Watercraft Insurance Georgia: Protect Your Boat and Watercraft

Georgia’s boating season brings thousands of residents to lakes, rivers, and coastal waters each year. Whether you own a fishing boat, jet ski, or sailboat, one thing stands between you and financial disaster: watercraft insurance in Georgia.

At North Point Insurance Group, we’ve seen firsthand how a single accident can turn a weekend on the water into a costly nightmare. The right coverage protects your investment and keeps you legally compliant.

Why Watercraft Insurance Matters in Georgia

Georgia’s Boating Landscape and Real Exposure

Georgia’s boating landscape creates real exposure that homeowners policies simply don’t cover. Lake Allatoona draws visitors annually, and the state’s rivers, coastal waters, and smaller lakes host everything from pontoons to personal watercraft year-round. Summer storms in North Georgia bring hail and severe weather that damage boats regularly, while the Intracoastal Waterway and Atlantic coastline expose vessels to saltwater corrosion and offshore risks. This diversity means your coverage needs shift depending on where and how you boat. A fishing boat stored at home near Acworth faces different risks than a jet ski launched at a busy public ramp during peak season.

The Real Cost of Boating Accidents

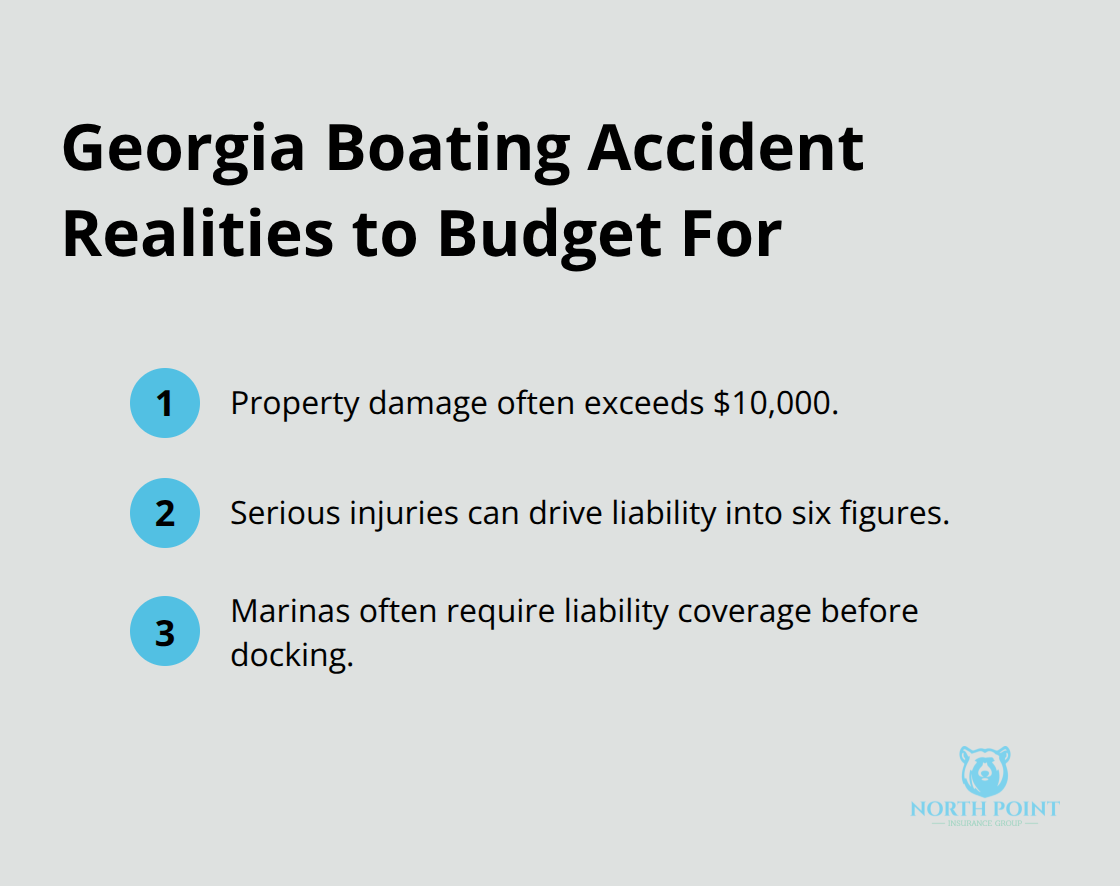

Liability claims from boating accidents escalate quickly in Georgia’s crowded summer conditions. Property damage alone-hitting another boat, a dock, or waterfront property-routinely exceeds $10,000, and serious injuries involving guests or other boaters can push liability costs into six figures. Collisions with other vessels on Lake Allatoona during festival weekends or summer crowds happen more often than many boat owners expect, and without adequate liability coverage, you remain personally responsible for damages.

Medical payments coverage matters equally; if a guest sustains an injury while water-skiing or tubing, their medical bills fall on you without this protection. The state doesn’t legally require boat insurance, but marinas often mandate liability coverage before you dock, and lenders require comprehensive and collision coverage if you financed your boat.

What Georgia Boaters Actually Need

Hull coverage and collision protection defend your boat’s physical structure and equipment from damage, while liability coverage shields your personal assets when you cause injury or damage to others. Uninsured boater coverage fills a critical gap: if another boater hits you and lacks adequate insurance, this coverage pays for your repairs and medical expenses. Agreed value coverage ensures you receive a pre-agreed payout amount if your boat is damaged or totaled, rather than depreciated actual cash value, which matters especially for newer vessels. Add-ons like towing and fuel spill cleanup handle breakdowns and environmental costs that standard policies exclude. Fishing gear coverage protects expensive equipment left on board.

Storage Location and Local Considerations

Boat owners in Acworth and surrounding areas should confirm their storage location-marinas near Cauble Park or Bentwater may qualify for theft-reduction discounts compared to home storage. Your proximity to major roads such as Cobb Parkway and Interstate 75 also influences transport risk and insurance premiums. Local agents who understand Georgia’s boating conditions and your specific lakes or coastal routes can match your policy to your actual exposure rather than leaving you underprotected when an accident occurs. The choice between agreed value and actual cash value reflects your vessel’s true value and depreciation, so this decision requires careful thought about your boat’s current market position and replacement cost.

Coverage That Actually Protects Your Boat

Hull Coverage and Collision Protection

Hull coverage pays for damage to your boat’s structure, engine, and permanently installed equipment when accidents happen-hitting another vessel, striking a dock, or colliding with underwater debris. Collision coverage specifically addresses impact damage and typically carries a deductible ranging from $250 to $1,000, meaning you pay that amount out-of-pocket before your insurer covers the rest. On Lake Allatoona during busy summer weekends, collisions occur regularly enough that this protection isn’t optional.

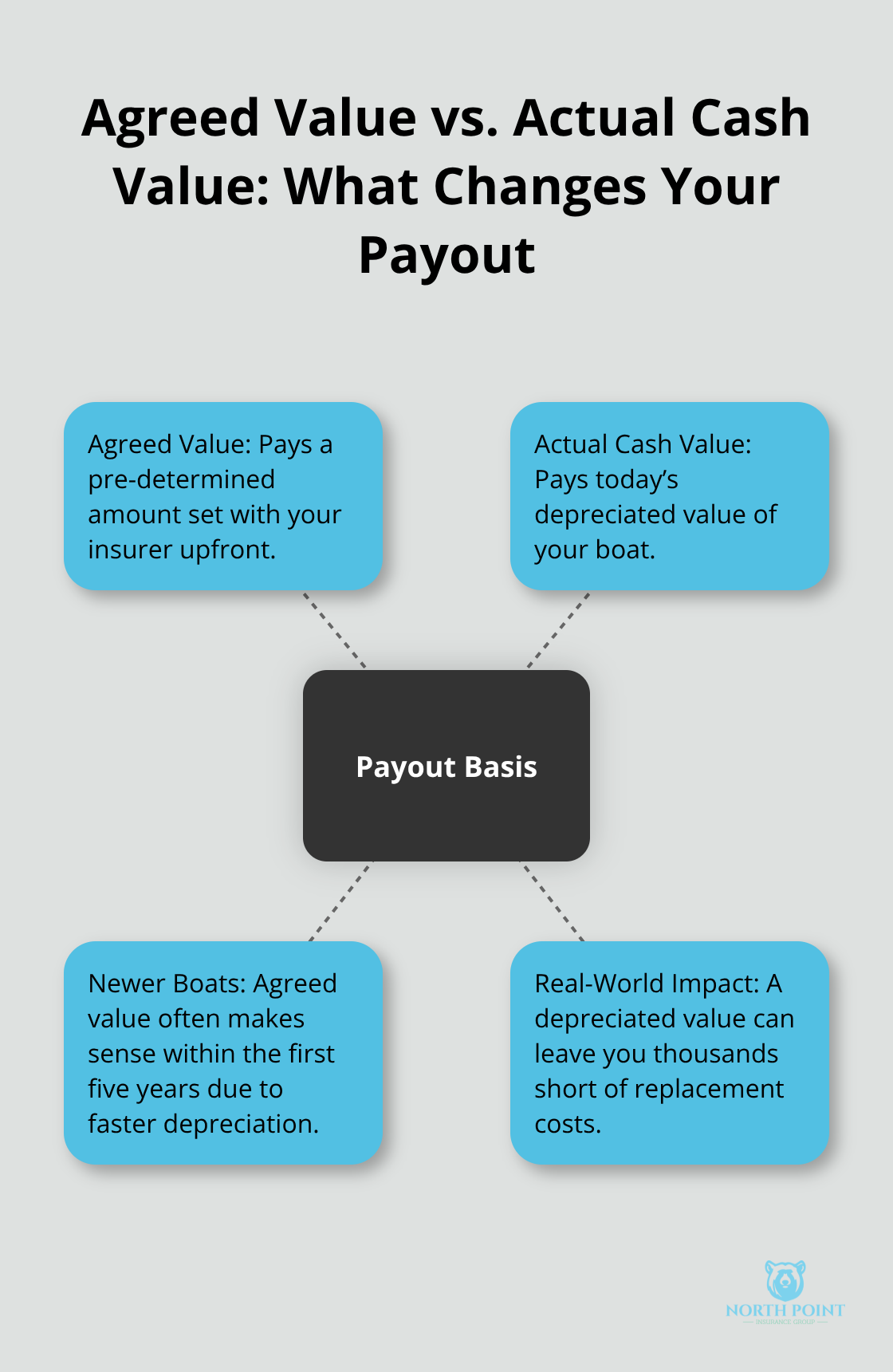

The real decision comes down to agreed value versus actual cash value. Agreed value pays a pre-determined amount you establish with your insurer upfront, while actual cash value pays only what your boat is worth today after depreciation. For boats purchased within the last five years, agreed value makes financial sense because depreciation works against you-a $35,000 boat loses significant value, and actual cash value could leave you thousands short of replacement costs.

Liability Coverage Protects Your Personal Assets

Liability coverage protects your personal assets when you cause injury or property damage to others, and this is where Georgia boaters face genuine exposure. Property damage liability covers the cost when you hit someone else’s boat or damage waterfront property, with damages easily reaching $15,000 to $50,000 in serious incidents. Bodily injury liability covers medical expenses and legal fees if a guest on your boat or an occupant of another vessel sustains injuries, and these costs escalate quickly-a severe water-skiing injury requiring surgery and ongoing care can exceed $100,000.

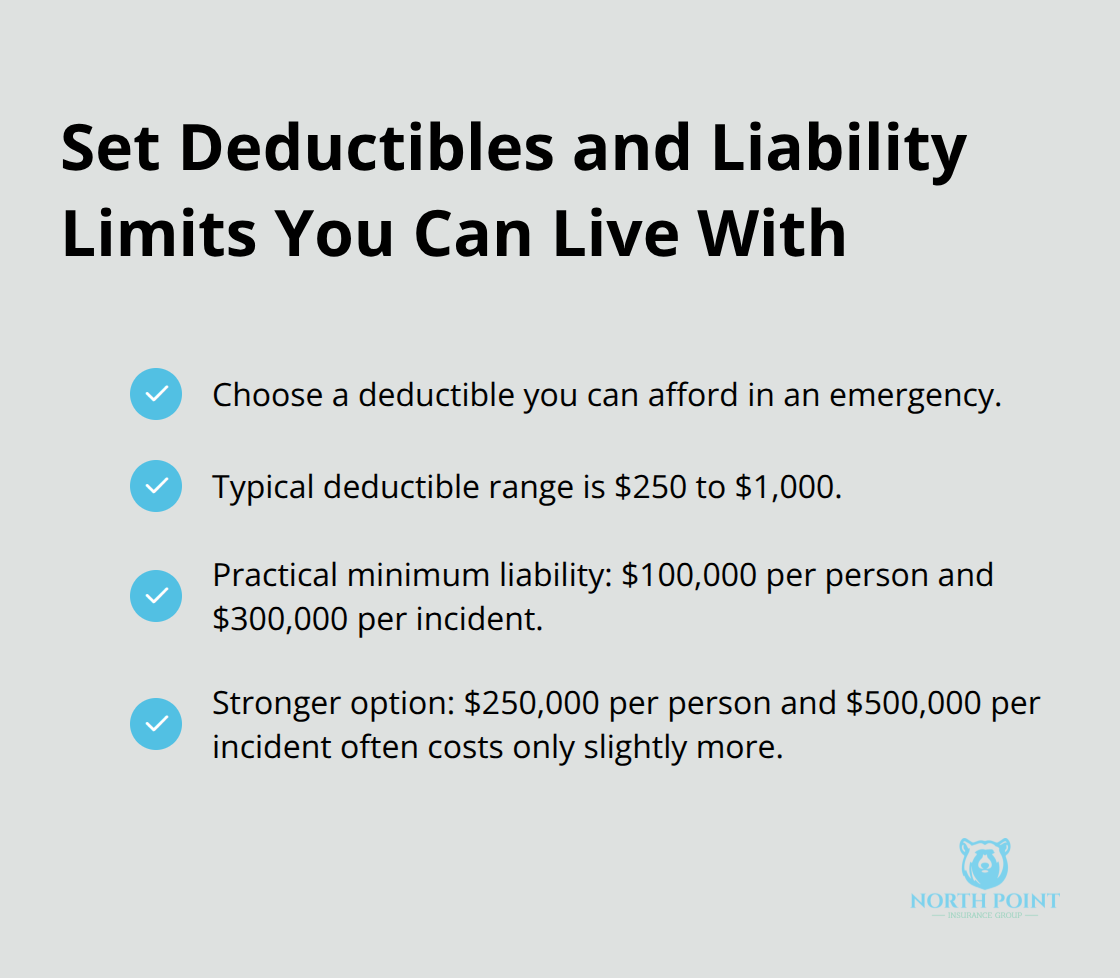

Georgia doesn’t mandate boat insurance by law, but marinas require liability coverage before allowing you to dock, and this requirement exists because accidents happen. Liability limits of $100,000 per person and $300,000 per incident represent a practical minimum for anyone with meaningful assets to protect.

Uninsured Boaters and Medical Payments Coverage

Uninsured boater coverage fills the critical gap when another boater causes damage but lacks adequate insurance to pay for it, covering both your boat repairs and medical expenses. Medical payments coverage operates separately, reimbursing guest injuries regardless of who caused the accident, making it essential if you regularly have family or friends on board.

These two coverages work together to address the reality of Georgia’s busy waterways. A guest sustains an injury while tubing, or another boater hits you without sufficient liability limits-medical payments and uninsured boater coverage step in where the other party’s insurance falls short. Understanding how these layers interact with your primary liability coverage prevents costly gaps when accidents occur on the water.

How to Match Your Policy to Your Boat and How You Use It

Assess Your Boat’s True Current Value

Start with your boat’s actual value, not what you paid five years ago. Check current market listings on sites like NADA Guides or Craigslist to see what similar models sell for today-depreciation cuts deep, and actual cash value policies reimburse only that depreciated amount. A $40,000 boat from 2020 might be worth $28,000 now, so an actual cash value policy would pay you only $28,000 if it’s totaled, leaving you $12,000 short of replacing it. Agreed value locks in a specific payout amount upfront and works better for boats under ten years old. This choice directly affects what you receive after a loss, so understanding the difference between these two approaches matters more than most boat owners realize.

Evaluate Your Usage Patterns and Exposure

Your usage patterns shape which coverages matter most. A pontoon launched weekly during summer on Lake Allatoona during festival weekends faces higher collision risk than a boat stored most of the year. Fishing boats with expensive tackle require fishing gear coverage, while a basic recreational vessel might skip this add-on. Document how often you boat, where you launch, and whether guests regularly come aboard-this information directly shapes which coverages matter most and which you can skip without leaving gaps. A boat entertained with guests faces different liability exposure than one used primarily for solo fishing trips.

Choose Deductibles and Liability Limits That Fit Your Situation

A $500 deductible means you pay that amount out-of-pocket when damage occurs, so select a level you can actually afford in an emergency-most Georgia boaters choose between $250 and $1,000. Liability limits should exceed your net worth by a meaningful margin; if you own a home and have savings, $100,000 per person and $300,000 per incident represent a practical minimum, though $250,000 and $500,000 limits cost only slightly more and provide better protection. The cost difference between adequate and excellent liability protection remains surprisingly small.

Work with Local Agents to Find Competitive Options

Local independent agents who understand Georgia’s waterways and neighborhoods can quote multiple carriers in minutes. These agents ask about your specific storage location, proximity to Lake Allatoona, and whether you trailer your boat, because marinas near Bentwater may qualify for theft discounts while home storage near busy roads like Cobb Parkway might increase premiums. An agent also clarifies which add-ons make sense for your situation: towing protects against breakdowns, fuel spill coverage handles environmental cleanup costs required by law, and watersport coverage reimburses guest medical expenses during water-skiing or tubing up to policy limits. Working with an agent who knows your local area prevents you from overpaying for unnecessary coverage or underpaying and facing gaps when accidents occur.

Final Thoughts

Watercraft insurance in Georgia protects your boat and your financial future when accidents happen on the water. Hull coverage and collision protection defend your boat’s physical structure, while liability coverage shields your personal assets when you cause injury or damage to others. Uninsured boater coverage fills critical gaps when another boater lacks adequate insurance, and medical payments coverage handles guest injuries regardless of fault.

Getting properly insured before the boating season starts matters more than waiting until after an accident occurs. Summer crowds on busy waterways increase collision risk, North Georgia storms bring hail and severe weather damage, and marinas require liability coverage before you dock your boat. Agreed value coverage ensures you receive a pre-agreed payout rather than depreciated actual cash value, protecting your investment in newer vessels.

We at North Point Insurance Group understand Georgia’s boating conditions and can match your policy to your actual exposure rather than leaving you underprotected. Contact us today to get a quote and secure your watercraft insurance before the season starts.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.