Home Insurance Coverage Explained: Building a Solid Policy

Most homeowners think their insurance covers everything-until they file a claim and discover it doesn’t. We at North Point Insurance Group see this gap between expectations and reality every day.

Home insurance coverage explained properly means understanding what’s actually protected and what isn’t. This blog post walks you through the coverage you have, the gaps you might miss, and how to build a policy that actually fits your home.

What Your Home Insurance Actually Protects

The Three Core Coverages That Matter Most

Your homeowners policy protects three main areas, and understanding exactly what each covers prevents costly surprises when you need to file a claim. Dwelling coverage pays to repair or rebuild your house structure and attached features like decks or garages after a covered loss-fire, windstorm, hail, theft, or vandalism. If a storm damages your roof, dwelling coverage handles repairs up to your policy limit minus your deductible. Personal property coverage reimburses you for furniture, clothing, electronics, and other belongings inside your home when they’re damaged or stolen. Contents coverage typically pays based on replacement cost, meaning you receive funds to buy new items at current prices rather than depreciated values, which matters significantly when replacing a five-year-old television versus a one-year-old one.

Liability and Medical Payments Protection

Liability protection shields you financially if someone is injured on your property or if you accidentally damage someone else’s property-your policy covers their medical bills and legal defense costs if they sue. Medical payments coverage works differently: it pays a guest’s immediate medical expenses if they’re injured at your home, regardless of who’s at fault, without requiring a lawsuit.

Why Rebuild Cost Matters More Than Home Value

The National Association of Insurance Commissioners notes that dwelling coverage limits depend on your home’s rebuild cost, construction type, distance to fire and water sources, and your home’s age and condition. Most homeowners significantly underestimate rebuild costs because they confuse home value with replacement cost-a $400,000 home might cost $550,000 to rebuild due to labor and material inflation. Your contents coverage typically maxes out at 50 to 70 percent of dwelling coverage, so a $300,000 dwelling limit might cover only $150,000 to $210,000 in belongings, which doesn’t protect high-value items like jewelry or art adequately.

The Hidden Limits in Standard Coverage

Personal liability coverage usually starts at $100,000, but that’s often insufficient for serious incidents; a court judgment could exceed this limit easily. Medical payments coverage typically provides $1,000 to $5,000 per person, covering immediate expenses but not ongoing medical care. The gap between what you think you’re covered for and what you actually are covered for creates real financial exposure. This is precisely why reviewing your declarations page matters before a loss occurs, not after-and why many homeowners discover they need additional protection through endorsements and riders that address their specific vulnerabilities.

Coverage Gaps That Cost Homeowners Thousands

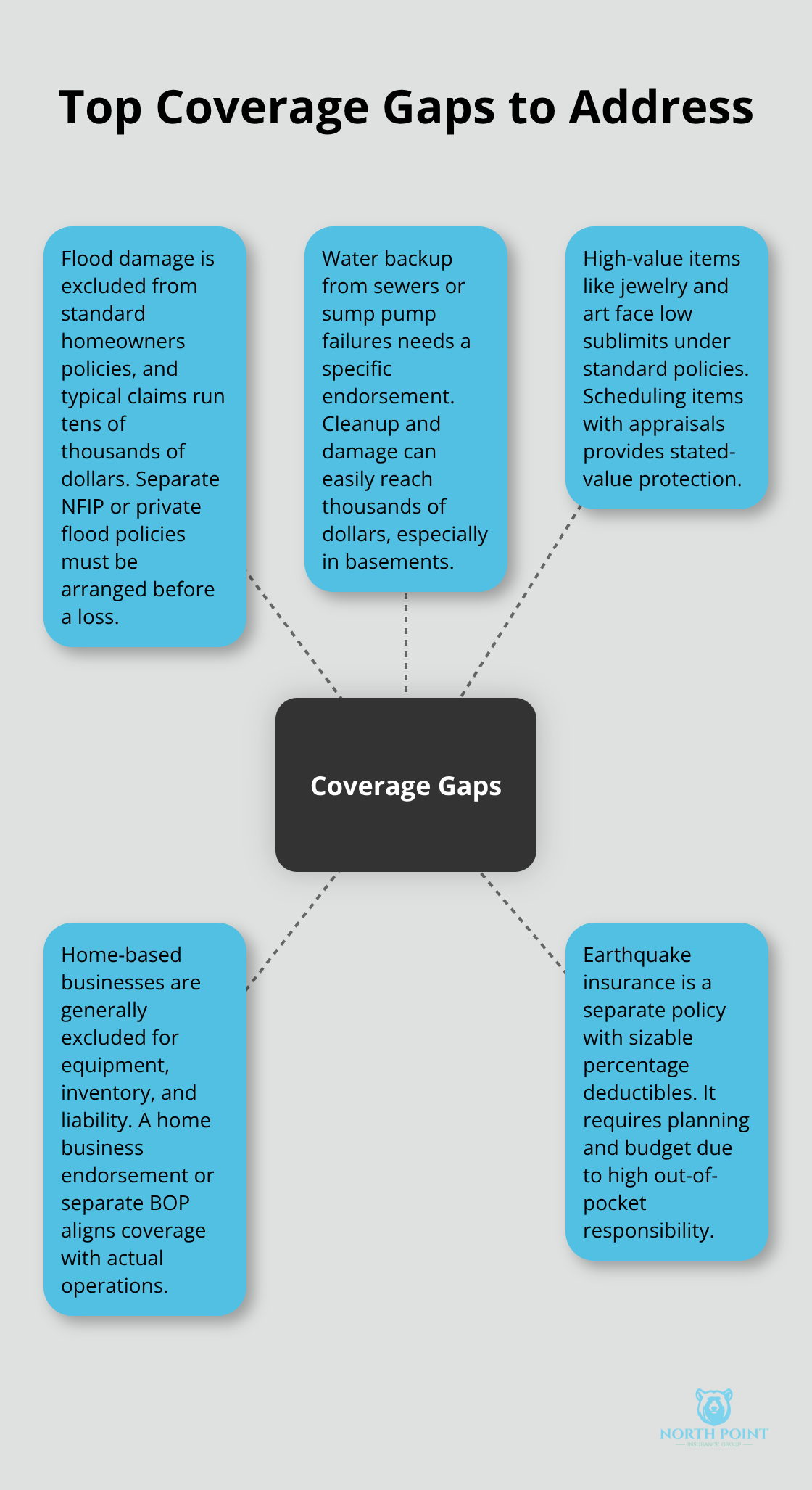

Flood Damage Remains Your Biggest Blind Spot

Flood damage destroys more than 1 in 4 homes since 2020 according to Kin Insurance, yet standard homeowners policies exclude it entirely. This gap costs real money-flood claims average $30,000 to $70,000 in damages, and homeowners without separate flood coverage pay the full amount out of pocket. The National Flood Insurance Program and private flood insurers offer policies with their own deductibles, typically ranging from $1,000 to $10,000, but you must apply for them separately before a loss occurs. Waiting until after a flood warning appears means you cannot obtain coverage, so homeowners in flood-prone areas need to act now rather than later.

Water Backup and Sewer Issues Require Specific Protection

Water backup from sewers or sump pump failures presents another blind spot most homeowners ignore until it happens. These events require a specific endorsement to your standard policy, yet countless homeowners have never added this protection despite living in areas where basement flooding is predictable. Sewer backups alone cost homeowners $2,500 to $25,000 in cleanup and property damage, making the endorsement a practical necessity if your home has a basement or finished lower level. Adding this coverage costs relatively little and protects against a predictable risk in many regions.

High-Value Items Get Minimal Protection Under Standard Policies

Jewelry, art, collectibles, and antiques receive minimal protection under standard coverage because personal property limits cap expensive items at $1,500 to $2,500 total. A single piece of jewelry worth $5,000 or an art collection valued at $15,000 receives drastically inadequate coverage, leaving you personally responsible for most losses. Scheduled personal property endorsements specify exact values for these items and cost relatively little-typically $50 to $200 annually depending on the items and your location-but they require documentation like appraisals or receipts before you add them. This endorsement transforms inadequate coverage into actual protection for what matters most to you.

Home-Based Businesses Need Separate Coverage

Standard homeowners policies exclude business equipment, inventory, and liability claims arising from business activities, which means a customer injured during a client meeting at your home receives no coverage under your homeowners liability. If you operate any business from your residence (consulting, freelancing, e-commerce, coaching, or service work), you need either a home business endorsement or a separate business owners policy. The endorsement typically costs $200 to $500 annually and covers equipment and basic liability, but it has limits; serious business operations require dedicated commercial coverage instead. Documenting what you actually do at home, then discussing coverage options with your agent, matches protection to your specific business model.

Earthquake Insurance Requires Significant Financial Commitment

Earthquake insurance requires a separate policy in areas prone to seismic activity, with deductibles typically ranging from 5 to 25 percent of your home’s insured value. A $500,000 home could have a $25,000 to $125,000 deductible, making this coverage a significant financial commitment that many homeowners delay until after experiencing a small quake. These coverage gaps exist because certain risks are either catastrophic in scale or require specialized underwriting.

Understanding what your standard policy excludes allows you to make informed decisions about which additional protections actually fit your home and your situation.

Building a Policy That Actually Protects Your Home

Start With Replacement Cost, Not Home Value

Your home’s replacement cost differs significantly from its market value, and this distinction determines whether you’re adequately insured. The National Association of Insurance Commissioners emphasizes that rebuild cost depends on construction type, local labor rates, and material prices in your area-factors that have nothing to do with what your house would sell for today. Contact three local contractors and ask what it would cost to rebuild your home from the foundation up, including permits and current material prices. A $400,000 home in Atlanta might cost $550,000 to rebuild due to labor shortages and material inflation, while the same home in a rural area might cost $480,000. Your dwelling coverage limit should match or slightly exceed that rebuild figure.

Most homeowners set limits too low, then discover during a claim that they’re underinsured and responsible for the gap themselves. Contents coverage typically maxes out at 50 to 70 percent of your dwelling limit, so if you have $300,000 in dwelling coverage, you’re looking at $150,000 to $210,000 for everything you own-furniture, electronics, clothing, everything. That amount often falls short, which is precisely why high-value items need separate scheduled personal property endorsements rather than relying on standard coverage limits.

Choose a Deductible You Can Actually Afford

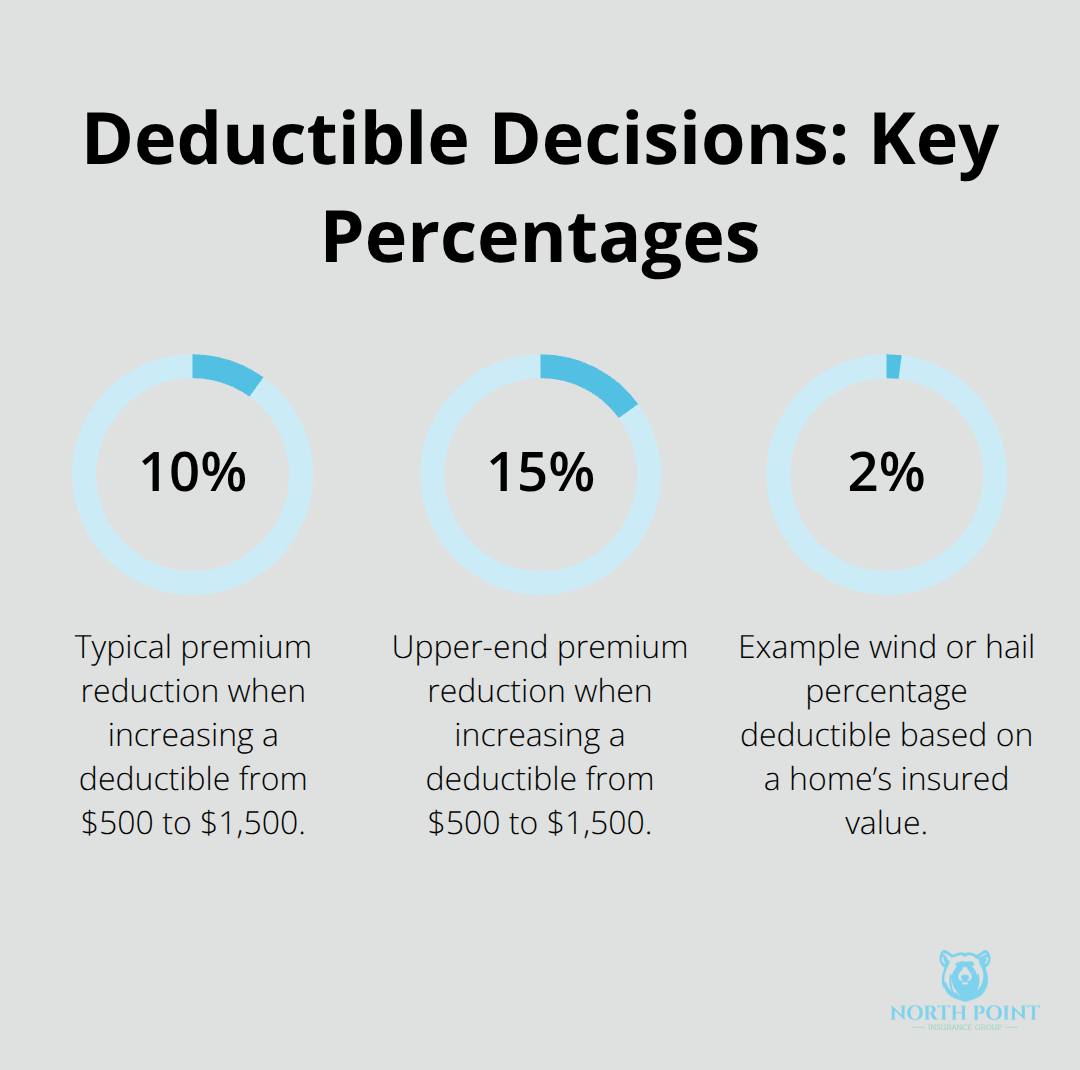

Your deductible choice directly impacts your monthly premium, so treat this as a financial decision rather than an abstract number. Most homeowners choose deductibles between $500 and $1,500, with $1,000 being typical, but the right choice depends on what you can actually afford to pay out of pocket if a loss occurs. Increasing your deductible from $500 to $1,500 typically lowers your annual premium by 10 to 15 percent, which might save you $100 to $200 yearly. That savings matters only if you can cover a $1,500 claim without financial stress; if you’d struggle to pay that amount, a lower deductible makes sense despite higher premiums.

Percentage-based deductibles exist for certain claims like wind or hail damage, particularly in coastal areas, and these function differently-a 2 percent deductible on a $400,000 home means you pay $8,000 before your insurer covers anything. Calculate what percentage-based deductibles actually cost you in real dollars before accepting them.

Add Endorsements for Your Specific Gaps

Once you’ve set your dwelling coverage and deductible, add endorsements for gaps you identified in your situation. Water backup coverage costs $50 to $100 annually and protects against sewer backups or sump pump failures-a predictable risk if you have a basement. Scheduled personal property endorsements for jewelry, art, or collectibles cost $50 to $200 annually per category and require appraisals or receipts upfront but provide actual protection rather than the $1,500 to $2,500 limits in standard policies.

If you operate any business from home, a business endorsement costs $200 to $500 annually and covers equipment and basic liability. In earthquake-prone areas, earthquake insurance requires commitment-deductibles range from 5 to 25 percent of insured value-but waiting until after a small quake means you cannot obtain coverage.

Review Your Declarations Page Annually

Your declarations page lists exactly what you have and what you don’t, so review it annually and adjust coverage when you renovate, purchase expensive items, or experience weather events in your area. This document becomes your reference point for understanding what protection actually exists under your policy (and what doesn’t). Changes to your home or possessions warrant a conversation with your agent about whether your current endorsements still fit your situation.

Final Thoughts

Building adequate home insurance coverage requires three concrete actions. First, match your dwelling limit to your home’s actual rebuild cost by consulting local contractors, not your home’s market value. Second, select a deductible you can genuinely afford to pay out of pocket without financial strain. Third, add endorsements for gaps specific to your situation-water backup if you have a basement, scheduled personal property for jewelry or art, business coverage if you work from home, and earthquake insurance if you live in a seismic zone.

Your declarations page reveals exactly what protection you have and what you lack. Pull it out today and compare what’s listed against what you actually own and what risks exist in your area-if you’ve renovated, purchased expensive items, or experienced weather events recently, your coverage likely needs adjustment. Most homeowners discover gaps only when filing a claim, which is far too late to add protection.

At North Point Insurance Group, our agents in Alpharetta, Georgia shop 20+ carriers to find coverage that fits your specific situation at competitive rates. We handle the complexity of deductibles, endorsements, and exclusions so you don’t have to, and we provide professional guidance from someone who understands your home and your needs. Contact North Point Insurance Group today to review your current coverage and identify gaps before they cost you thousands.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.