New Driver Auto Insurance: What Every New Driver Should Know

Getting your first car is exciting. But new driver auto insurance can feel overwhelming with all the coverage options, legal requirements, and pricing factors to consider.

At North Point Insurance Group, we’ve helped countless new drivers navigate these decisions. This guide breaks down everything you need to know to find coverage that protects you without breaking your budget.

What Coverage Do You Actually Need as a New Driver

Every state requires liability coverage before you can legally drive, but the minimums vary significantly. Most states require at least $15,000 in bodily injury liability per person and $30,000 per accident, though some states push higher. Check your state’s requirements first because driving without the legal minimum results in fines, license suspension, and potential legal liability if you cause an accident.

Go Beyond State Minimums

State minimums protect you legally, but they don’t protect your wallet. If you cause a major accident, a $30,000 limit disappears fast when medical bills and vehicle damage pile up. Try $100,000 per person and $300,000 per accident as a practical baseline that actually protects your assets. This higher coverage costs only slightly more than minimums but shields you from catastrophic financial exposure.

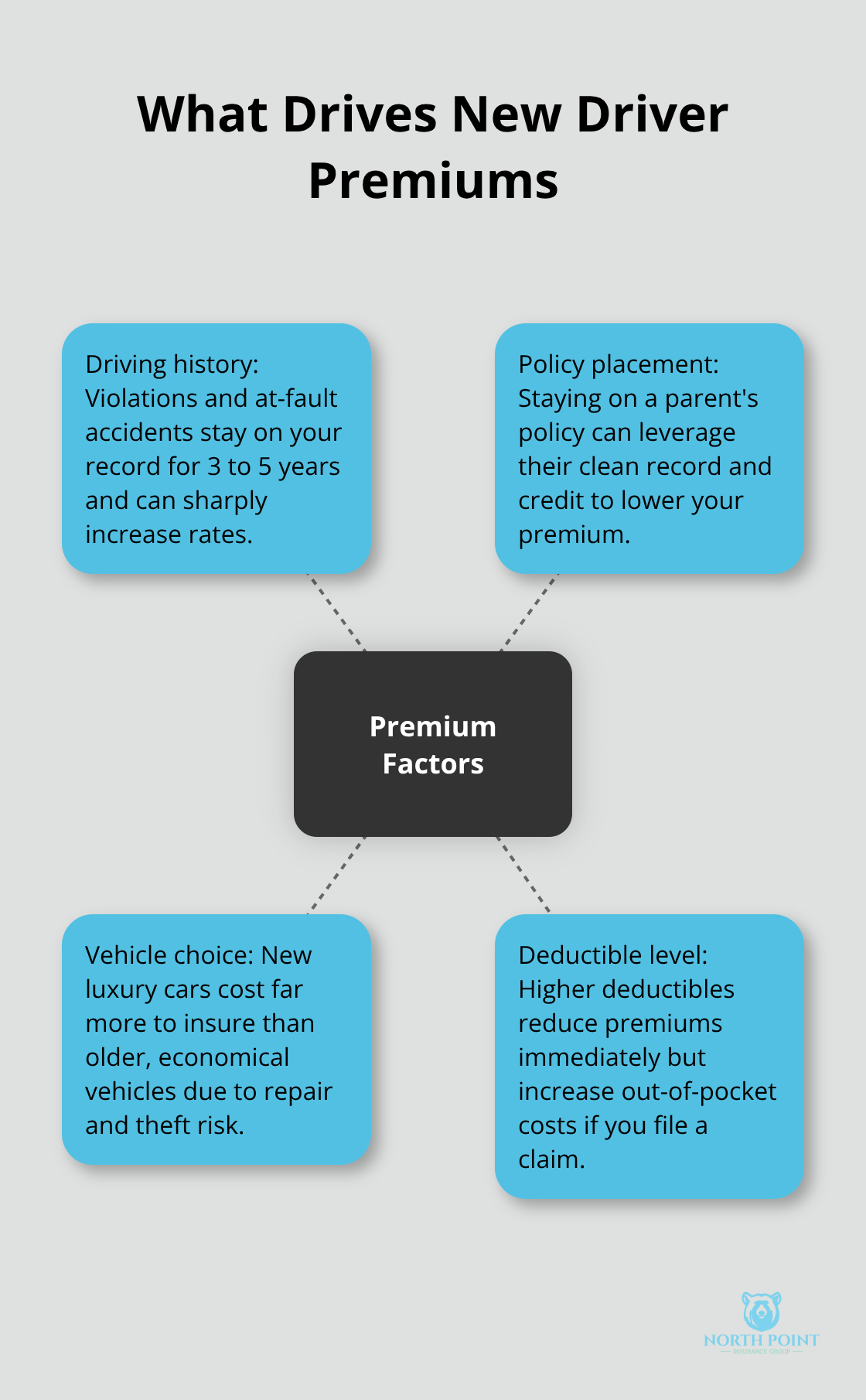

Why New Drivers Pay More

New drivers face higher premiums because insurers view them as statistically riskier. Your driving history, location, and the vehicle you choose are the biggest cost factors.

Tickets and at-fault accidents stay on your record for three to five years and cause premiums to rise substantially. If you stay on a parent’s policy, their clean driving record and credit profile work in your favor. The vehicle matters too-insuring a brand-new luxury car for a new driver costs far more than an older, economical vehicle. Choosing a higher deductible reduces premiums immediately, though you’ll pay more out of pocket if you file a claim.

Required vs. Optional Coverage

Liability coverage pays for damages you cause to others and is legally required everywhere. Collision coverage pays for damage to your own vehicle from crashes, and comprehensive coverage handles theft, weather, and vandalism. If you’re financing or leasing your car, your lender requires both collision and comprehensive, so you don’t have a choice there.

For new drivers, optional coverages worth considering include 24-hour roadside assistance and rental car reimbursement. These cost little but provide genuine help when your car breaks down or needs repairs.

Discounts That Lower Your Premium

Defensive-driving courses reduce premiums and provide practical skills that matter more than any discount. Shop quotes from multiple insurers because each company weighs risk factors differently, and the difference between carriers can exceed $400 annually for identical coverage. This comparison process reveals which insurers value your specific situation most favorably.

How to Get Lower Insurance Rates as a New Driver

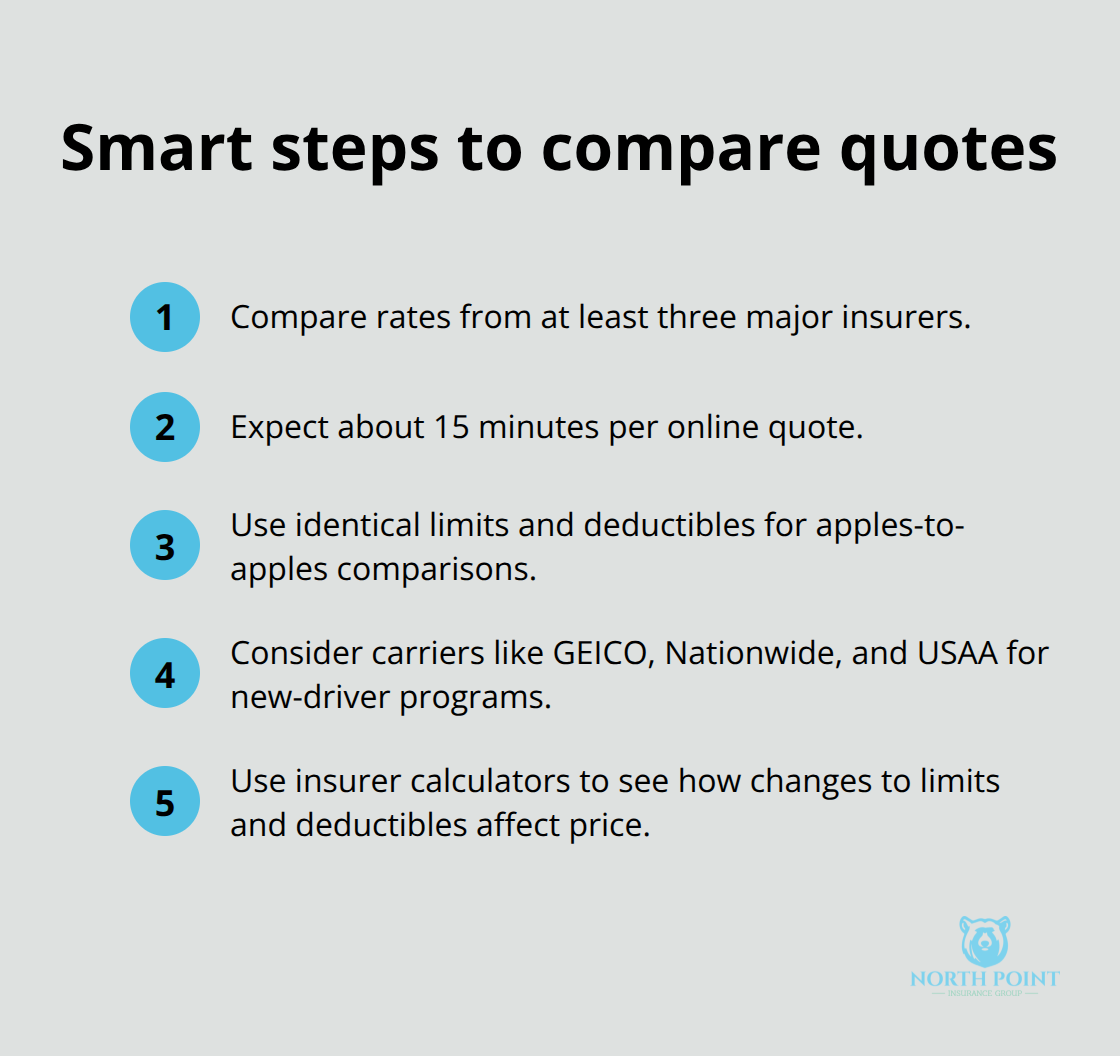

Shopping around for quotes isn’t optional-it’s the single most effective way to lower your premium. According to Car and Driver, each insurer weighs risk factors differently, and comparing quotes from multiple carriers can save you more than $400 annually on identical coverage. Start with at least three major insurers online, which typically takes 15 minutes per quote. The Zebra identifies GEICO, Nationwide, and USAA as strong options for new drivers due to affordability and helpful driver-discount programs. When comparing quotes, use identical coverage limits and deductibles across all quotes so you’re making true apples-to-apples comparisons. Many insurers now offer online calculators that show exactly how changes to deductibles, limits, and coverage types affect your final price.

This transparency helps you understand where your money goes and where you can trim costs without sacrificing protection.

Discounts That Actually Add Up

Good student discounts apply to drivers under 25 with around a 3.0 GPA and typically require periodic transcripts to verify eligibility. Defensive-driving courses qualify you for discounts and provide skills that genuinely matter on the road-you’ll need to provide transcripts or completion certificates to verify the course. Multi-car discounts apply if your family has more than one vehicle insured with the same company, and bundling auto with home insurance can save over $950 according to Liberty Mutual’s data.

Anti-theft devices and safety features installed in your vehicle can reduce premiums, so disclose any equipment when shopping quotes. Some insurers offer occupation-based discounts for certain professions due to perceived lower claim risk, so mention your job when getting quotes. The most powerful discount for new drivers comes from staying on a parent’s policy rather than purchasing standalone coverage-adding a new teenage driver to a family policy costs roughly half what a standalone policy would, according to WalletHub. If you stay on a parent’s policy, their clean driving record and credit profile directly benefit your rate.

Why Your Driving Record and Car Choice Matter Most

Your driving record is your insurance future. Tickets and at-fault accidents stay on your record for three to five years and cause premiums to rise substantially, which is why avoiding violations during your first few years matters enormously. The vehicle you choose influences your premium as much as your driving history does. Insuring a brand-new luxury car costs far more than an older, economical vehicle because luxury cars cost more to repair and attract higher theft rates. When selecting a car, check IIHS crash-test ratings and choose vehicles with modern safety features like forward collision warning and lane departure warning-these features can meaningfully improve your safety profile and may lower premiums over time. Vehicles with lower theft risk and cheaper repair costs naturally cost less to insure. Higher deductibles reduce premiums immediately; choosing a $1,000 deductible instead of $500 noticeably lowers your monthly payment, though you’ll pay more out of pocket if you file a claim.

Taking Action on Your Insurance Search

Your next step involves gathering information about your specific situation. Prepare your driver’s license, vehicle details (make, model, year, and mileage), and your state’s minimum coverage requirements before you start requesting quotes. This preparation streamlines the quote process and ensures you receive accurate pricing. Once you have multiple quotes in hand, you’ll be ready to evaluate which coverage options align with your budget and protection needs-a decision that sets the foundation for your first policy.

Insurance Mistakes That Cost New Drivers Real Money

Most new drivers either purchase too little coverage to save money upfront or buy a policy without reading what they actually bought. The first mistake stems from sticker shock-state minimums cost less, so new drivers assume that’s enough protection. But state minimums typically max out at $30,000 per accident, which evaporates instantly when medical bills and vehicle damage accumulate. A single serious accident can leave you personally liable for tens of thousands of dollars beyond what your insurance covers.

Why Insufficient Coverage Backfires

The financial exposure from low coverage limits shocks new drivers who face claims. Medical expenses alone from a moderate accident exceed $30,000 in seconds. Property damage to another vehicle, especially luxury cars, adds thousands more. You become responsible for the difference between what your insurance pays and what the injured party actually lost. This liability can follow you for years through wage garnishment or asset seizure, making the initial premium savings look foolish in hindsight.

Reading Your Policy Before You Buy

The second mistake happens because policies are dense documents that feel impossible to parse, so many new drivers sign without understanding their deductibles, coverage limits, or exclusions. Then they file a claim and discover their $500 deductible or limited coverage doesn’t match what they expected. Spend 20 minutes reading your policy documents or call your agent and ask them to walk you through exactly what your coverage includes, what your deductible is, and what situations aren’t covered. This conversation prevents the costly surprises that plague new drivers who cut corners on clarity.

Updating Your Policy When Life Changes

The third mistake involves life changes-moving to a new address, changing jobs, or adding another vehicle to your household-without updating your policy. Insurance companies use your location and driving patterns to calculate premiums, so failing to report changes means your coverage doesn’t reflect your actual situation and could complicate claims. Set a calendar reminder every six months to review your coverage and contact your insurer immediately to update your information if anything has changed.

Taking Control of Your Coverage

Choose coverage limits that actually protect your assets, not just the legal minimum-$100,000 per person and $300,000 per accident provides genuine financial protection and costs only marginally more than minimums. These three steps prevent the costly surprises that plague new drivers who cut corners on coverage or neglect to maintain accurate policy details.

Final Thoughts

State minimums leave you financially exposed, shopping multiple carriers saves hundreds annually, and your driving record matters more than anything else. Avoid the three mistakes that cost new drivers real money-insufficient coverage limits, skipping policy details, and failing to update information when life changes. Instead, choose coverage limits around $100,000 per person and $300,000 per accident, read your policy before purchasing, and set reminders to review your coverage every six months.

Start by gathering your driver’s license, vehicle information, and your state’s minimum requirements, then request quotes from at least three major insurers. Use identical coverage limits across all quotes so you compare apples to apples, and look for discounts that apply to your situation-good student discounts, defensive driving course completion, multi-car bundling, and safety features all reduce premiums. The vehicle you choose influences your premium as much as your driving history does, so prioritize cars with strong IIHS crash ratings and modern safety features.

At North Point Insurance Group, our local agents understand that new driver auto insurance requires clear guidance without the call-center runaround. We shop 20+ carriers to find coverage that fits your situation and budget, whether you’re deciding between staying on a parent’s policy or going solo, selecting the right vehicle, or understanding what coverage you actually need. Contact our agents to walk through every decision and get this right from the start.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.