Boat Insurance Coverage Explained: Understanding Protection

Boat owners face real risks on the water, and the wrong insurance policy can leave you exposed when you need protection most. We at North Point Insurance Group know that boat insurance coverage explained clearly helps you make smarter decisions about what actually protects your vessel and passengers.

Most boat owners don’t realize how many gaps exist in standard policies until something goes wrong. This guide walks you through the coverage types that matter, what affects your rates, and the protection holes you need to fill.

Types of Boat Insurance Coverage

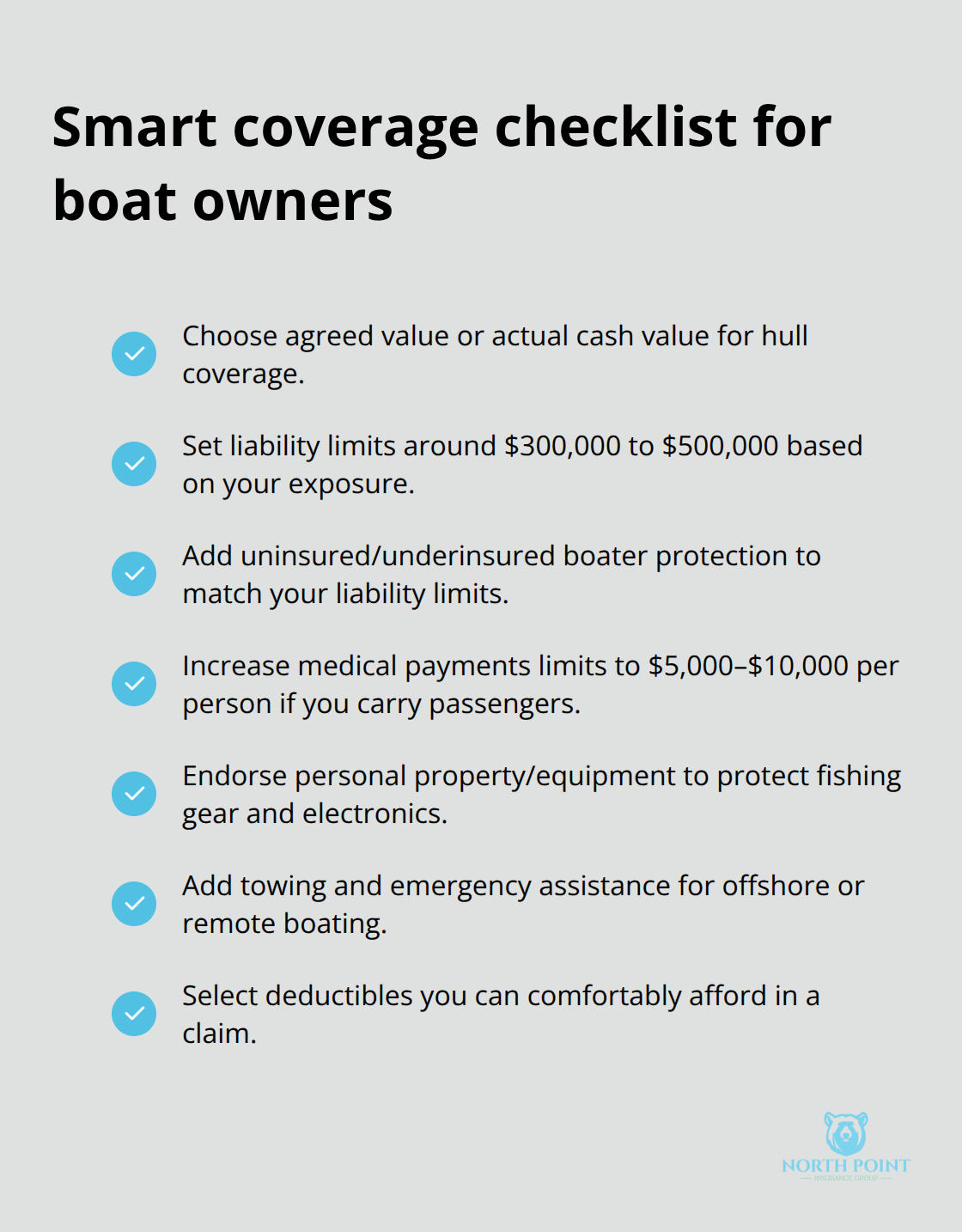

Liability coverage forms the foundation of any boat insurance policy, and it’s the one coverage most states require you to carry. This coverage pays for damages or injuries you cause on the water-damage to someone else’s dock, another boat, or injuries to passengers and other boaters. If you hit someone’s boat and cause $50,000 in damage, your liability coverage covers it. Most boat owners carry $300,000 to $500,000 in liability protection, which is smart given that a serious injury claim can easily exceed $100,000.

Watersports create additional liability exposure since passengers who tube, wakeboard, or waterski can suffer serious injuries. Your policy should explicitly cover these activities. Liability also covers wreck removal and disposal costs, which can run $10,000 to $50,000 depending on your boat size and location. Under federal law, vessel operators face liability exposure up to $939,800 for oil pollution cleanup, so adequate liability limits matter far more than most boat owners realize.

Hull Coverage Protects Your Actual Boat

Collision and comprehensive coverage together form what’s called hull coverage, and this is where most boat owners get confused about what’s actually protected. Collision coverage pays for damage from hitting another boat, dock, or submerged object, and it covers capsizes too. Comprehensive coverage handles everything else-theft, vandalism, fire, storms, lightning, and falling trees. If a hurricane damages your boat while it’s docked, comprehensive pays for repairs minus your deductible. If you sink in deep water, comprehensive covers the wreck removal.

Standard deductibles range from $500 to $2,500, with some policies allowing 1% to 5% of your boat’s insured value. The key decision is whether you choose agreed value or actual cash value. Agreed value policies pay a fixed amount you set at policy start, so your new $80,000 boat stays insured for $80,000 even if the market value drops.

Actual cash value policies pay current market value minus depreciation, which means a five-year-old boat worth $50,000 new might only be worth $30,000 in a total loss claim. Agreed value costs more but protects you from depreciation surprises.

Uninsured and Underinsured Boater Protection Fills a Real Gap

Uninsured and underinsured boater coverage protects you and your passengers if another boater hits you but lacks adequate insurance. This coverage actually matters more than many boat owners think. Not every boater carries insurance, and some carry minimal limits. If an uninsured boater causes $75,000 in damage to your boat and injures a passenger, your uninsured boater coverage picks up the claim. You can typically select limits matching your liability coverage-$300,000 to $500,000 is reasonable.

Medical Payments and Passenger Protection

Medical payments coverage is separate and pays for actual medical bills for you and your passengers regardless of fault, which means it applies even if you caused the accident. Medical payments limits typically range from $1,000 to $5,000 per person. For serious boating activities or boats that regularly carry passengers, higher medical payments limits prevent out-of-pocket medical costs from becoming a financial problem.

The coverage types you select directly influence what your rates will be, and understanding how boat characteristics and your personal boating profile affect those rates helps you make smarter decisions about where to allocate your insurance budget.

Factors That Affect Your Boat Insurance Rates

Your boat’s characteristics and personal profile determine roughly 80% of what you’ll pay for coverage, and understanding these factors lets you make strategic decisions about where to cut costs without sacrificing protection.

Boat Type, Age, and Value Shape Your Premium

Boat type matters significantly-a 25-foot center console fishing boat costs far less to insure than a 35-foot speedboat or luxury yacht because repair and replacement costs are lower. A new $150,000 boat will cost more to insure than a 10-year-old $60,000 model, but the relationship between boat value and premium isn’t linear. Annual boat insurance typically costs 1% to 5% of the boat’s value, which means a $50,000 boat might run $500 to $2,500 per year depending on coverage selections and other factors.

Boat age and condition directly affect premiums too-insurers often require a recent marine survey before quoting older boats, and a well-maintained 15-year-old vessel costs less to insure than a neglected 8-year-old one. The condition of your boat matters as much as its age when insurers calculate your rate.

Your Boating Experience and Claims History

Your boating experience and claims history create the second major cost driver, and insurers weight this heavily because experience reduces accident risk. First-time boat owners typically pay 15% to 25% more than experienced operators, and completing a boating safety course through Boat-Ed or a state-approved provider can lower your premium by 5% to 15% depending on your insurer.

A clean claims history matters enormously-one prior claim increases premiums 10% to 30%, while multiple claims can make coverage difficult or expensive to obtain. Your track record on the water directly influences what insurers charge you.

Location and Storage Create Dramatic Cost Differences

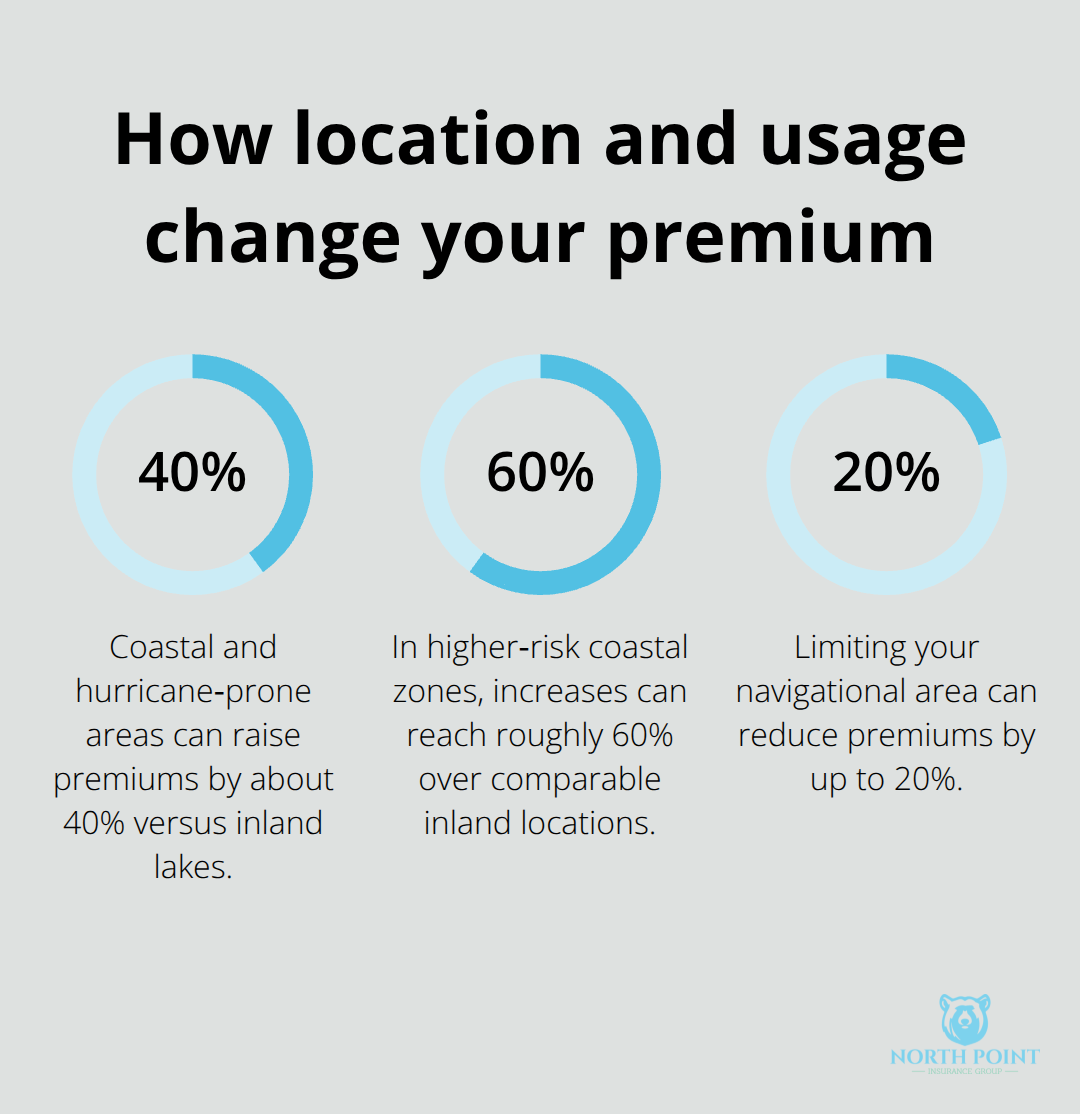

Location determines the final piece of the pricing puzzle, and this is where geography creates dramatic cost differences. Coastal properties and hurricane-prone areas see premiums 40% to 60% higher than inland lake locations because storm damage and salt water exposure increase claim frequency. A boat moored in Miami costs substantially more to insure than the same boat stored on an inland lake in Georgia.

Where you actually operate your boat also matters-limiting your navigational area to the specific lakes or waters where you boat can reduce premiums by 10% to 20% compared to policies allowing unlimited navigation. Boats stored in covered slips or boathouses cost less than those left exposed to weather, and this protection translates directly into lower rates since comprehensive claims drop significantly.

Deductibles and Coverage Choices Control Your Costs

Deductible selection offers direct control over premium costs-choosing a $2,500 deductible instead of $500 typically saves 15% to 25% on your annual premium, though you absorb more risk in smaller claims. The coverage types you select directly influence what your rates will be, and understanding how boat characteristics and your personal boating profile affect those rates helps you make smarter decisions about where to allocate your insurance budget.

These rate factors reveal why two identical boats can have vastly different premiums-one owner’s location, experience, and coverage choices might cost half what another owner pays. The gaps that remain in standard policies, however, often surprise boat owners when claims actually happen.

Common Gaps in Boat Insurance Policies

Most boat owners discover coverage gaps only after filing a claim, and that’s when the financial damage extends far beyond what the policy covers. Standard boat insurance policies protect your hull and liability exposure, but they leave significant protection holes that can cost thousands in out-of-pocket expenses.

Equipment and Personal Belongings Require Separate Coverage

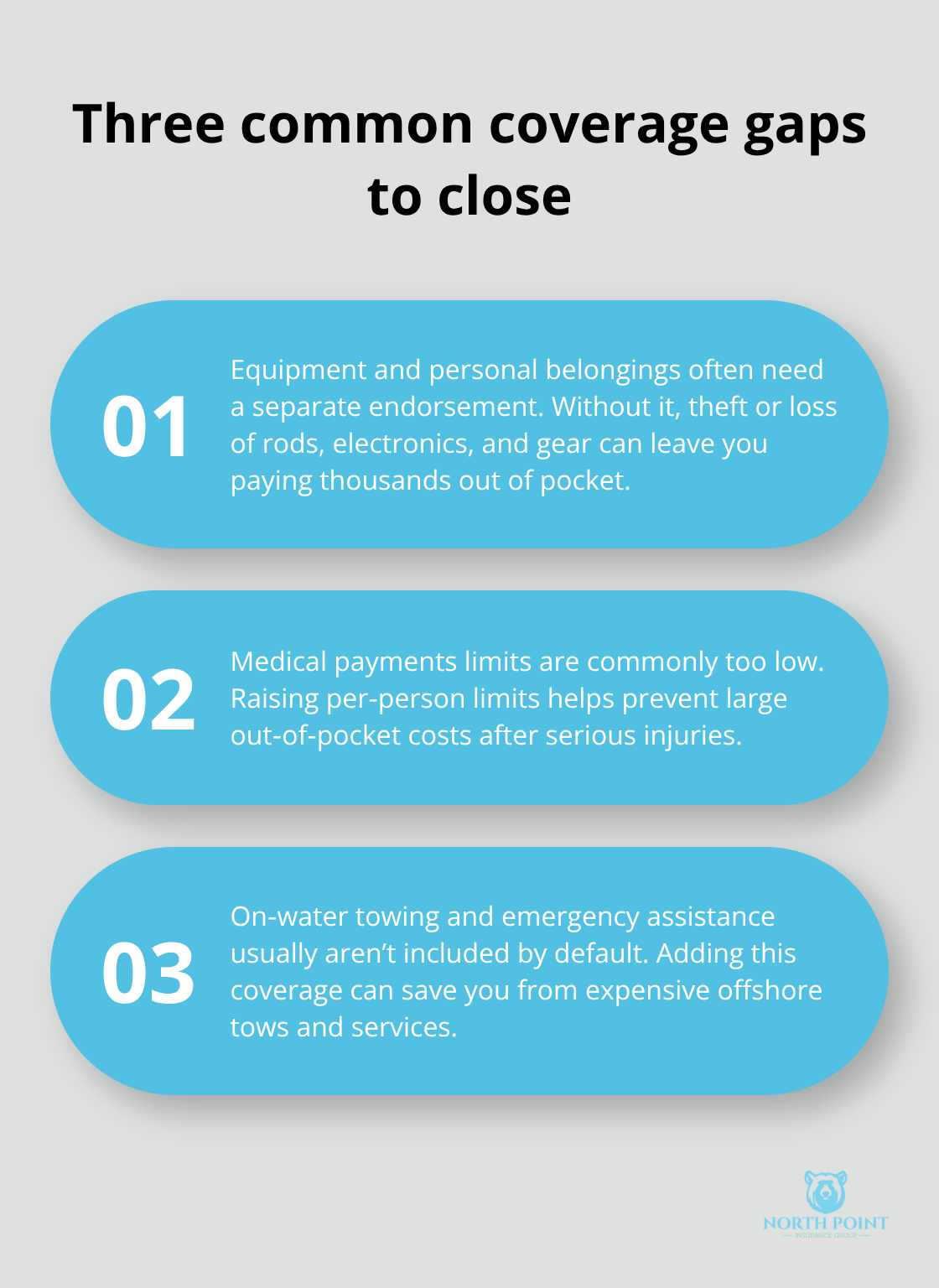

Your fishing rods, marine electronics, scuba gear, and personal belongings aboard your boat typically aren’t covered under standard hull policies unless you add personal property or equipment coverage as a separate endorsement. A $3,000 GPS chartplotter, $2,500 in fishing equipment, and $1,500 in personal electronics can vanish in a theft or accident, and your base policy won’t reimburse a cent without that specific protection. This gap matters most for serious anglers and water sports enthusiasts who carry expensive gear regularly.

Some insurers offer coverage for fishing equipment or carry-on items lost or stolen, but you must request this endorsement explicitly-it doesn’t come standard. The cost to add personal property coverage typically runs 1-2% annually, a small price compared to replacing thousands in gear.

Medical Payments Limits Fall Short in Serious Injuries

Medical payments coverage presents another significant gap that boat owners overlook until someone gets injured. Your medical payments limit might be $2,500 per person, but a serious head injury or spinal damage can generate $50,000 to $150,000 in medical costs within hours.

If you carry four passengers regularly, a $2,500 per-person limit means your policy caps total medical coverage at $10,000 for an incident involving all four people.

That $10,000 exhausts quickly when emergency room visits, CT scans, and helicopter evacuation costs mount up. Higher medical payments limits-$5,000 to $10,000 per person-cost relatively little to add but prevent catastrophic out-of-pocket exposure for you and your passengers.

Towing and Emergency Assistance Coverage Costs Extra

On-water towing and emergency assistance coverage also disappears in many standard policies, which means if your engine fails 10 miles offshore, you’re paying $1,500 to $3,000 out of pocket for professional towing back to harbor. Some insurers offer towing coverage that covers fuel delivery, jump starts, and mechanical labor, but you must request this endorsement specifically.

The combination of these three gaps-equipment coverage, inadequate medical limits, and missing towing protection-creates real financial vulnerability that most boat owners don’t address until it’s too late.

Final Thoughts

Boat insurance coverage explained clearly shows that protection gaps exist in nearly every standard policy, and addressing those gaps before you need a claim prevents financial disaster. The foundation starts with liability coverage that meets your state’s requirements and your actual exposure-most boat owners benefit from $300,000 to $500,000 in limits given the cost of serious injuries and property damage on the water. Hull coverage through collision and comprehensive protection keeps your vessel safe from both accidents and weather, while uninsured boater coverage fills the gap when another operator lacks adequate insurance.

Your personal situation determines which additional coverages matter most. If you regularly carry passengers or engage in water sports, medical payments limits of $5,000 to $10,000 per person prevent catastrophic out-of-pocket costs. If you own expensive fishing equipment or marine electronics, personal property coverage protects thousands in gear that standard policies ignore. If you boat far from shore or in remote areas, on-water towing coverage becomes practical protection rather than optional luxury.

Comparing quotes from multiple insurers reveals dramatic differences in both price and coverage quality. One insurer might charge $1,200 annually for basic coverage while another offers comprehensive protection for $950, and the cheaper option often excludes towing or limits medical payments to inadequate levels. We at North Point Insurance Group understand that boat insurance decisions require balancing protection against cost, and our local agents shop multiple carriers to find coverage that matches your actual boating profile and budget.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.