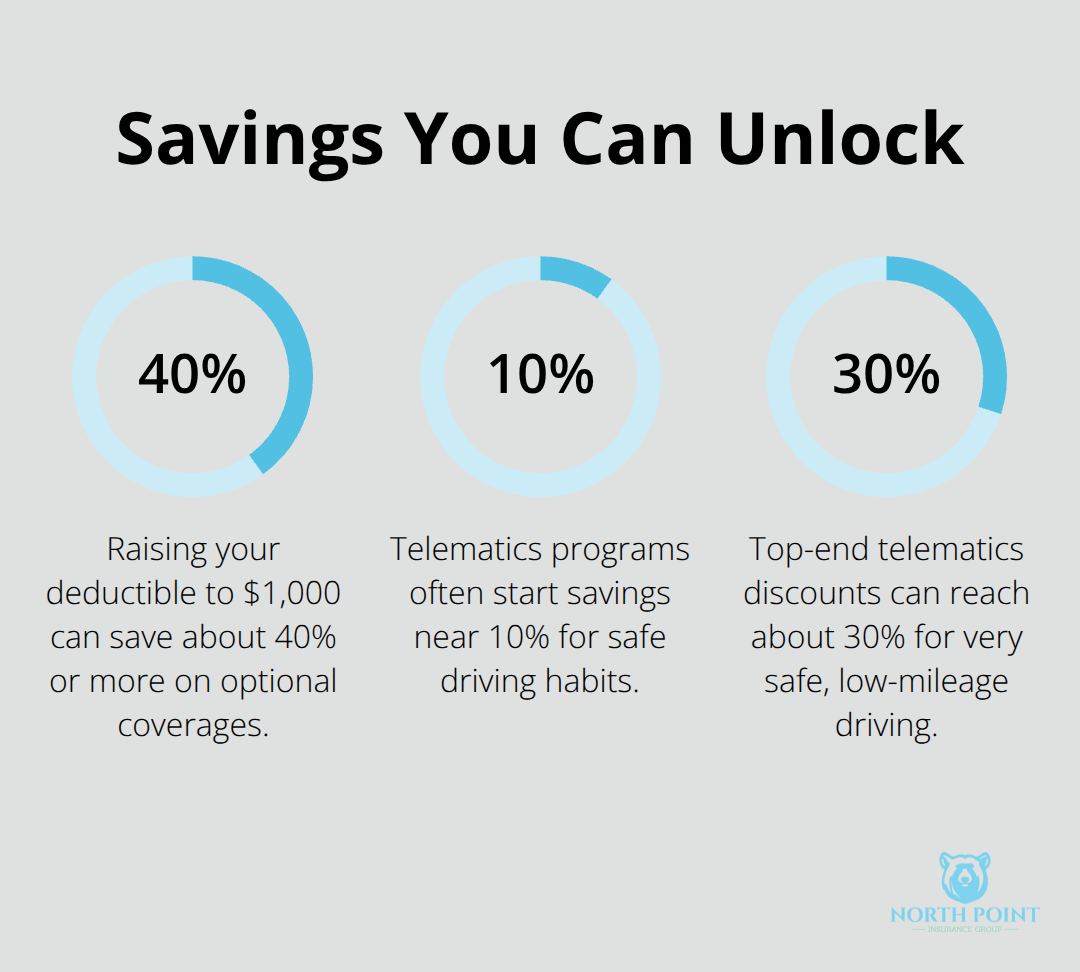

If you’re already locked into an expensive location, your coverage choices become your lever for cost control. Increasing your deductible from $200 to $500 can reduce optional collision and comprehensive coverage premium costs, while jumping to a $1,000 deductible can save 40 percent or more. The math is straightforward: higher deductibles mean you pay more out-of-pocket after a claim, but lower monthly premiums. For older vehicles worth less than $4,000, dropping collision and comprehensive entirely often makes financial sense-your monthly savings exceed what you’d recover in a claim.

Liability-only coverage runs roughly $50 monthly versus $129 for full coverage with a $1,000 deductible, giving you concrete numbers to evaluate your actual risk tolerance.

Discounts That Actually Reduce Your Premium

Discounts represent the final lever most drivers ignore entirely. Bundling auto with home or renters insurance typically saves more than any other discount available-sometimes hundreds annually. Multi-car policies, good driver discounts for three years without violations, paperless billing, and paying your premium in full upfront all stack meaningful savings. Telematics programs like Progressive Snapshot or State Farm Drive Safe & Save track your actual driving habits and reward safe behavior with discounts ranging from 10 to 30 percent; these programs benefit low-mileage drivers and careful drivers most dramatically. Good student discounts apply if you maintain a 3.0 GPA or higher, defensive driving course completion removes a violation from your record in many states, and some insurers offer group discounts through employers or professional associations you already belong to.

Shopping Around Reveals Your True Savings

The critical insight: the final premium matters far more than the number of discounts. One insurer might advertise ten discounts but still charge more than a competitor offering three. Compare actual quotes across at least three carriers rather than chasing discount names. Your state insurance department publishes complaint data for each insurer-checking this reveals which companies follow through on promises versus those that disappoint. Shopping around every two to three years catches rate increases before they compound and uncovers new discounts as your life changes.

Final Thoughts

Your auto insurance premium reflects a combination of factors working together-your age, driving record, location, vehicle choice, and coverage decisions all matter. What affects auto premiums most heavily are the elements you control: maintaining a clean driving record, selecting appropriate deductibles, and bundling policies when possible. Age and location shape your baseline rate, but your actions determine whether you pay more or less than necessary within that framework.

Shopping around every two to three years is non-negotiable because rates shift as your risk profile changes and insurers adjust their pricing strategies. Comparing quotes from at least three carriers reveals gaps that loyalty masks, with one company’s $129 monthly premium potentially costing $336 more annually than a competitor offering identical coverage. Your state insurance department publishes complaint data for each insurer, giving you insight into which carriers deliver on their promises versus those that frustrate customers.

At North Point Insurance Group, our agents shop 20+ carriers to find coverage that matches your specific situation and budget. We tailor solutions that reflect what actually affects your premiums and your wallet without the call-center experience. Visit North Point Insurance Group to discuss your coverage today.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.