Car Insurance Policy Explanations: Key Terms and Coverage

Car insurance policies are filled with terms and coverage options that confuse most drivers. You might think you’re fully protected, but gaps in your coverage could leave you vulnerable after an accident.

At North Point Insurance Group, we’ve helped thousands of customers understand their policies and find the right protection. This guide breaks down the essential terms and coverage types so you can make informed decisions about your insurance.

What Actually Protects You in Your Car Insurance Policy

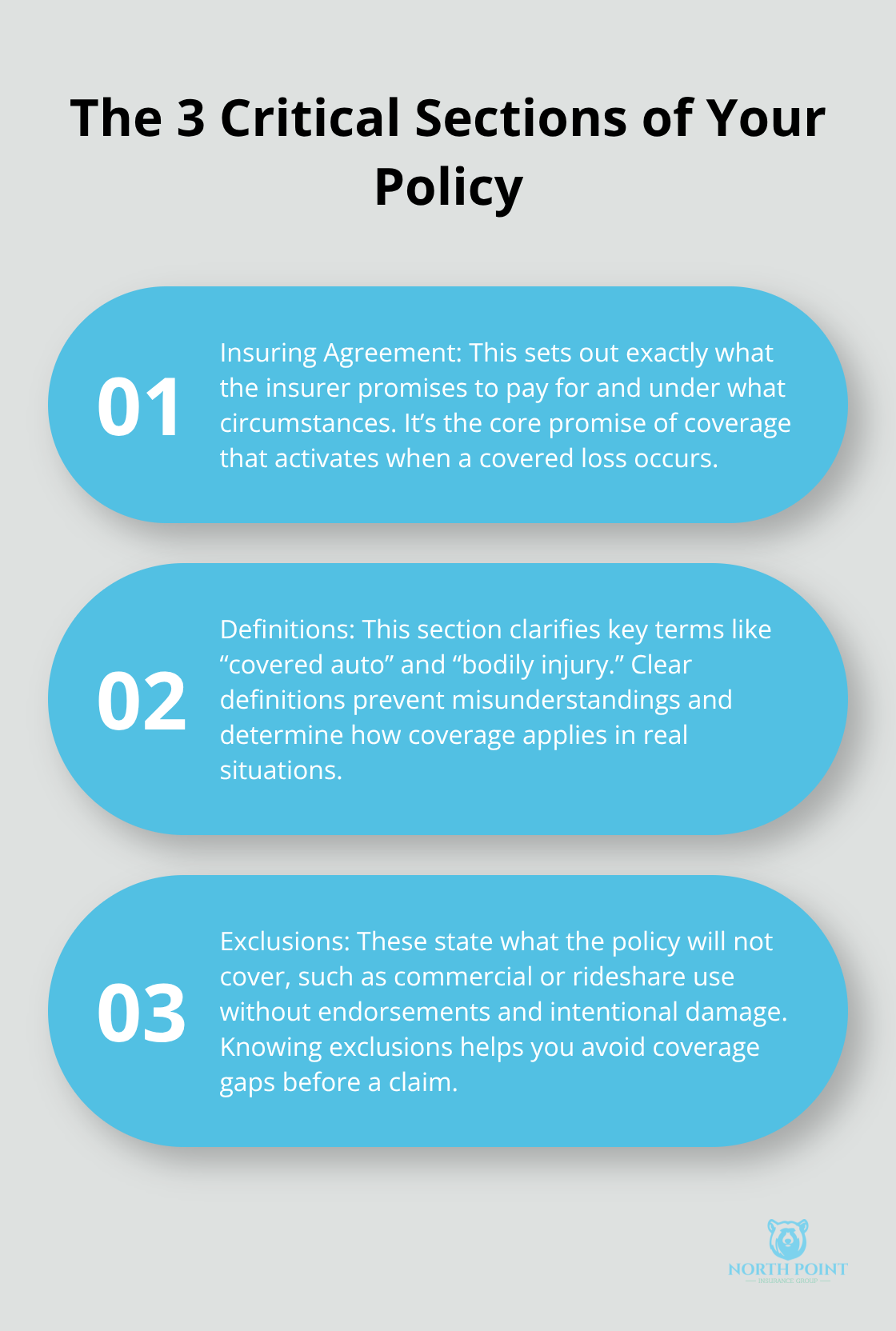

Your car insurance policy is a contract between you and your insurer that outlines exactly what risks they’ll cover and under what conditions. Most drivers never read beyond the declarations page, which is where the real problem starts. The policy itself contains three critical sections: the insuring agreement that spells out what the company will pay for, the definitions section that clarifies terms like “covered auto” and “bodily injury,” and the exclusions that detail what isn’t covered. Without understanding these sections, you might assume you’re protected when you’re actually facing gaps. Standard personal auto policies explicitly exclude commercial driving, rideshare services without proper endorsements, and intentional damage.

If you drive for Uber or Lyft without adding rideshare coverage, a claim during a ride will be denied entirely. The declarations page lists your coverage types and limits, but it doesn’t explain what those limits mean in real dollars. A 15/30/5 liability limit in California means you have $15,000 per person and $30,000 total for injuries you cause, plus only $5,000 for property damage. That $5,000 property limit covers damage to someone else’s vehicle or property-one accident with a newer car can easily exceed that amount, leaving you personally liable for thousands.

How Deductibles Shape What You Actually Pay

The deductible is the amount you pay out of your own pocket before your insurance kicks in, and it’s one of the most misunderstood parts of a policy. A higher deductible lowers your premium, sometimes significantly, but only if you can actually afford to pay it when a claim happens. If you set a $1,000 deductible to save $20 per month but your emergency fund has $800, you’ve created a false economy. Raising your deductible from $500 to $1,000 can reduce your premium by 10 to 15 percent depending on your insurer and driving record. The real strategy involves matching your deductible to your financial situation. If you have savings to cover a $1,000 claim, that deductible makes sense. If not, a $500 deductible is worth the extra premium because you won’t end up in debt after an accident. Collision and comprehensive coverage both have separate deductibles, so you could pay $500 for collision damage and another $500 for comprehensive damage if both occur. Your deductible also applies to subrogation situations where your insurer recovers money from the at-fault party-your deductible gets included in that recovery before you see any money back.

Understanding Premium Rates and Cost Drivers

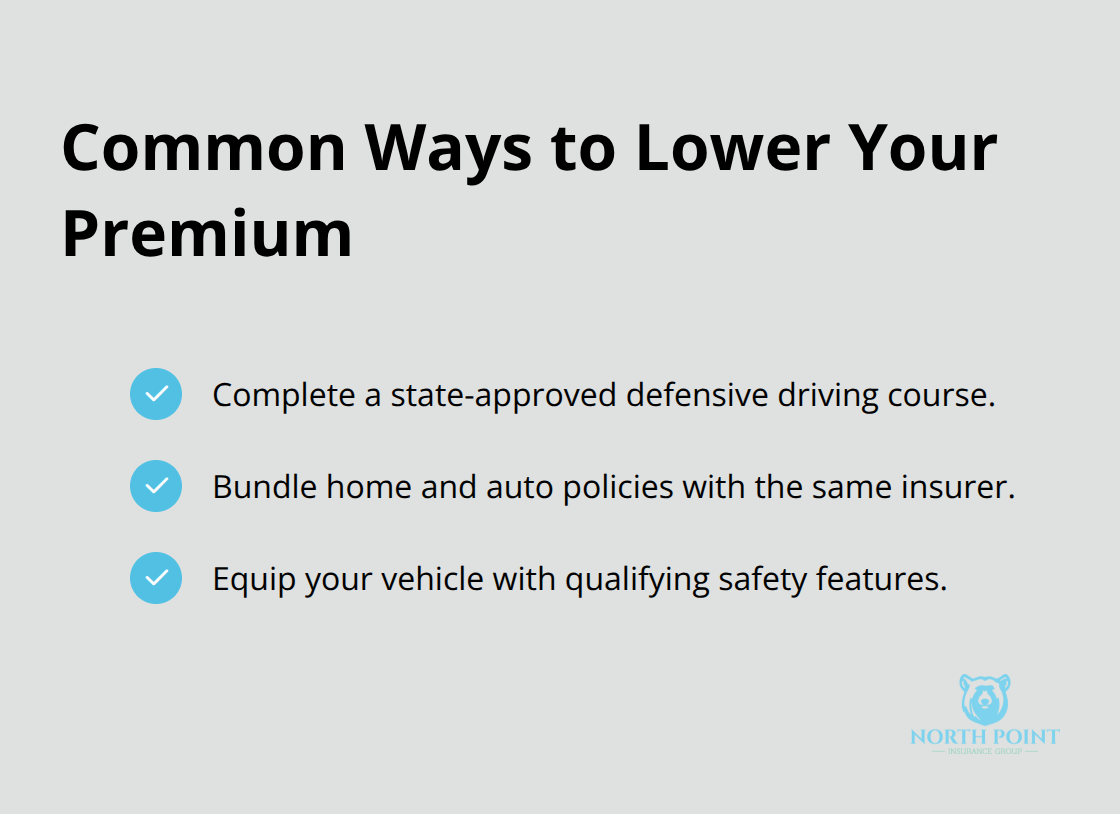

Your premium isn’t random-it’s calculated based on specific factors that insurers use to predict claim likelihood. Driving record carries the heaviest weight; a single at-fault accident can increase your premium by 25 to 40 percent depending on severity, while moving violations add surcharges that vary by infraction type. Age matters significantly because drivers under 25 and over 65 statistically file more claims. Vehicle type affects cost too-a sports car costs more to insure than a sedan because repair and medical costs run higher after accidents. Where you live changes everything; urban drivers pay more than rural drivers due to higher accident frequency and theft rates. Some insurers use credit-based insurance scores, which correlate with claims likelihood, so a lower credit score can raise your premium even if you’ve never had an accident. Different insurers weight these factors differently-one company might penalize age heavily while another focuses on driving record. A 35-year-old with one accident five years ago might receive a better quote from one carrier than another by 30 percent or more. Discounts like defensive driver courses, bundling home and auto policies, and safety features on your vehicle can reduce premiums by 5 to 25 percent each. The mistake most drivers make is accepting the first quote without shopping around or asking about available discounts.

When you compare quotes across multiple carriers, you’ll often find significant price differences for identical coverage, which is why shopping matters more than accepting whatever your current insurer offers.

The Coverage Types That Actually Protect You

Why Liability Limits Matter More Than You Think

Liability coverage is mandatory in every state, yet most drivers carry the bare minimum required by law rather than what actually protects their assets. California requires 15/30/5, meaning $15,000 per person for bodily injury, $30,000 total per accident for bodily injury, and $5,000 for property damage. That $5,000 property limit is dangerously low-repair costs for a newer vehicle easily exceed this amount, leaving you personally responsible for the difference. If you cause an accident that injures two people and damages their vehicle, California’s minimum coverage becomes insufficient within seconds.

Carrying at least 100/300/50 limits protects your personal assets significantly better and costs only slightly more than minimums. Medical bills from a serious accident routinely exceed $50,000, and if you’re liable, the injured party can pursue your wages and savings through a lawsuit. Bodily injury liability covers medical expenses, lost wages, pain and suffering, and legal defense costs for injuries you cause to others. Property damage liability pays for repairs or replacement of someone else’s vehicle or property. The difference between state minimums and adequate coverage often costs $10 to $20 monthly-a minimal price for protecting yourself from financial devastation.

Collision and Comprehensive: Protecting Your Own Vehicle

Collision and comprehensive coverage protect your own vehicle rather than others. Collision pays for damage when you hit another vehicle or object, regardless of fault, while comprehensive covers non-collision events like theft, vandalism, fire, hail, and animal strikes. Most lenders require both coverages if you’re financing your vehicle, which means skipping them isn’t actually an option for financed cars.

The critical decision involves your deductible amount on each coverage type. A $500 collision deductible costs more monthly than a $1,000 deductible, but you’ll pay $500 out of pocket after any collision claim versus $1,000. If your vehicle is worth $8,000 and you have a $1,500 deductible on collision, you’re accepting significant financial risk-a claim would require you to pay 19 percent of your vehicle’s value before insurance covers the rest.

Uninsured and Underinsured Motorist Protection

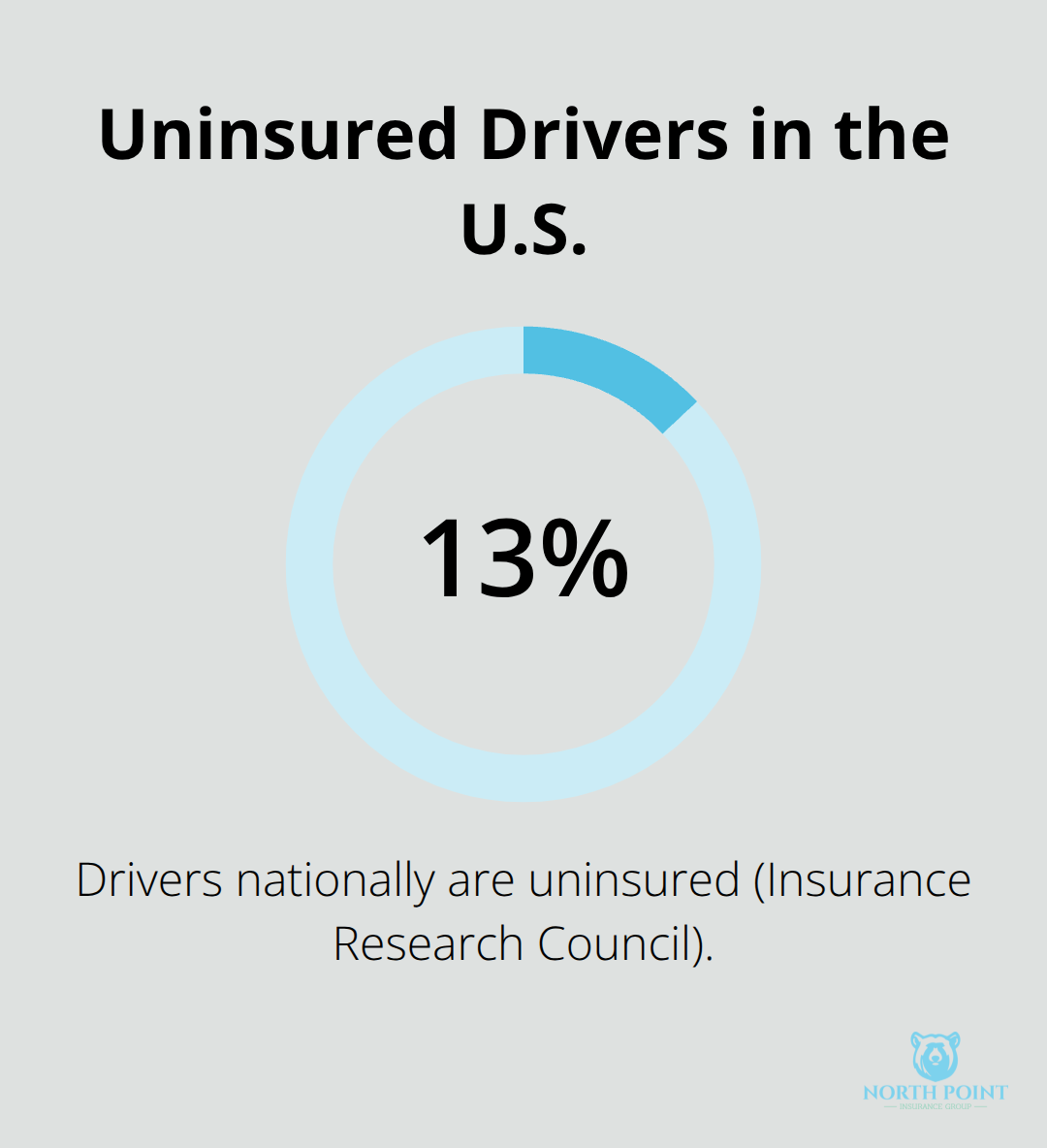

Uninsured motorist coverage protects you when the at-fault driver has no insurance, while underinsured motorist coverage applies when their limits are insufficient for your damages. These coverages should match your bodily injury liability limits whenever possible-if you carry 100/300 liability limits, your uninsured motorist limits should also be 100/300. Approximately 13 percent of drivers nationally are uninsured according to the Insurance Research Council, meaning roughly one in eight vehicles on the road carries no coverage.

A hit-and-run accident where the other driver flees leaves you dependent entirely on uninsured motorist coverage to pay for injuries and vehicle damage. Setting your uninsured motorist limits lower than your liability limits creates a gap where you’re better protected against harming others than protecting yourself. Understanding these gaps in your coverage becomes essential before you face a claim, which is why reviewing your declarations page and policy terms matters far more than most drivers realize.

What Your Declarations Page Actually Tells You

Your declarations page is the single most important document in your policy, yet most drivers glance at it once and never look again. This page shows your policy number, coverage limits, deductibles, premium amount, and the vehicles covered under your policy. The declarations page lists the specific dollar amounts for each coverage type-if it says 100/300/50, that’s your actual liability protection, not some theoretical number.

Verifying Your Vehicle Information and Coverage Details

Check that every vehicle listed matches what you actually drive. A common mistake occurs when someone buys a new car but forgets to update their policy; the new vehicle won’t be covered under your existing declarations page until you contact your agent and receive an updated version. Your deductible amounts appear here separately for collision and comprehensive, so you know exactly what you’ll pay out of pocket. If the declarations page shows a $1,000 collision deductible and $500 comprehensive deductible, those are two different amounts you might owe after separate claims.

Endorsements also appear on the declarations page-if you added rideshare coverage or rental reimbursement, it will be listed here. Missing endorsements create dangerous gaps; many drivers assume they have coverage they never actually purchased. The premium breakdown shows what you’re paying for each coverage type, revealing whether your costs align with your protection level. A $25 monthly policy with 15/30/5 liability limits is dangerously cheap because you’re underprotected, not because you found a great deal.

Understanding Policy Renewal Deadlines

Policy renewal deadlines appear in your declarations page, and missing this date can result in coverage lapsing entirely. Most policies renew every six to twelve months, and your insurer sends renewal notices at least 30 days before expiration. If you ignore the renewal notice and your policy lapses, you’re driving uninsured and risking serious legal consequences. Some states impose license suspension and fines for driving without active coverage, even for a single day.

Identifying Exclusions and Limitations

Exclusions and limitations represent the most dangerous part of your policy because they define what isn’t covered, yet most drivers never read this section. Standard personal auto policies exclude commercial use, which means if you deliver packages for a gig economy service without commercial coverage, a claim during that delivery will be denied. Named driver exclusions prevent specific people from driving your vehicle and remaining covered by your policy; if you excluded a teenage driver to lower your premium and they drive your car anyway, any accident they cause won’t be covered.

Your policy also excludes intentional damage, so if you cause damage deliberately rather than accidentally, you can’t file a claim. Understanding these exclusions before you need them prevents devastating surprises after an accident. When you work with an independent agent (such as those at North Point Insurance Group), they review these exclusions with you during the application process to identify gaps and add proper coverage rather than discovering problems after a loss occurs.

Final Thoughts

Car insurance policy explanations matter because understanding your coverage prevents costly mistakes after an accident. Most drivers never review their policies beyond the initial purchase, which means they operate with incomplete information about what actually protects them. The declarations page shows your limits and deductibles, but only reading the full policy reveals exclusions that could deny your claim, and a single serious accident can exceed state minimums within moments, leaving you personally liable for tens of thousands of dollars.

Reviewing your policy for gaps requires checking three specific things: verify that your declarations page lists all vehicles you currently drive and that coverage limits match your actual risk exposure, read the exclusions section to identify situations where coverage won’t apply (rideshare driving, commercial use, and named driver exclusions are the most common gaps), and compare your uninsured motorist limits to your liability limits to eliminate protection imbalances. After major life events like buying a new car, paying off a loan, or adding a teenage driver, your coverage needs change and your policy should be updated accordingly.

At North Point Insurance Group, our local agents in Alpharetta, Georgia shop 20+ carriers to find coverage that actually fits your needs rather than just the cheapest option available. We review your declarations page, identify exclusions that create gaps, and recommend endorsements that fill those gaps with proper protection. Working with an independent agent means someone explains what your coverage actually means in real dollars and helps you make informed decisions about deductibles and limits based on your financial situation, not just your monthly budget.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.