Renters Home Insurance Basics: Protecting Your Space

Renting gives you flexibility, but it doesn’t protect your belongings. A fire, theft, or accident can wipe out your personal items and leave you facing serious financial consequences.

At North Point Insurance Group, we help renters understand the basics of renters home insurance and why it matters. This guide walks you through what coverage actually protects you, why it’s affordable, and how to pick the right policy for your situation.

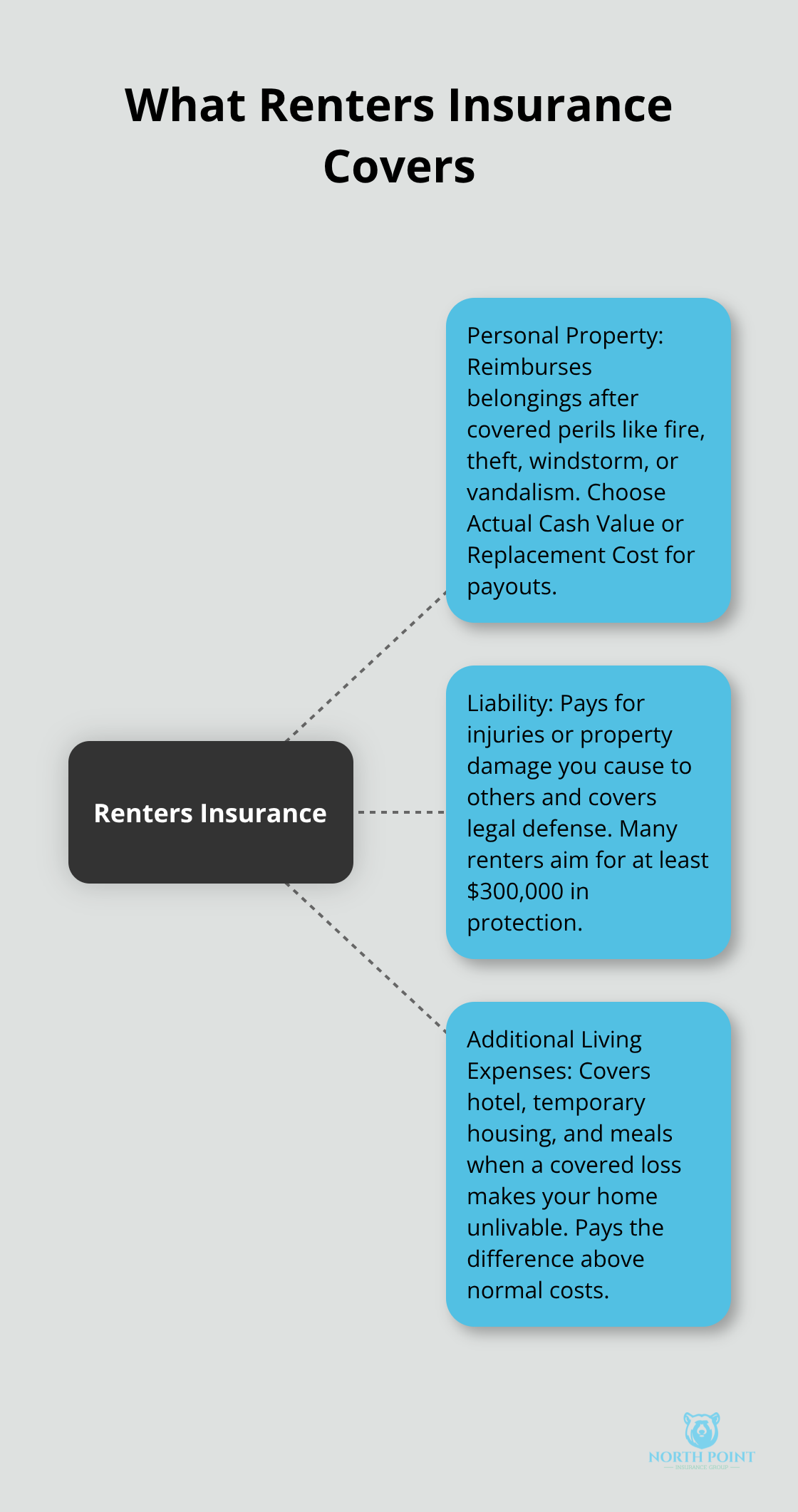

What Your Renters Policy Actually Covers

Renters insurance protects three distinct areas of your life, and understanding each one matters because they work together to keep you financially safe. Personal property coverage reimburses you for belongings damaged or stolen due to covered events like fire, theft, windstorm, or vandalism. According to the Insurance Information Institute, standard renters policies cover these common perils, but floods and earthquakes are not included by default and require separate coverage. When you file a claim, you’ll choose between Actual Cash Value, which pays depreciated amounts, or Replacement Cost, which covers the full expense to replace items new. Replacement Cost costs roughly 10% more annually but protects you from depreciation losses-a worthwhile difference if you own electronics, furniture, or appliances that lose value quickly. Most renters carry coverage between $20,000 and $40,000 depending on unit size and belongings value, though larger homes or high-value item collections may need $40,000 to $60,000 or more.

Why Liability Protection Matters More Than You Think

Liability coverage pays for injuries or property damage you or your family cause to others, including damage from your pets, and it covers your legal defense costs if someone sues. Starting liability limits sit around $100,000, but the Insurance Information Institute recommends trying for at least $300,000 in protection. This isn’t theoretical-a single serious injury in your apartment, a guest’s fall on your stairs, or your dog biting a neighbor can trigger medical bills and legal expenses that exceed basic coverage. If $300,000 feels insufficient for your situation, umbrella policies add $1 million in extra liability protection for $200 to $350 annually.

Additional Living Expenses Keep You Afloat

The third component, Additional Living Expenses, covers hotel stays, temporary housing, and meal costs when a covered disaster makes your apartment unlivable. This coverage pays the difference between your extra expenses and normal living costs, helping you avoid financial strain while your rental is being repaired or rebuilt. These three protections work as your safety net against the specific financial threats renters face daily. Now that you understand what coverage protects you, the next step is recognizing why renters insurance matters so much-especially when it costs far less than most people expect.

Why Renters Insurance Costs Far Less Than You Think

The Real Monthly Price Tag

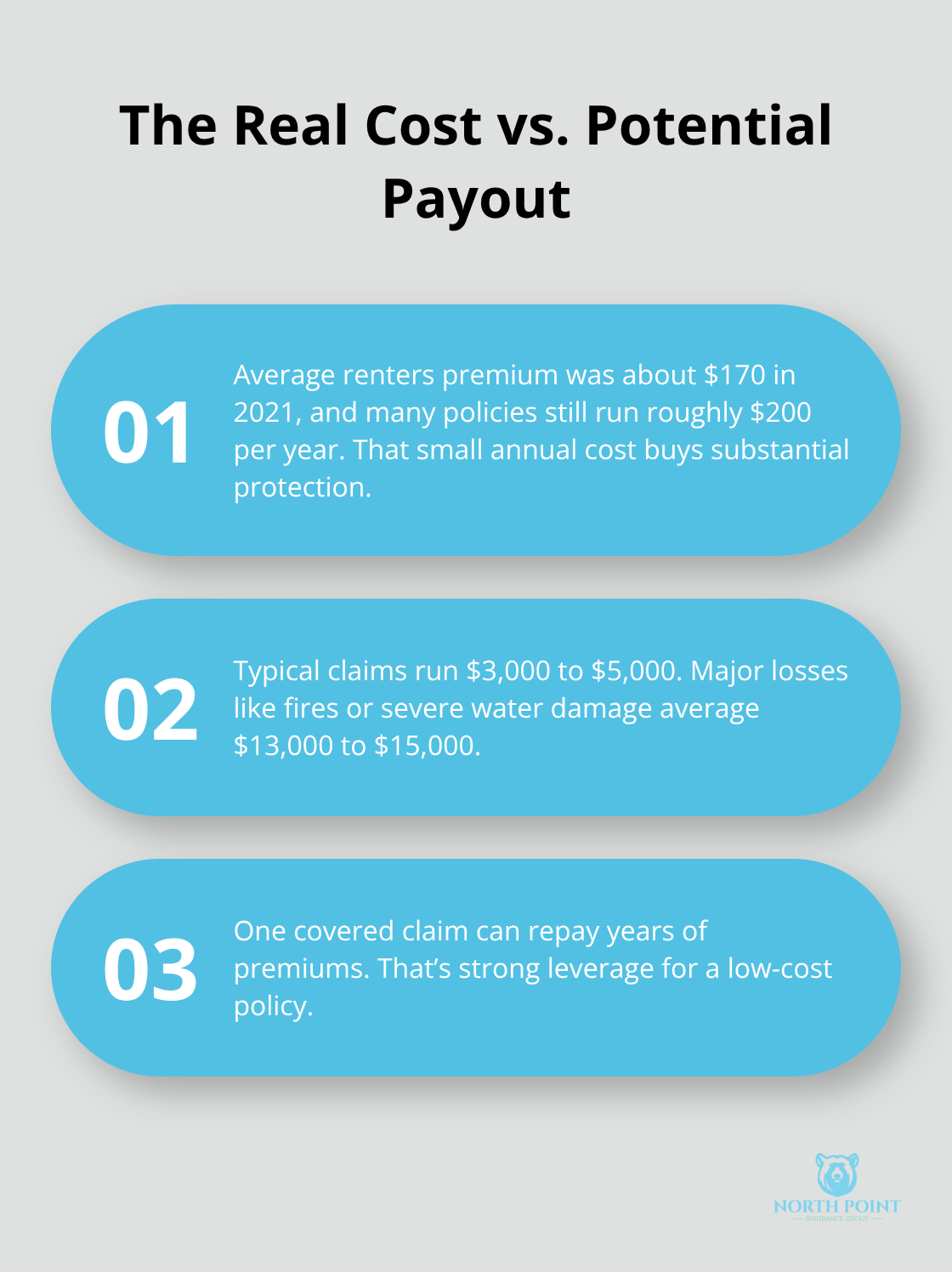

The average premiums for renters insurance in 2021 was $170 annually, making it one of the most affordable ways to protect yourself from financial disaster. Most people spend more on coffee in a month than on renters insurance annually. For roughly $200 per year, you cover personal property worth $20,000 to $40,000, liability protection starting at $100,000, and additional living expenses if your apartment becomes unlivable. That’s not theoretical math-typical renters claims run $3,000 to $5,000, with major losses like fires or severe water damage averaging $13,000 to $15,000. A single claim pays for years of premiums.

Why Half of Renters Skip Coverage

Yet roughly half of the 45.2 million renters in the United States skip this protection entirely, leaving 20 to 25 million renter households uninsured. Many landlords require renters insurance before you can move in, which means the decision isn’t always yours to make. Even when it’s not mandatory, the financial reality is stark: one theft, fire, or liability incident can cost tens of thousands of dollars out of pocket. Without coverage, you’d need an emergency fund large enough to replace everything you own plus cover legal expenses and temporary housing-a burden most renters simply don’t have.

Getting Coverage Takes Minutes

You can start a quote online with multiple carriers within minutes, and many insurers offer same-day coverage after you apply. The combination of low cost, quick setup, and protection against catastrophic loss makes renters insurance a non-negotiable part of your financial safety plan. Once you understand the true cost of being uninsured, the next step is figuring out exactly how much coverage your specific belongings and situation actually require.

How to Pick the Right Coverage for Your Situation

Start With an Honest Inventory of Your Belongings

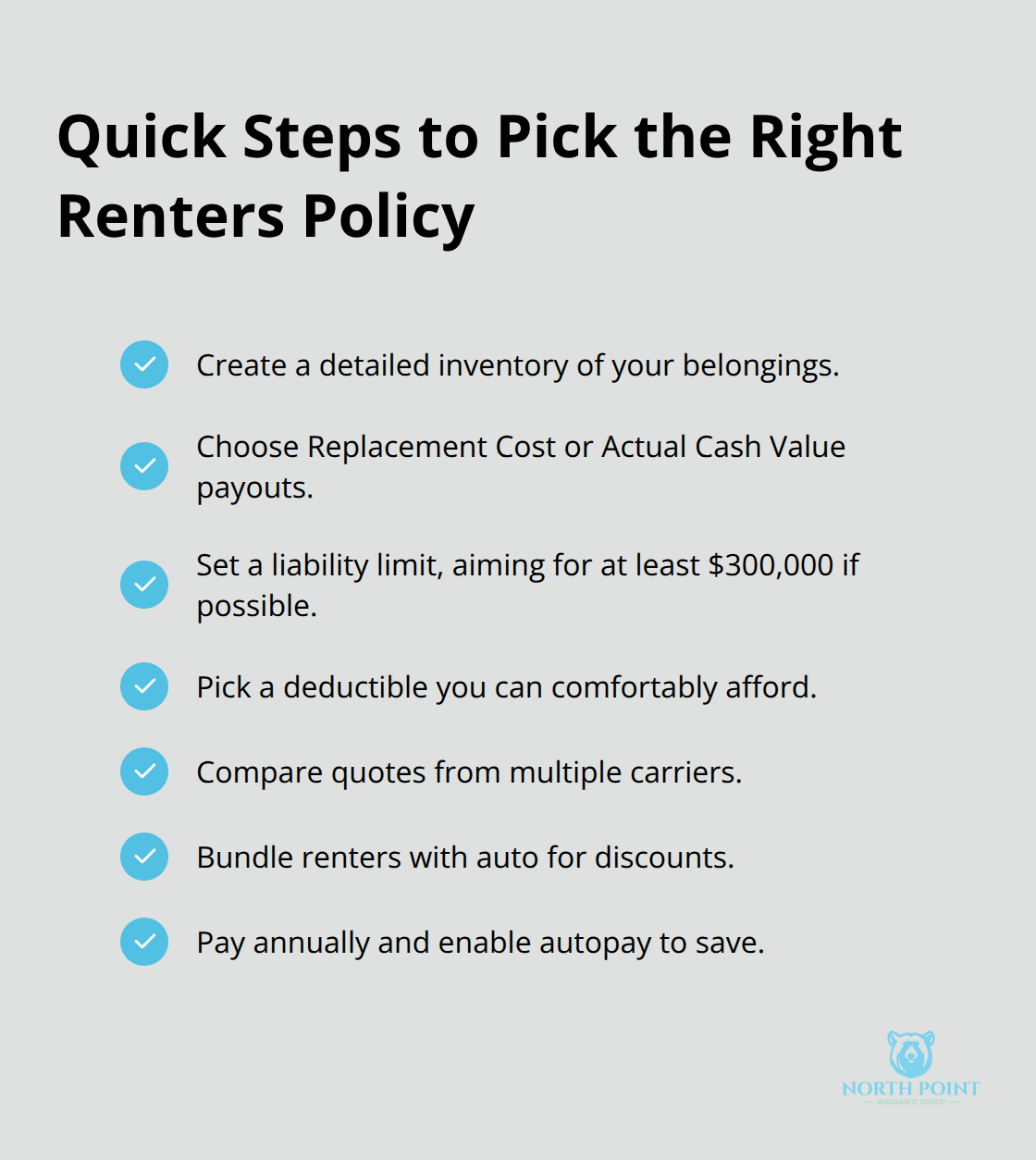

Start with an honest inventory of what you actually own. Most renters underestimate their belongings value until they sit down and list everything-furniture, electronics, clothing, kitchen items, bedding, and decor. The Insurance Information Institute offers KnowYourStuff.org, a free web-based inventory tool that makes this process simple and speeds up claims if you ever need to file one. Once you’ve inventoried your possessions, the easiest way to figure out how much personal property protection to buy is to create a detailed list of all of your personal possessions.

Choose Between Actual Cash Value and Replacement Cost

Replacement Cost coverage typically costs about 10% more annually than Actual Cash Value, but it’s worth the extra expense because you’ll receive full replacement value without depreciation deductions-especially important for electronics and furniture that lose value quickly. This choice directly affects how much you recover after a loss, so select the option that matches your financial situation and risk tolerance.

Set Your Liability Limit and Deductible

Your liability limit matters equally. Standard policies start around $100,000, but the Insurance Information Institute recommends trying for at least $300,000 to handle serious injuries or property damage lawsuits. If $300,000 feels tight for your situation, umbrella policies add $1 million in extra liability protection for just $200 to $350 per year. Deductibles directly impact your monthly premium, and selecting one requires honest assessment of your emergency savings. A higher deductible lowers your premium significantly, but only select a level you can actually afford to pay out of pocket if you file a claim-small losses below your deductible won’t be covered.

Compare Quotes From Multiple Carriers

Compare actual quotes from multiple carriers rather than relying on online estimates alone. Independent agencies can quote from 20 or more carriers, and prices vary substantially based on your specific city, the value of your belongings, your chosen limits, and your deductible.

Maximize Savings on Your Premium

Many insurers offer same-day coverage after you apply online, and bundling renters insurance with auto coverage often yields meaningful discounts. Paying your premium annually instead of monthly saves money compared to installment plans, and autopay discounts are common across carriers.

Final Thoughts

Renters home insurance basics protect three critical areas of your financial life: your belongings, your liability exposure, and your temporary housing costs if disaster strikes. You now understand what coverage actually does, why it costs less than $200 annually, and how to match your policy to your real situation. The next step is acting on this knowledge without delay.

Getting a quote takes minutes online, and you can compare rates from multiple carriers and secure same-day coverage without visiting an office. When you shop, bring your inventory list, decide between Actual Cash Value and Replacement Cost, set liability limits that reflect your actual risk (most renters benefit from at least $300,000), and choose a deductible you can genuinely afford to pay out of pocket. Bundling with auto insurance and paying annually both reduce your premium significantly.

The peace of mind from adequate renters insurance isn’t abstract-it’s the confidence that a fire, theft, or lawsuit won’t destroy your finances. Contact North Point Insurance Group today to get your renters insurance quote and stop leaving your financial security to chance.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.