Landlord Liability Coverage: Why It Matters

Owning rental property comes with real financial exposure. Tenant injuries, property damage claims, and legal battles can drain your savings fast.

Landlord liability coverage protects you from these costly scenarios. We at North Point Insurance Group help property owners understand what protection they actually need and why standard policies fall short.

What Landlord Liability Coverage Actually Protects

How Liability Coverage Shields Your Finances

Landlord liability coverage protects you from bodily injury and property damage claims that arise from conditions on your rental property. When a tenant slips on a poorly maintained staircase, a guest suffers injury from defective flooring, or someone is harmed by a break-in enabled by inadequate locks, liability coverage pays for medical expenses, legal defense costs, and settlements-potentially saving you tens of thousands of dollars. This protection applies regardless of whether fault is immediately clear, meaning your insurer covers legal defense even during investigation. A serious injury claim can easily exceed $50,000 when medical costs, lost wages, and pain-and-suffering damages combine.

Why Your Homeowners Policy Leaves You Exposed

Standard homeowners policies do not extend protection to rental activity; they are designed for owner-occupied homes and exclude ongoing tenant exposure. Your homeowners policy explicitly excludes rental income and the unique exposures that tenants create. A homeowners insurer will deny a claim if they discover your property is being rented, leaving you personally liable for injuries, damages, and legal fees. If you attempt to rent out a home covered only by homeowners insurance, you risk policy cancellation and zero protection when claims arise.

The Real Difference in Landlord Policies

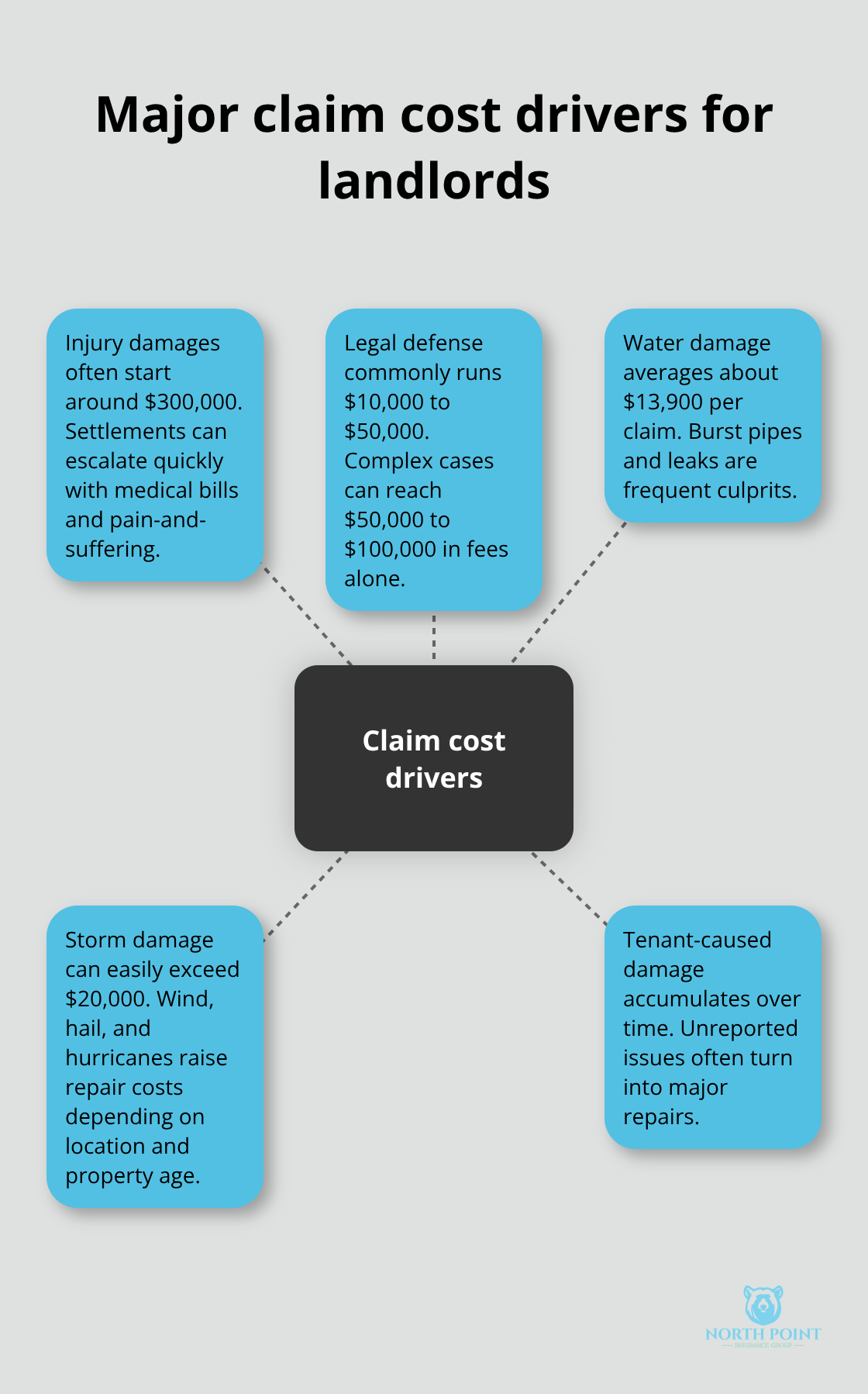

Landlord policies are built specifically for rental properties and include liability limits starting around $300,000 to $500,000 according to the Insurance Information Institute, with higher limits available for multi-unit buildings or properties with amenities like pools. Water damage claims, which average about $13,900 per claim, and storm damage represent common landlord losses, but liability claims from tenant or guest injuries represent a distinct and serious exposure that homeowners insurance ignores entirely. A DP-3 policy offers the broadest liability protection and includes coverage by default, whereas DP-1 and DP-2 policies require you to add liability as an endorsement-a critical distinction when comparing quotes.

Verify Your Coverage Before It’s Too Late

Failing to verify that your DP-1 or DP-2 policy includes liability coverage leaves you completely exposed. An independent agent can review your current policy and identify any gaps between what you think you have and what you actually have. This verification step takes minutes but prevents catastrophic financial exposure when an injury claim arrives at your door.

What Injuries and Damages Cost Landlords

Tenant and Guest Injuries Drain Your Finances Fast

Tenant and guest injuries represent the largest financial threat most landlords never prepare for. A slip on a poorly maintained staircase, a fall caused by defective flooring, or an injury from a break-in enabled by broken locks can trigger significant liability exposure. The Insurance Information Institute reports that liability claims often start at $300,000 in damages, and defending yourself legally costs $10,000 to $50,000 before any settlement is paid. Without liability coverage, you personally cover these expenses from your own pocket, which can force you to sell the property or declare bankruptcy.

Property Damage Claims Add Up Quickly

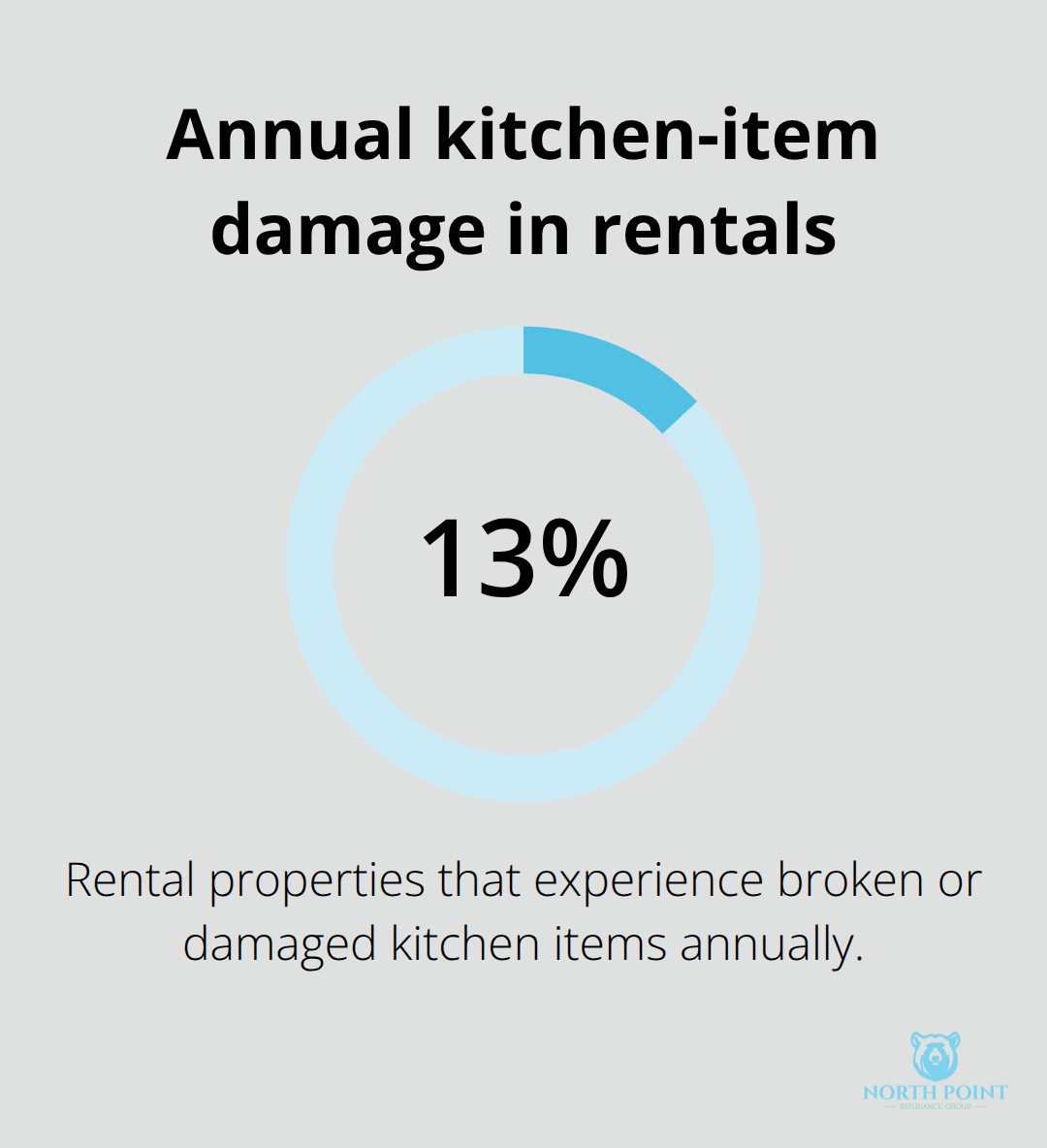

Property damage claims follow a similar pattern and hit your bottom line hard. Water damage from burst pipes or leaking plumbing averages about $13,900 per claim according to industry data, while storm damage from wind, hail, or hurricanes can easily exceed $20,000 depending on your location and property age. Tenant-caused damage represents another constant drain that catches many landlords off guard. About 13% of rental properties experience broken or damaged kitchen items annually, affecting roughly 5.59 million rental homes nationwide, and these damages accumulate quickly when tenants fail to report issues until major repair work becomes necessary.

Legal Defense Costs Escalate Rapidly

Legal defense costs pile up regardless of whether you win or lose a case. Your insurer covers attorneys, court filings, investigation expenses, and expert witnesses only if you have proper liability coverage in place. Without it, you hire your own lawyer at $200 to $400 per hour and hope to recover costs later, which rarely happens. A modest injury claim that goes to trial costs $15,000 to $30,000 in legal fees alone, and complex cases with multiple injuries or property damage can run $50,000 to $100,000.

Geographic Location Amplifies Your Exposure

Landlords in high-risk states like California, Florida, and New York face even steeper exposure because juries in these areas award higher damages and courts impose stricter liability standards on property owners. The Insurance Information Institute notes that lawsuits against landlords are increasing, making liability protection less optional and more essential. Failing to carry liability coverage transforms a manageable insurance claim into a personal financial disaster that affects your credit, your other assets, and your ability to own rental property in the future. These real costs make understanding your coverage options the next critical step in protecting your investment.

Choosing the Right Liability Limits for Your Property

Match Your Liability Limits to Your Actual Exposure

Selecting proper liability limits starts with understanding what your property actually exposes you to, not what sounds reasonable. The Insurance Information Institute recommends liability limits starting around $300,000 to $500,000 for standard rental properties, but this baseline assumes a single-family home with minimal amenities and low injury risk. Multi-unit buildings, properties with pools or gyms, or rental homes in high-litigation states like California, Florida, and New York demand significantly higher limits because juries in these jurisdictions award larger damages and courts hold landlords to stricter liability standards. A serious injury claim involving permanent disability or death easily exceeds $500,000 when medical costs, lost wages, pain-and-suffering damages, and legal fees combine.

Ask yourself three hard questions to assess your exposure: How many units do you own? Does your property have amenities that increase injury risk? What is your state’s typical damage award range for slip-and-fall or premises liability cases?

Your answers determine whether $300,000 suffices or whether you need $1 million or more in protection.

Consider Umbrella Policies for Multiple Properties

If you own multiple properties, an umbrella liability policy covering several million dollars across all your rentals simplifies management and provides genuine protection against catastrophic claims that exceed underlying policy limits. Umbrella policies cost far less than you might expect and fill critical gaps that standard landlord policies leave open. This approach consolidates your liability protection and ensures that a single major claim does not wipe out your entire rental portfolio.

Balance Deductibles Against Your Cash Reserves

Deductibles matter far more than most landlords realize because they directly affect your out-of-pocket costs when claims happen. A $1,000 deductible sounds manageable until water damage from burst pipes averages $13,900 per claim, leaving you responsible for the first $1,000 and your insurer covering the remainder.

Raising your deductible to $2,500 or $5,000 reduces your annual premium significantly, but you must have cash reserves available to cover that amount immediately when a claim occurs. Many landlords make critical mistakes here: they select low premiums with high deductibles they cannot actually afford to pay. This strategy backfires when a claim arrives and you lack the cash to cover your deductible while waiting for your insurer to reimburse you.

Compare Quotes and Verify Coverage Details

Compare quotes across multiple carriers because premium differences for the same coverage often exceed 30%, and verify exactly what each policy excludes before committing. Exclusions for tenant-business activities, intentional acts, or professional services unrelated to the rental property can create dangerous gaps in coverage. Ask your agent directly whether your DP-1 or DP-2 policy includes liability coverage as standard or requires adding it as an endorsement, because this distinction alone can mean the difference between $300,000 in protection and zero protection when injury claims arrive.

Premium differences matter, but coverage gaps matter more. A cheap policy with excluded scenarios leaves you exposed to the exact losses you thought you had covered. Take time to read policy definitions for key terms like occurrence, bodily injury, and property damage so you understand what your insurer actually covers. An independent agent can review your options and explain how each policy responds to your specific property risks.

Final Thoughts

Landlord liability coverage protects your finances from the injuries and damages that can destroy your rental business. Without it, a single slip-and-fall claim or property damage lawsuit forces you to pay tens of thousands of dollars from your own pocket, threatening your ability to keep your properties and maintain your financial stability. The real cost of being uninsured far exceeds the premium you pay for proper protection.

Verify what coverage you currently have before a claim arrives at your door. If you own rental property under a homeowners policy, that coverage will be denied the moment a claim arises. If you have a DP-1 or DP-2 policy, confirm that liability coverage is included rather than optional, because many landlords discover too late that they selected the cheapest policy without realizing liability was excluded entirely.

Work with an independent agent who understands rental property risks and can compare multiple carriers on your behalf when you are ready to secure proper coverage. We at North Point Insurance Group work with landlords across Georgia and beyond to build landlord liability coverage that protects your investments without overpaying for unnecessary features. Contact us for a quote and let our local agents review your current coverage to identify any gaps before a claim forces you to face them alone.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.