Georgia Auto Insurance Guide: Key Features and Tips

Georgia drivers face real costs when they get auto insurance wrong. We at North Point Insurance Group created this Georgia auto insurance guide to show you exactly what coverage you need, what affects your rates, and how to cut your premiums without cutting corners.

This guide walks through mandatory requirements, rate factors, and proven money-saving strategies that work for Georgia drivers.

Georgia Auto Insurance Requirements and Coverage Types

Mandatory Liability Coverage Limits in Georgia

Georgia law requires you to carry bodily injury liability of at least $25,000 per person and $50,000 per accident, plus property damage liability of $25,000 per accident. These minimums exist for a reason-they cover damage you cause to others. But here’s the problem: they’re dangerously low. If you cause an accident that injures someone seriously, your $25,000 limit evaporates instantly, and you’re personally liable for everything beyond that.

We recommend carrying at least $100,000 in bodily injury coverage per person and $300,000 per accident-a relatively small premium increase that protects your actual assets. This higher limit shields your home, savings, and future earnings from a lawsuit after a serious accident.

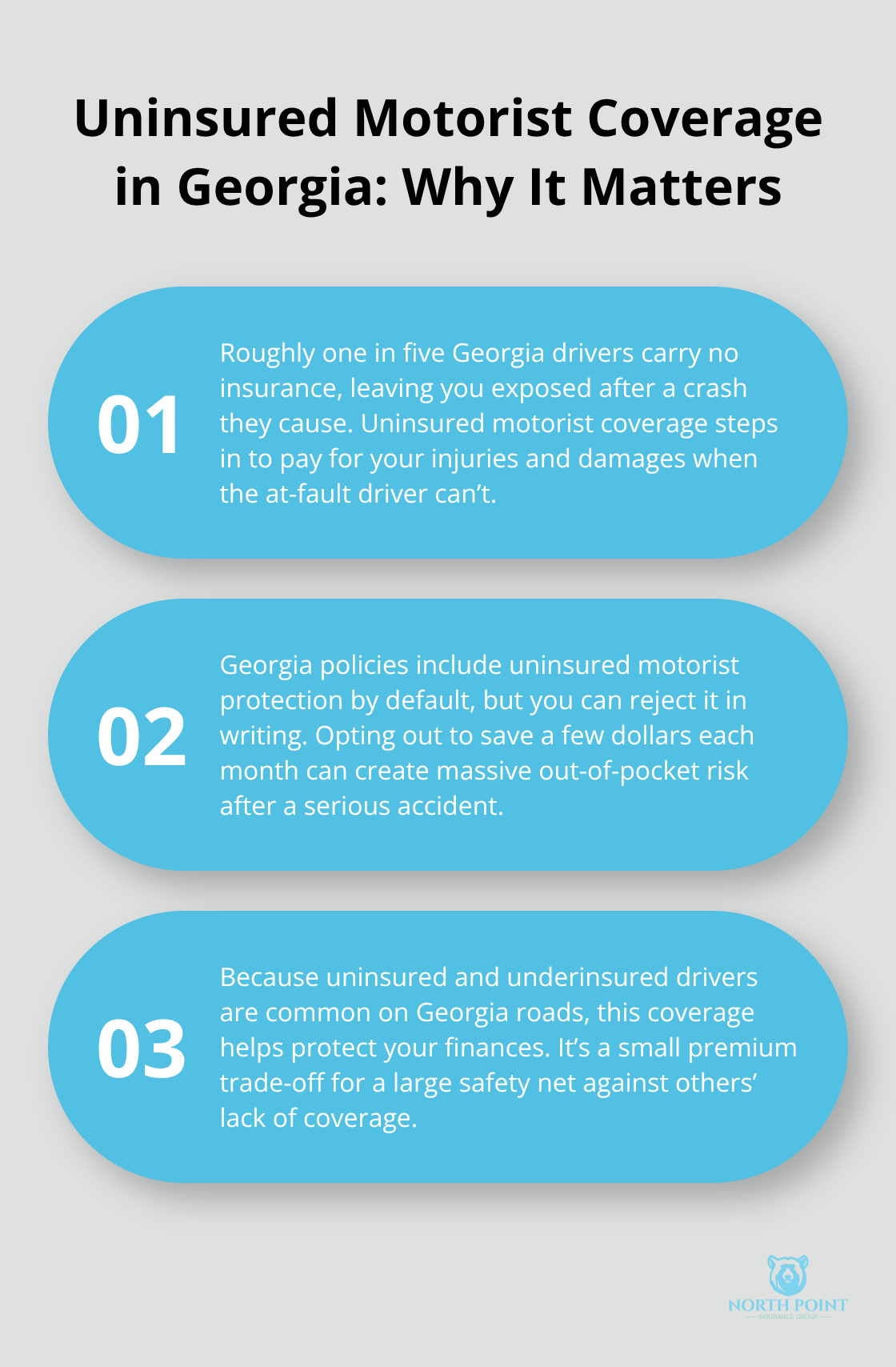

Uninsured Motorist Coverage: Your Safety Net

Uninsured motorist coverage deserves your attention because about 18.1 percent of Georgia drivers carry no insurance. This coverage protects you if an uninsured or underinsured driver hits you and can’t pay for damages. Georgia includes uninsured motorist protection in policies by default, but you can reject it in writing-a mistake many drivers make to save a few dollars monthly. The financial risk of driving without this protection far outweighs the monthly savings, especially given how many uninsured drivers share Georgia roads.

Comprehensive and Collision Coverage: What You Actually Need

Comprehensive and collision coverage are optional unless you finance or lease your vehicle, but they serve different purposes. Collision pays for damage from accidents with other vehicles or objects, while comprehensive covers theft, weather, vandalism, and glass damage. Comprehensive typically costs 20 to 30 percent less than collision because weather and theft claims happen less frequently than accidents.

If you own your vehicle outright and drive an older car worth less than $10,000, dropping these coverages might make financial sense. But if your vehicle has real value or you drive in Atlanta or other high-risk areas, the cost of being uninsured after a total loss far exceeds the monthly premium savings. Calculate your vehicle’s actual value, check your local theft and weather claim rates, and decide whether you can absorb a total loss without financial hardship.

Your coverage choices directly impact how much you pay each month, but your driving record, location, and vehicle type shape your rates even more dramatically.

Factors That Affect Your Georgia Auto Insurance Rates

Driving Record: The Biggest Cost Driver

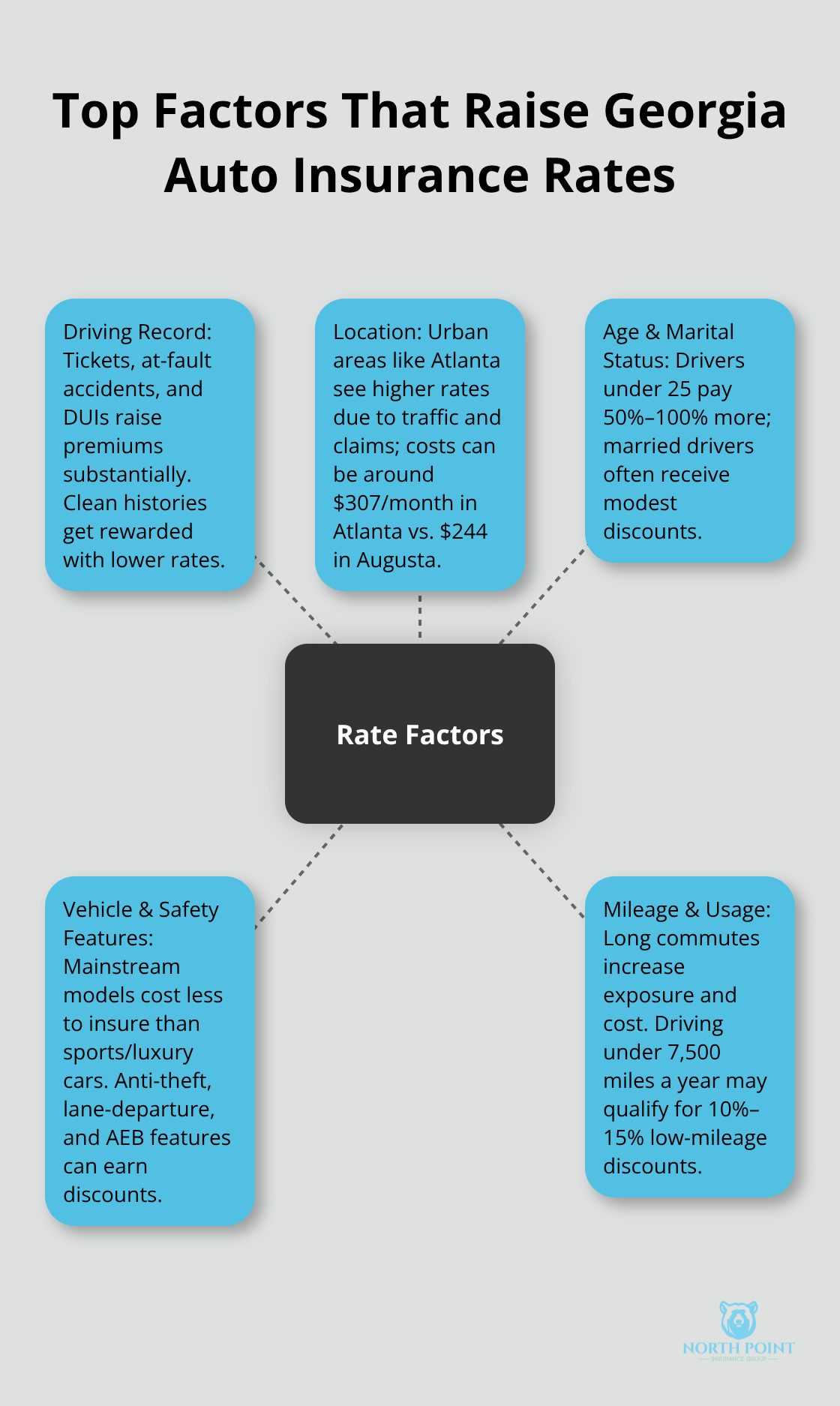

Your driving record is the single most important factor determining what you pay for auto insurance in Georgia. Insurers examine your history over the past three to five years, and even one at-fault accident or traffic violation spikes your premium significantly. A speeding ticket or minor fender-bender raises your rates 10 to 40 percent depending on severity. A DUI conviction hits much harder-your premiums can double or triple for years.

Insurers view drivers with clean records as lower-risk investments, so they reward you with lower rates.

Defensive driving courses offer one of the fastest ways to lower your costs without changing coverage. These courses reduce your premium by at least 10 percent on liability, collision, and first-party medical coverage if all named drivers meet age requirements. A four-hour course (available in most Georgia counties) costs around $20 to $50 and typically saves drivers $100 to $150 annually. That financial return makes the time investment worthwhile.

Age, Gender, and Location: Demographic Rate Factors

Drivers under 25 pay substantially higher premiums because they cause accidents at higher rates-insurance data consistently shows this demographic represents outsized risk. Young drivers in Georgia can expect to pay 50 to 100 percent more than drivers in their 40s or 50s. Marital status affects rates too; married drivers often qualify for modest discounts because they statistically file fewer claims.

Your location within Georgia creates dramatic rate differences. Atlanta drivers pay significantly more than drivers in rural areas because traffic density and accident frequency increase costs. A driver in Atlanta pays roughly $307 monthly for full coverage, while a driver in Augusta pays about $244 monthly-a $63 difference that compounds to over $750 annually.

Vehicle Type and Usage Patterns: Hidden Rate Multipliers

Your vehicle itself determines a significant portion of your rate. A Honda Accord or Toyota Camry costs far less to insure in Georgia than a sports car or luxury sedan because repair costs are lower and theft rates remain manageable. Insurance companies also examine how you use your vehicle-commuting 50 miles daily to Atlanta costs more than occasional local driving because higher mileage increases accident exposure.

If you work from home or drive less than 7,500 miles annually, mention this to your agent; some insurers offer low-mileage discounts that reduce your premium by 10 to 15 percent. Vehicle safety features matter significantly as well. Cars equipped with anti-theft devices, lane-departure warnings, or automatic emergency braking qualify for additional discounts because these features demonstrably reduce claim frequency and severity. When shopping for your next vehicle, checking insurance costs before you buy takes ten minutes online and can save you hundreds annually.

These rate factors combine to create your final premium, but smart drivers can control several of them through their choices and behavior. The next section reveals proven strategies that Georgia drivers use to cut their costs without sacrificing protection.

Money-Saving Strategies for Georgia Drivers

Bundle Your Policies for Immediate Savings

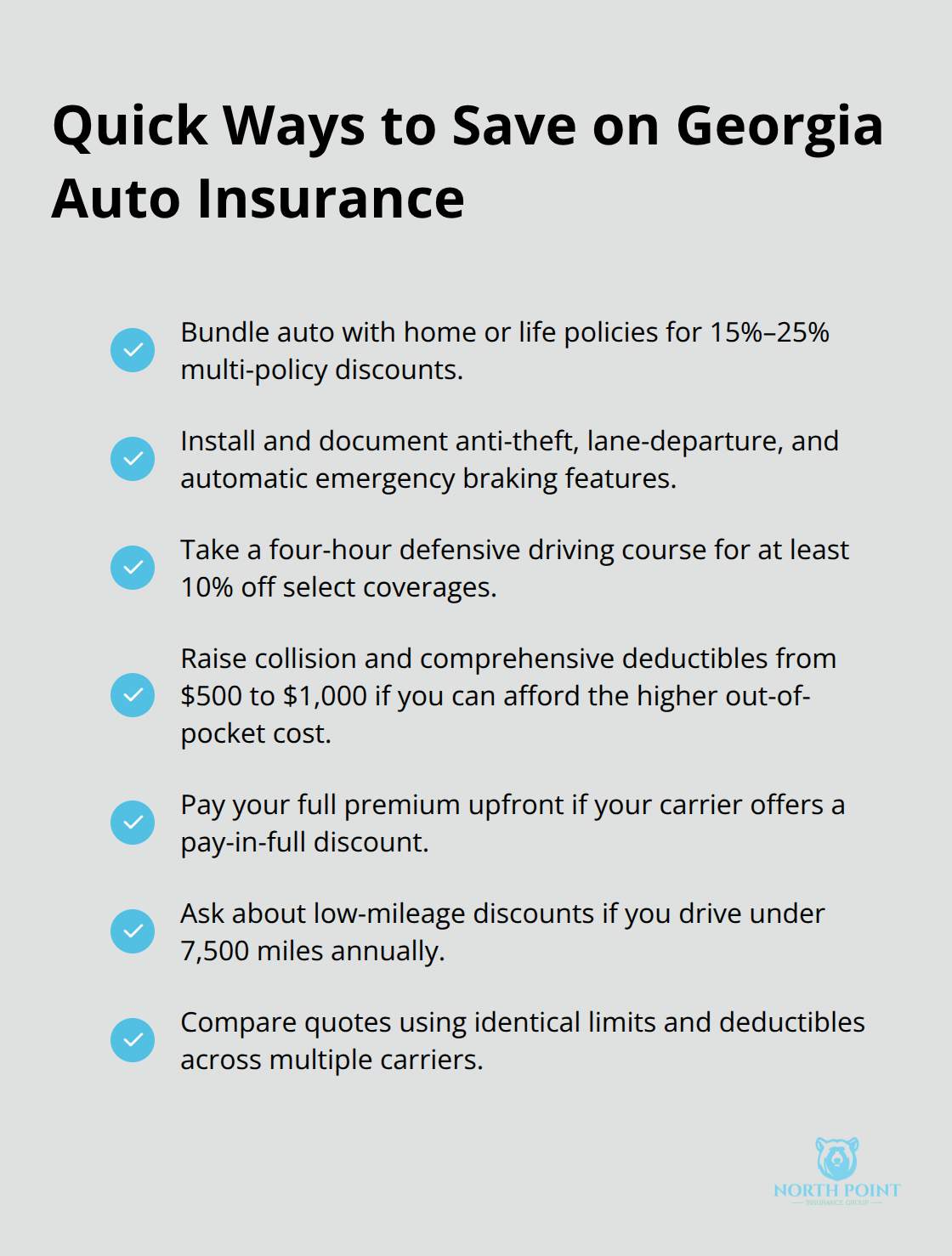

Bundling your auto insurance with home, life, or other policies at the same carrier delivers immediate savings that most Georgia drivers overlook. Multi-policy discounts typically reduce your combined premiums by 15 to 25 percent, meaning a driver paying $260 monthly for full-coverage auto insurance could save $39 to $65 monthly just by moving their homeowners policy to the same insurer. That compounds to $468 to $780 annually with zero effort beyond a phone call.

The math becomes even more compelling when you factor in that bundling also simplifies your billing and claims process, reducing the time you spend managing multiple insurance accounts. If you currently split your policies across different carriers, request quotes from each company for bundled coverage before renewing. Many Georgia drivers discover they could pay less total premium for better combined coverage by consolidating rather than shopping each policy separately.

Install Safety Features and Take Defensive Driving Courses

Safety features installed on your vehicle qualify for concrete discounts that insurers track closely. Anti-theft devices, lane-departure warnings, and automatic emergency braking systems reduce your premium because they demonstrably lower claim frequency and severity. If your vehicle already has these features, confirm they’re listed on your policy because some drivers miss discounts simply because their agent didn’t document the equipment.

Defensive driving courses represent your fastest path to immediate savings without equipment investments. A four-hour course costs $20 to $50 in most Georgia counties and reduces your premium by at least 10 percent on liability, collision, and first-party medical coverage. That $100 to $150 annual savings pays for the course in the first month.

Adjust Your Deductible and Payment Method

Raising your deductible from $500 to $1,000 on collision and comprehensive coverage typically lowers your monthly premium by $15 to $30 depending on your vehicle and location. The trade-off demands honest self-assessment: can you actually cover a $1,000 deductible without financial stress if you file a claim? If yes, the savings accumulate fast. A $20 monthly savings from a higher deductible reaches $240 annually.

Paying your full annual premium upfront rather than in monthly installments also reduces costs in most states, though this option isn’t available in California and may vary by carrier in Georgia. Ask your agent specifically whether upfront payment qualifies for a discount in your situation, and calculate whether setting aside the lump sum makes sense for your budget before committing.

Final Thoughts

Georgia auto insurance costs more than most states, but this guide shows you exactly why and what actions cut your premiums without sacrificing protection. Your mandatory liability limits of $25,000 per person and $50,000 per accident form your legal foundation, yet carrying higher limits protects your actual assets from lawsuit exposure after a serious accident. Uninsured motorist coverage shields you against the 18.1 percent of Georgia drivers operating without insurance, while comprehensive and collision coverage decisions depend on your vehicle’s value and your ability to absorb a total loss.

The money-saving strategies in this Georgia auto insurance guide work because they address real cost drivers that affect your monthly bill. Bundling policies saves 15 to 25 percent of your combined premiums, a four-hour defensive driving course costs $20 to $50 and returns $100 to $150 in annual savings, and raising your deductible from $500 to $1,000 cuts your monthly premium by $15 to $30. These aren’t theoretical savings-Georgia drivers implement them every month and watch their premiums drop substantially.

Your next step involves comparing quotes from multiple carriers using identical coverage limits and deductibles so you see true price differences rather than coverage variations. Document any safety features on your vehicle, mention low annual mileage if it applies to your situation, and request quotes for bundled policies if you carry homeowners or life insurance elsewhere. When you’re ready, the team at North Point Insurance Group can help you find coverage that matches your actual needs and budget.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.