Georgia Auto Insurance Discounts: How to Save on Premiums

Georgia drivers overpay for auto insurance every single day. Most people stick with their current policy without realizing they’re leaving hundreds of dollars on the table each year.

At North Point Insurance Group, we’ve helped countless drivers find auto insurance discounts in Georgia that actually work. The strategies in this post will show you exactly where those savings hide and how to claim them.

The Three Biggest Ways to Cut Your Georgia Auto Insurance Bill

Bundling Policies Delivers Immediate Savings

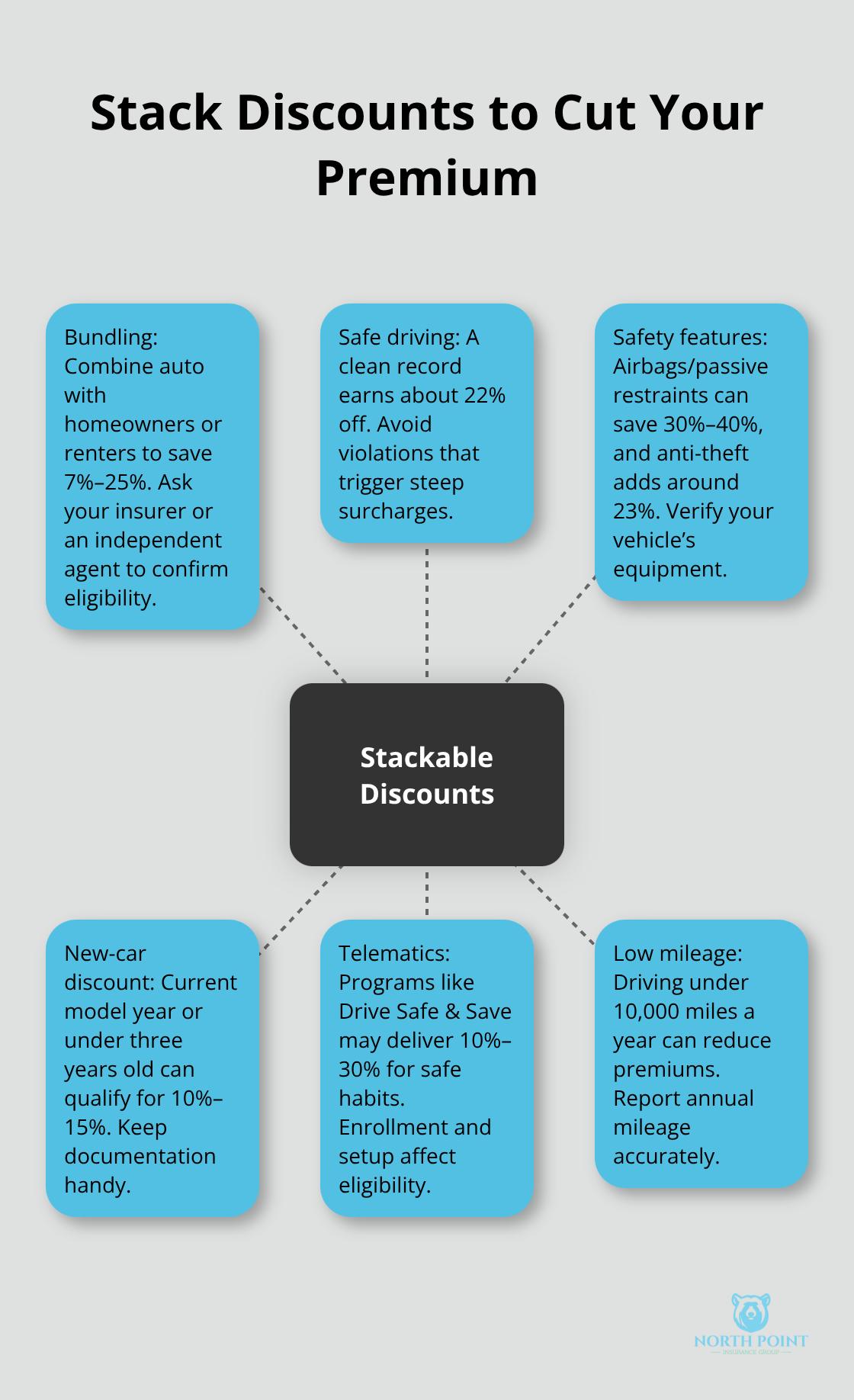

Data shows undling your auto policy with homeowners or renters insurance cuts your premium substantially. Drivers who bundle save between 7% and 25% on their rates. If you own a home or rent an apartment in Georgia, this discount alone can save you hundreds annually. The math is straightforward: a driver paying $213 per month for full coverage could pocket $15 to $53 each month just by combining policies with the same insurer.

The key is asking your insurer explicitly about bundling options when you shop, because many drivers assume they already have this discount when they don’t. An independent agent can shop multiple carriers to find the best bundling rates for your specific situation, comparing options across 20+ insurers to identify which combination saves you the most money.

Safe Driving History Generates Substantial Discounts

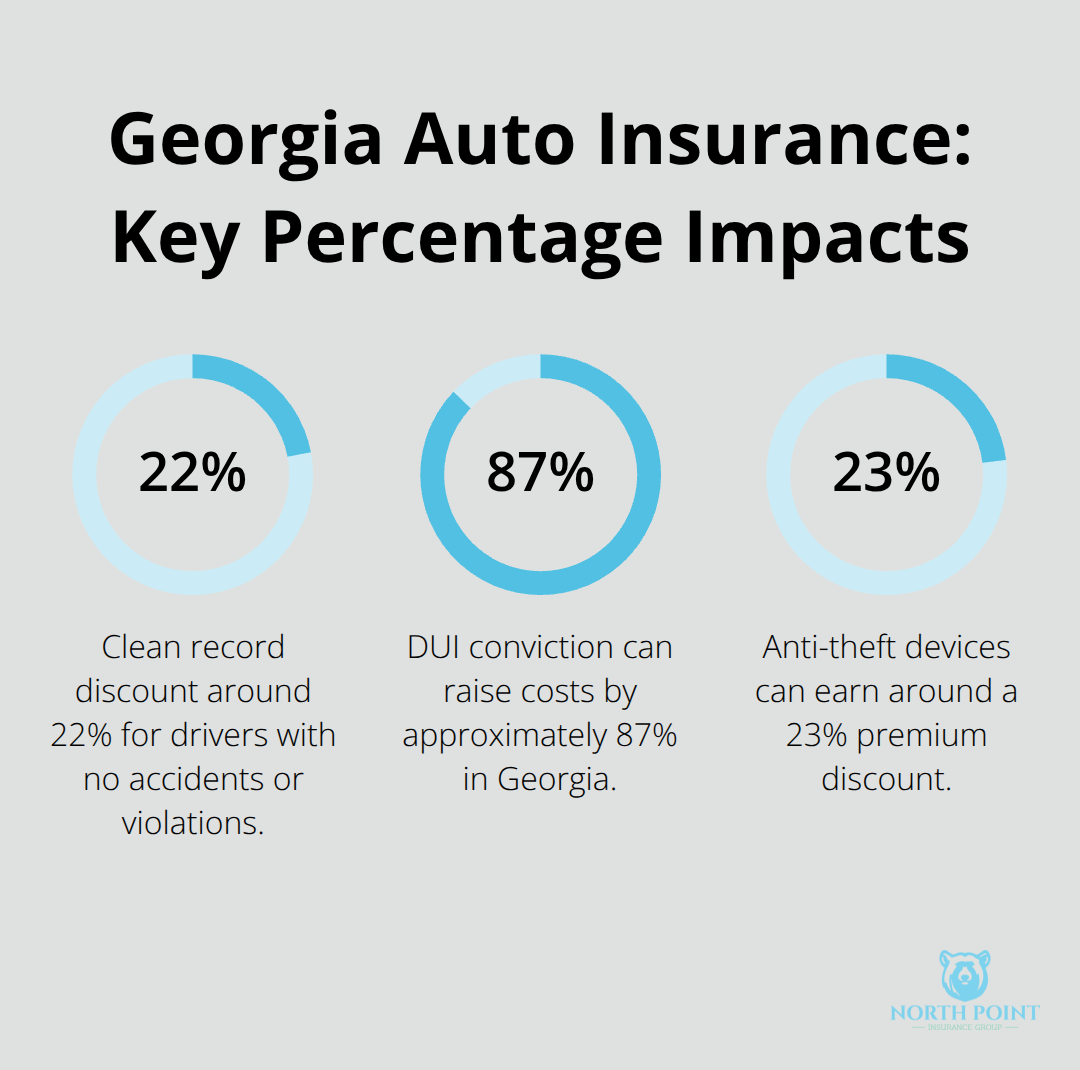

A clean driving record generates discounts around 22%, meaning a driver with no accidents or violations can save roughly $47 per month on a $213 monthly premium. Georgia’s minimum liability limits are 25/50/25, but increasing to 50/100/50 often costs only slightly more while protecting you far better after an accident. The real trap appears after a single at-fault accident: premiums spike by more than $800 annually in Georgia, with some insurers charging substantially more.

Data suggests that a DUI conviction hits even harder, raising costs by approximately 87%. This makes defensive driving courses financially smart. Drivers who complete a Georgia Department of Driver Services-approved course within the last three years qualify for the Defensive Driving Course Discount, which renews every three years if you maintain a clean record. The discount applies immediately for new policies or at course completion for existing ones.

Vehicle Safety Features Lower Your Premiums

Vehicles with airbags and anti-theft devices earn discounts reaching 30% to 40% for passive restraints and around 23% for anti-theft features. Newer cars qualify for new-car discounts of 10% to 15% when the vehicle is the current model year or under three years old. Telematics programs like Drive Safe & Save use your actual driving data to calculate discounts, with safe drivers potentially saving 10% to 30%. Georgia eligibility for these programs depends on setup and individual circumstances, so confirm availability with your insurer.

The combination strategy works best: a driver insuring multiple vehicles, bundling policies, maintaining a clean record, and driving a newer safe car with anti-theft features can stack discounts to cut premiums dramatically. Georgia premiums have climbed from $1,161 in 2015 to $2,039 in 2024, making discount stacking essential for affordability. Understanding which discounts apply to your specific vehicle and driving profile requires comparing quotes across multiple carriers-a process that reveals which insurers offer the best rates for your exact situation.

How to Compare Quotes and Find Real Savings

Request Quotes from Multiple Carriers with Identical Information

Shopping multiple carriers is not optional if you want the lowest rate in Georgia. Insurance rates vary wildly between insurers for identical coverage, with premiums ranging from approximately $50 per month for liability-only. That $24 monthly difference compounds to $288 annually on a single policy. When you add full coverage, the spread widens dramatically.

You find these gaps only by requesting quotes from at least three to five different insurers with identical coverage limits and deductibles. Provide each insurer the same vehicle description, driving profile, coverage selections, and household information so comparisons reflect actual price differences rather than quote variations. Most carriers now offer online quote tools that generate estimates in minutes, eliminating the excuse of shopping inconvenience.

Evaluate Coverage Limits Against Your Actual Needs

Coverage limits deserve serious attention because underinsuring costs far more than overinsuring. Georgia’s minimum liability limits of 25/50/25 leave you vulnerable after a serious accident. Increasing to 50/100/50 typically costs only slightly more per month while protecting substantially more of your assets.

Review your vehicle’s actual cash value and your personal assets to determine whether collision and comprehensive coverage make financial sense. If you own a vehicle worth less than $10,000, the premium for collision and comprehensive coverage might exceed the vehicle’s replacement value within a few years. Conversely, if you financed or leased your vehicle, your lender requires physical damage coverage regardless of value.

Leverage Low-Mileage and Usage-Based Discounts

Low-mileage discounts and usage-based programs like Drive Safe & Save reward actual driving patterns rather than assumptions. Drivers logging under 10,000 miles annually qualify for reduced premiums since they spend less time exposed to accident risk. Telematics programs take this further by monitoring your acceleration, braking, and nighttime driving, with safe drivers saving 10% to 30% according to Insurify data.

Georgia eligibility depends on individual circumstances and insurer requirements, so confirm program availability before enrolling. The key is honest evaluation of your actual coverage needs and driving habits, then requesting quotes that reflect your true situation rather than accepting default options. Once you’ve gathered quotes and identified your ideal coverage levels, the next step involves working with a local insurance agent who understands Georgia’s specific insurance landscape and can help you navigate discount opportunities you might otherwise miss.

Where to Find Discounts You’re Missing

Review Your Current Policy for Hidden Savings

Most Georgia drivers leave hundreds of dollars in savings unclaimed because they never ask the right questions. Your current policy likely includes discounts you don’t know about, and your insurer won’t volunteer information about lesser-known savings that could apply to your situation. Drivers who take thirty minutes annually to review their coverage and ask specific discount questions reduce their premiums by an average of 15% to 20% beyond their initial quote.

Start with your current policy and list every discount applied-most insurers show these clearly in the declarations page. Then contact your agent with a specific question: what discounts am I eligible for that aren’t currently on my policy? Common overlooked discounts include paperless billing, automatic payment enrollment, and good-driver discounts that require explicit activation.

Activate Discounts You Already Qualify For

Some insurers offer discounts for completing safe-driving courses through the Georgia Department of Driver Services, which not only saves money immediately but protects your rate for three years if you maintain a clean record. Ask whether your vehicle qualifies for anti-theft discounts if you’ve installed aftermarket security systems, since many drivers pay for these systems but never claim the associated savings.

Low-mileage discounts apply if you drive under 10,000 miles annually, yet countless Georgia drivers qualify without realizing it. The difference between a policy with three stacked discounts and one with seven can easily exceed $60 monthly. Your agent can identify which discounts stack on your policy and which ones conflict with each other, since some insurers restrict certain discount combinations.

Work with an Independent Agent to Compare Carriers

An independent agent fundamentally changes your discount outcomes because agents shop multiple carriers simultaneously rather than accepting whatever your current insurer offers. When you call a regional or national carrier directly, you speak with someone limited to that company’s discounts and rates. An independent agent compares your profile across 20+ insurers and identifies which companies offer the best combination of rates and discounts for your exact situation.

An agent also knows which carriers in Georgia frequently offer unpublished discounts to loyal customers or which companies run seasonal promotions. They understand that discount eligibility varies dramatically by ZIP code, vehicle type, and driving profile-information you cannot gather alone through online quotes.

Model Different Coverage Scenarios

Ask your agent to model scenarios showing your premium if you increase your deductible or adjust coverage limits, then compare that against the actual cost difference with a competing insurer. This analysis reveals whether paying slightly higher premiums for better coverage makes financial sense for your assets and driving habits. After securing quotes, ask your agent to identify any additional discounts you haven’t yet qualified for but could access within the next year (such as completing a defensive driving course or installing an anti-theft device) so you can plan for future savings.

Final Thoughts

Georgia drivers waste hundreds of dollars annually on auto insurance premiums they could reduce through discounts and comparison shopping. The strategies throughout this post reveal exactly where those savings hide: bundling policies for 7% to 25% off, maintaining a clean driving record for 22% discounts, and leveraging vehicle safety features that cut premiums by 10% to 40%. These aren’t theoretical savings-they’re concrete reductions that compound year after year, and most Georgia drivers qualify for multiple discounts they’ve never activated.

Your next step requires pulling out your current policy and listing every discount you already receive, then contacting your insurer to ask what you’re missing. Many drivers qualify for discounts from paperless billing to low-mileage programs without realizing it, and the difference between a policy with three discounts and one with seven can exceed $60 monthly. Georgia premiums have climbed from $1,161 in 2015 to $2,039 in 2024, making comparison shopping essential rather than optional.

An independent agent transforms this process by shopping multiple carriers simultaneously and identifying which companies offer the best combination of rates and discounts for your profile. At North Point Insurance Group, our local agents understand Georgia’s specific insurance landscape and can model different coverage scenarios to show you exactly how much you’ll save with each option (we handle the comparison work so you don’t have to). Contact us today to review your current policy and request quotes from competing insurers-the time investment pays for itself within weeks through the savings you’ll uncover.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.