Umbrella Policy Benefits: What They Do for Your Protection

Your homeowner’s insurance and auto policy have limits. When a lawsuit exceeds those limits, your personal assets are at risk.

An umbrella policy bridges that gap by providing additional liability coverage beyond what your standard policies offer. At North Point Insurance Group, we’ve seen how umbrella policy benefits protect families and business owners from catastrophic financial loss. This guide walks you through how umbrella coverage works and whether you need it.

How Umbrella Policies Work

An umbrella policy sits on top of your existing auto, home, and other liability policies and activates only after those policies hit their limits. Think of it as a second line of defense. Your homeowners policy covers up to $300,000 in liability. Your auto policy covers up to $250,000. A single serious accident or lawsuit can easily exceed both. That’s where the umbrella kicks in, covering the remaining damages up to its limit, often $1 million or more.

The reality is that a severe car accident resulting in multiple injuries can generate settlements well beyond typical policy limits. According to data from the Insurance Information Institute, average bodily injury claims reached $28,278 in 2024, while property damage claims averaged $6,770. These trends make umbrella coverage less of a luxury and more of a practical necessity for protecting your assets.

What Umbrella Coverage Actually Protects

Umbrella policies cover a wider range of liabilities than many people realize. Beyond standard bodily injury and property damage from accidents, they protect you against defamation claims, false arrest accusations, and invasion of privacy lawsuits. If someone is injured on your property, at an event you host, or in a situation where you’re found liable, the umbrella steps in after your homeowners or other primary coverage is exhausted.

The coverage extends to your entire household, so injuries involving your children or guests are included. One important point: umbrella policies require you to maintain minimum underlying coverage before activation. Most insurers require at least $250,000 in auto bodily injury limits and $300,000 in homeowners liability before they’ll write an umbrella. This requirement isn’t arbitrary-it protects you at the base level before the umbrella takes over.

Cost and Coverage Limits Make Sense

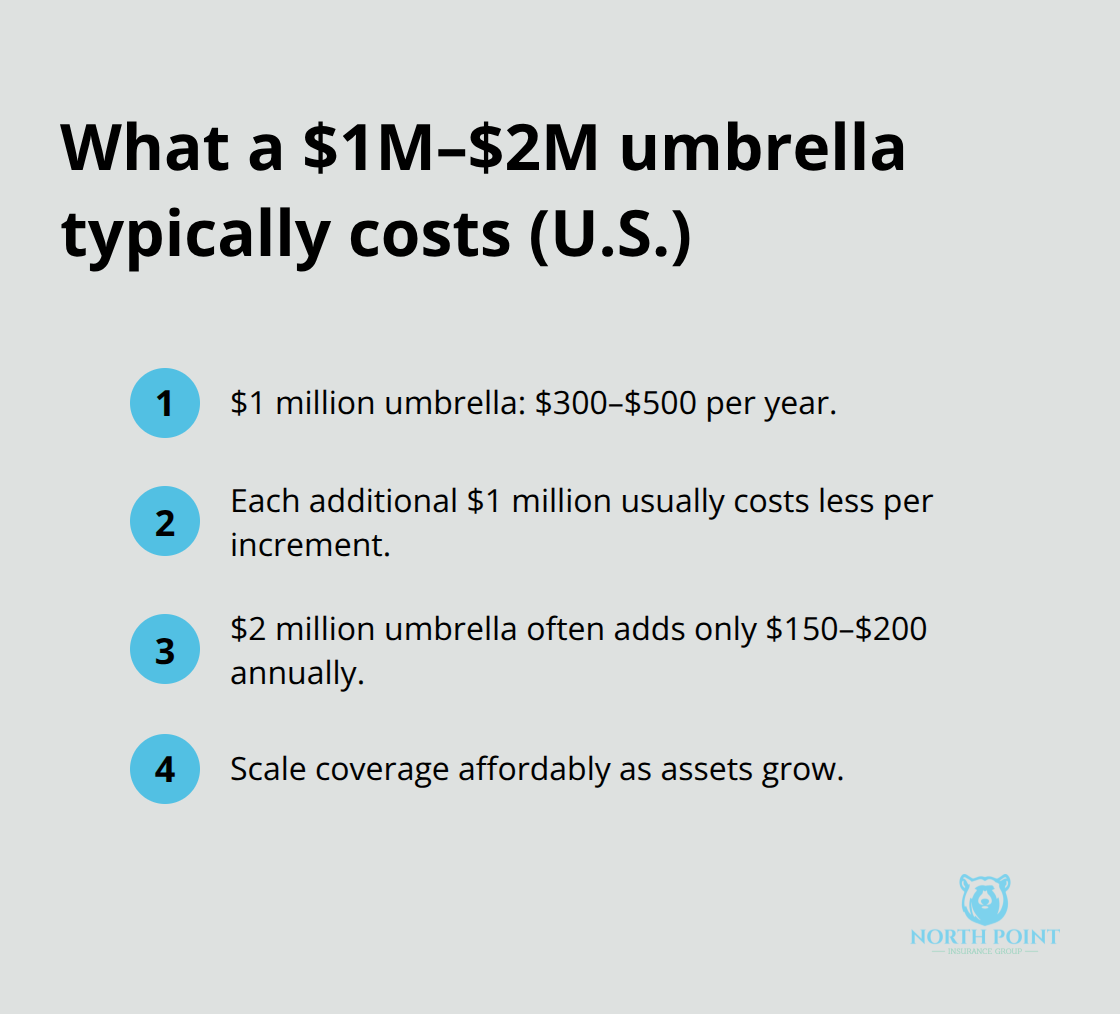

The affordability of umbrella coverage surprises most people. A $1 million umbrella policy typically costs between $300 and $500 per year, making it one of the cheapest forms of comprehensive protection available. Adding more coverage doesn’t scale linearly either-each additional $1 million in limits generally costs less per increment than the previous one (so a $2 million umbrella might cost only $150 to $200 more annually).

You can choose coverage amounts that match your actual assets and risk exposure. If you own a home worth $400,000 and have $200,000 in investments, a $1 million umbrella provides solid protection. If you have rental properties, multiple vehicles, or a teenage driver, you might lean toward $2 million. The goal is matching your coverage to what you actually stand to lose in a lawsuit.

Determining Your Coverage Needs

Your household’s specific situation determines how much umbrella protection you actually need. High-net-worth individuals, property owners with rental units, and families with teenage drivers face elevated liability exposure. Dog owners and those who frequently host events also benefit from the broader protection that umbrella policies provide (including social host liability and animal-related incidents).

Start by calculating your total assets-home equity, investments, retirement savings, and future earning potential all count. Then assess your risk factors: the number of vehicles you own, the ages of drivers in your household, whether you have a pool or trampoline, and your property’s condition. This honest evaluation helps you select a limit that actually protects what matters to you. Your next step is to speak with an insurance professional who can review your specific situation and recommend appropriate coverage levels.

Why Umbrella Coverage Costs Less Than You Think

Umbrella policies deliver one of the best cost-to-protection ratios in insurance. A $1 million umbrella typically costs $383 per year for comprehensive liability defense. That’s less than $1.50 per day for coverage that protects everything you own. The real advantage emerges when you add higher limits. A $2 million umbrella might cost only $450 to $700 per year, meaning that second million in protection costs roughly $150 to $200 extra. This declining cost structure makes scaling your protection genuinely affordable as your assets grow. Most households can add comprehensive liability defense for the price of a couple of restaurant dinners monthly.

What Actually Happens When a Lawsuit Exceeds Your Limits

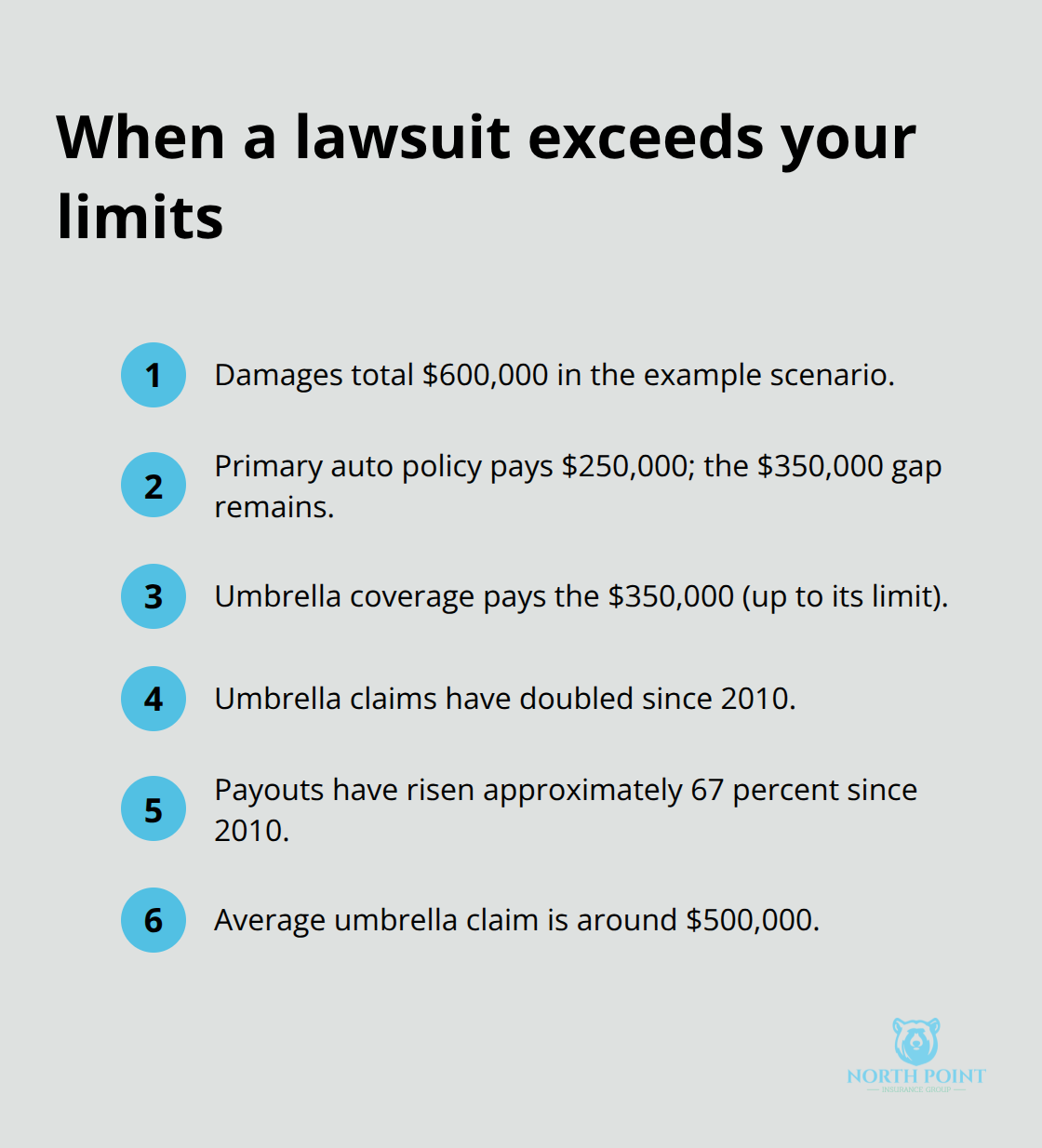

Consider a concrete scenario: a serious multi-vehicle accident where you’re found liable. Your auto policy covers $250,000 in bodily injury liability. Medical bills, lost wages, and pain-and-suffering damages total $600,000. Without umbrella coverage, you’re personally liable for the remaining $350,000. That gap comes from your savings, investment accounts, home equity, or future wages through garnishment. With umbrella coverage, the policy pays that $350,000 (up to its limit) and protects your financial future completely.

According to Safeco Insurance, umbrella claims have doubled since 2010, with payouts rising approximately 67 percent over that same period. The average umbrella claim now sits around $500,000, reflecting how quickly liability exposure spirals in today’s litigious environment.

Who Actually Needs This Protection

Umbrella coverage isn’t just for wealthy individuals, though they certainly benefit. Anyone with meaningful assets-home equity, retirement savings, investment accounts-faces real exposure. Families with teenage drivers have significantly higher accident risk. Dog owners face liability from bites or injuries. Property owners with rental units encounter tenant-related claims. People who frequently host events risk social host liability if a guest is injured. The Texas Department of Insurance notes that umbrella policies protect everyone in your household, so injuries involving your children or guests activate coverage. High-net-worth individuals particularly benefit because they have more to lose in a judgment, but the real protection matters for any household with assets worth protecting.

How Your Future Earnings Factor Into Coverage Decisions

Your assets aren’t just what you own today-they include future earning potential, which courts can garnish to satisfy judgments. Umbrella coverage prevents that outcome by covering damages before they touch your paycheck. This protection becomes especially valuable for professionals in their peak earning years. A surgeon, attorney, or business owner faces substantial wage garnishment risk if a major liability claim exceeds their primary coverage. The umbrella steps in and eliminates that threat entirely. Your next step is to assess your specific risk profile and speak with an insurance professional who can recommend appropriate coverage levels for your household’s unique situation.

Real-World Situations Where Umbrella Protects Your Assets

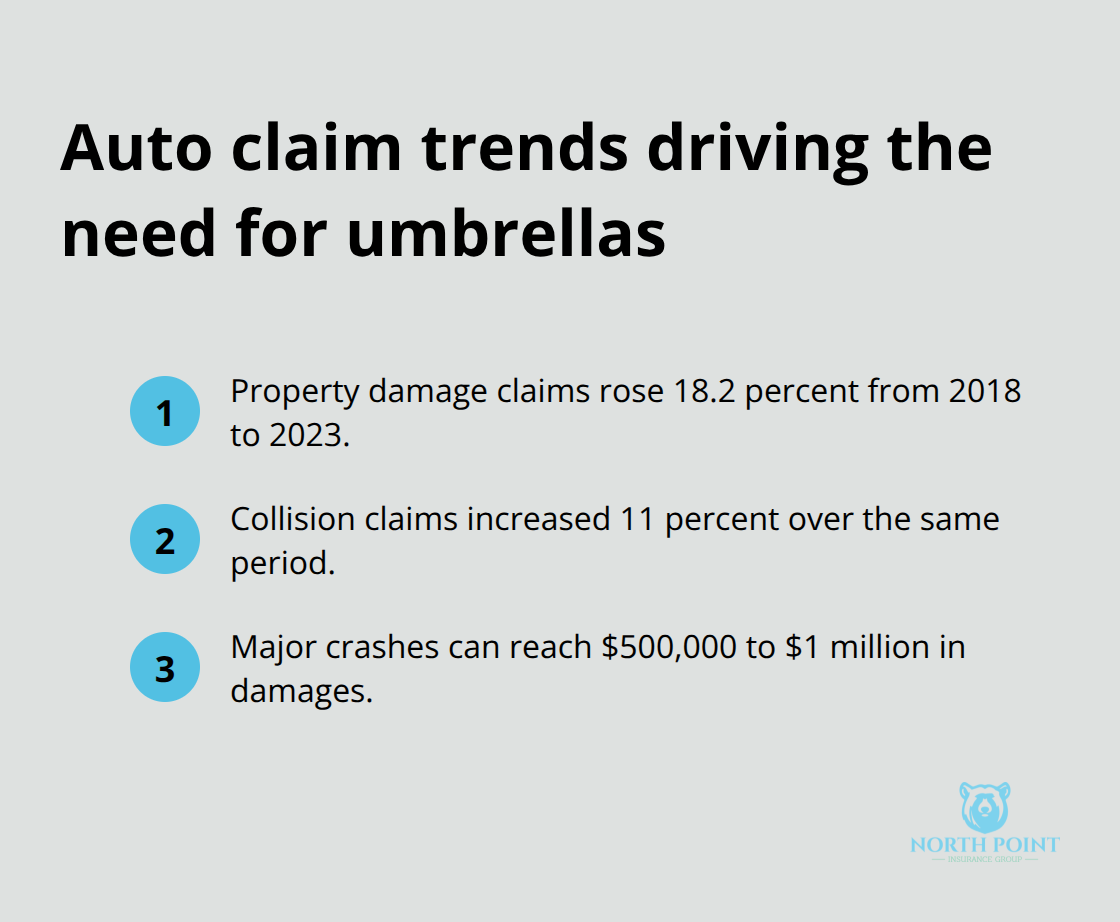

A single accident exposes everything you own. Auto crashes generate the largest share of umbrella claims, and the numbers tell a sobering story. According to the American Property Casualty Insurance Association, property damage claims rose 18.2 percent for property damage between 2018 and 2023, while collision claims increased 11 percent during that same period. A multi-vehicle collision where you’re found at fault can easily produce $500,000 to $1 million in damages when multiple people suffer serious injuries.

Your auto policy’s $250,000 limit evaporates quickly once medical bills, lost wages, and pain-and-suffering awards accumulate. The remaining liability falls directly on you. Umbrella coverage absorbs that gap, protecting your home equity, savings accounts, and future paychecks from garnishment. Without it, a single accident can force the sale of your house or drain decades of retirement savings.

When Your Home Becomes a Liability Magnet

Homeowner liability claims represent the second major category of umbrella losses. A guest slips on your icy driveway and breaks their leg. A child in your yard suffers a serious injury. Someone is injured at a party you host. These incidents create medical expenses, ongoing care costs, and legal judgments that routinely exceed your homeowners policy’s $300,000 liability limit. Property damage liability compounds the problem-a guest’s car sustains damage while parked in your driveway, or your landscaping damages a neighbor’s fence and foundation. These claims accumulate faster than most homeowners expect. Your homeowners policy covers the initial damages, but significant injuries push claims beyond those limits quickly. Umbrella coverage kicks in and pays the remainder up to its limit, which means the injured party receives full compensation without touching your assets.

Dog Bites and Pet-Related Incidents Create Substantial Exposure

Dog bite claims have become one of the fastest-growing homeowner liability exposures. A single serious bite can create $50,000 to $200,000 in medical bills, surgical costs, and reconstructive procedures, not counting legal fees and pain-and-suffering awards. Some breeds face coverage restrictions with standard homeowners policies, which means you’re already underprotected at the base level. Umbrella coverage extends protection to animal-related incidents that your homeowners policy may not fully cover or may exclude entirely. Beyond bites, dogs cause injuries through jumping, knocking someone down, or triggering falls. An elderly visitor trips over your dog and breaks their hip, creating $100,000 in medical costs and ongoing care expenses. Umbrella coverage protects you when those claims exceed your homeowners liability limit. The same protection applies to other property-related incidents on your property (a trampoline injury, pool drowning, or structural hazard that causes harm to guests or visitors). These scenarios happen regularly, and umbrella coverage ensures that one incident doesn’t destroy your financial stability.

Final Thoughts

Umbrella policy benefits extend far beyond the basic protection your auto and homeowners policies provide. A single serious accident, injury on your property, or liability claim can exceed your standard coverage limits and threaten everything you’ve built. Umbrella coverage fills that gap affordably, typically costing $300 to $500 annually for $1 million in protection-genuine financial security for less than the cost of a monthly subscription service.

The real question isn’t whether umbrella coverage is expensive; it’s whether you can afford not to have it. If you own a home, drive a vehicle, or have meaningful assets, you face liability exposure. Teenage drivers, rental properties, pools, trampolines, and frequent entertaining all increase your risk. Courts don’t care about your financial situation when awarding judgments; they award what the injured party deserves, and you’re personally liable for anything your insurance doesn’t cover.

Determining your coverage needs starts with an honest assessment of what you stand to lose. Calculate your home equity, investments, retirement savings, and future earning potential, then evaluate your specific risk factors. Contact North Point Insurance Group to discuss your umbrella coverage options with an agent who takes time to understand your situation and recommend appropriate protection levels for your family’s financial security.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.