Student Driver Insurance Georgia: Tips for Savvy Student Drivers

Student driver insurance in Georgia comes with its own set of rules and costs. Getting behind the wheel as a young driver means navigating coverage requirements, premium rates, and discounts that differ from standard policies.

At North Point Insurance Group, we’ve helped countless student drivers find affordable coverage that actually protects them. This guide walks you through Georgia’s specific insurance landscape and shows you how to cut costs without cutting corners.

What Georgia Requires and Why It Matters for Student Drivers

Georgia’s Minimum Coverage and Real Costs

Georgia’s minimum liability insurance is 25/50/25, meaning $25,000 per person for bodily injury, $50,000 total per accident, and $25,000 for property damage. This baseline is the legal floor, not a recommendation. The average Georgia driver pays about $1,298 per year for full coverage, but student drivers in Georgia average roughly $5,760 annually. CDC data show teen drivers are nearly three times more likely than drivers over 20 to be involved in a fatal crash, which explains why insurers charge significantly higher premiums for young drivers.

How Age and Vehicle Choice Impact Your Rate

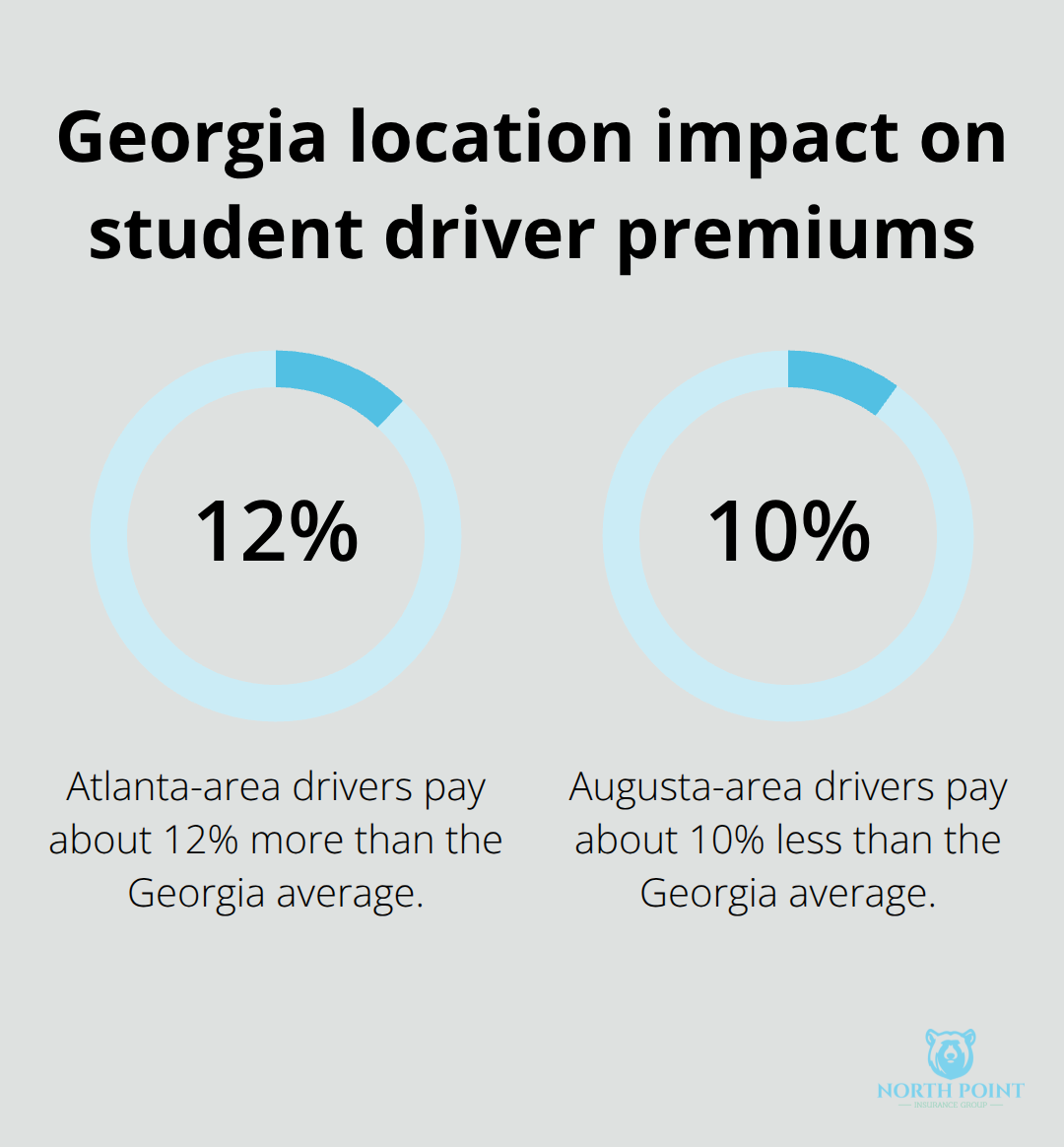

Age hits your wallet hard. A 16-year-old pays substantially more than an 18-year-old, and both pay more than a 21-year-old because insurers view driving experience as the strongest predictor of safety. Male student drivers typically face higher premiums than female peers at the same age. Your vehicle choice matters too-a safe, reliable sedan costs less to insure than a sports car or older model. Location within Georgia also shifts rates; Atlanta-area drivers pay roughly 12% more than the state average due to congestion and theft risk, while Augusta-area drivers pay about 10% less.

Discounts That Actually Reduce Your Premium

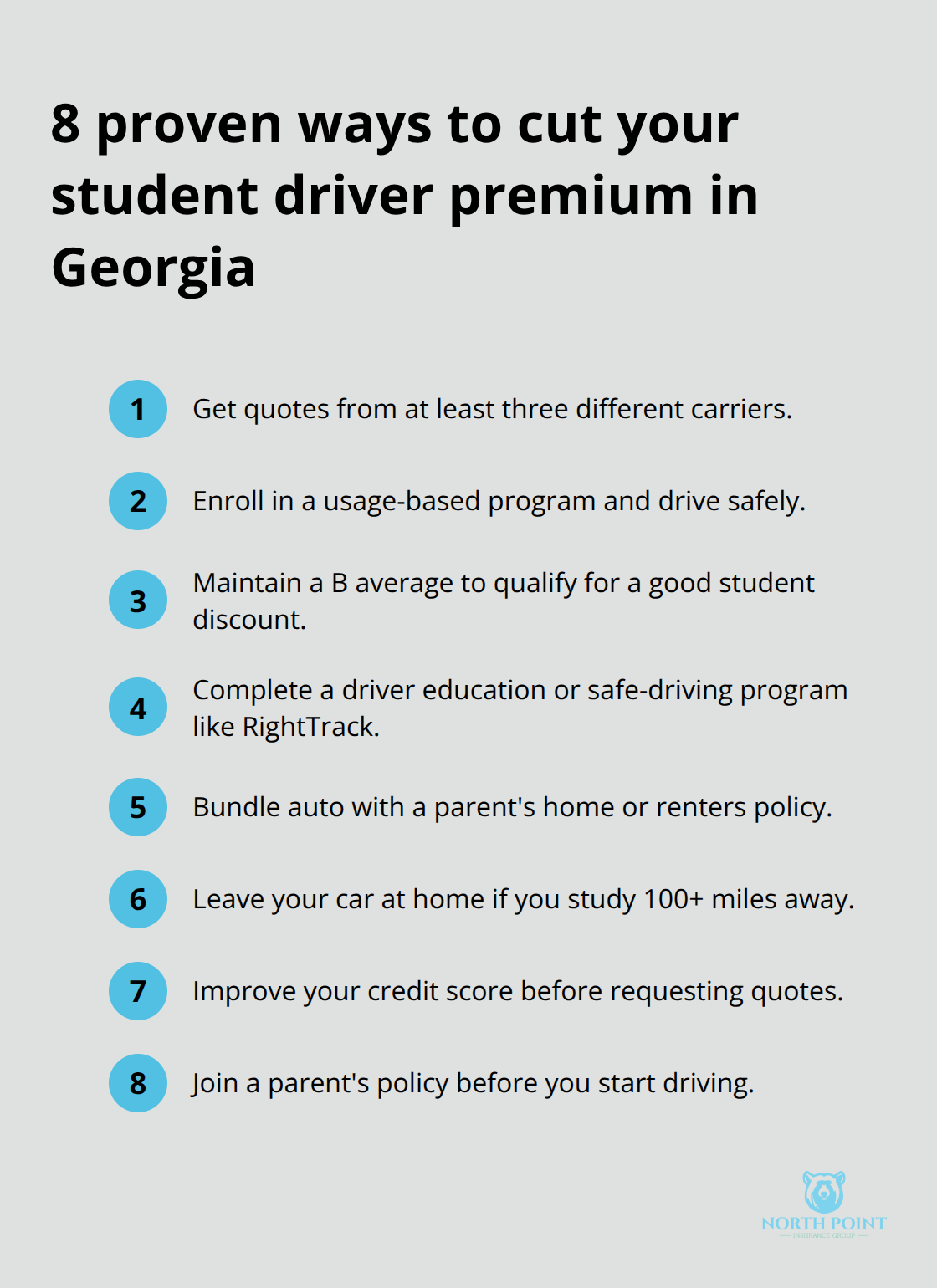

Good grades open real savings doors. A good student discount rewards students under 25 who maintain a B average or better, reducing premiums by 15-25%. Completing a driver education course or a safe driving program like RightTrack can deliver up to 30% savings and provides feedback on your actual driving habits. Bundling auto with a parent’s home or renters policy typically saves 10-15% on both policies. If you study more than 100 miles away and leave your car at home, an away-at-school discount applies.

The Power of Comparison Shopping and Credit

The most powerful move is comparison shopping-quotes from at least three different carriers typically save 30-50%. Telematics programs monitor your actual driving behavior and reward safe habits with 15-40% discounts if you maintain clean driving records. Credit score affects rates too; good credit can lower premiums by up to about 60% compared to poor credit. These discounts stack, so combining good student status with bundling and a safe-driving program creates the biggest impact on your annual cost.

Now that you understand what Georgia requires and where savings hide, the next step is learning which mistakes student drivers make that can erase those savings or leave them dangerously underinsured.

How to Cut Your Student Driver Insurance Costs

The gap between what you’re paying and what you could pay is often massive. Student drivers who take three specific actions consistently save 30-50% on their annual premiums, yet most never bother trying.

Shop Multiple Carriers Without Wasting Hours

Stop accepting the first quote you receive. Insurance companies price identically-qualified drivers differently based on their own risk models and underwriting rules. One carrier might view your driving record as low-risk while another penalizes you heavily for the same history. Getting quotes from at least three carriers is non-negotiable if you want competitive rates.

Independent agencies shop 20+ carriers at once, which means you see real price differences without spending hours on individual insurer websites. This approach eliminates the tedious process of visiting each company’s site separately and gives you leverage to negotiate better terms.

Prove Your Safe Driving Habits With Usage-Based Programs

Usage-based insurance programs monitor how you drive through a mobile app or device, and safe drivers earn 15-40% discounts by proving they follow speed limits, avoid hard braking, and stay off roads during high-risk hours. Programs like RightTrack go further by giving you real-time feedback on specific driving habits, turning your phone into a coaching tool that both saves money and makes you a safer driver.

This approach works because insurers reward measurable behavior. You control the outcome directly-drive safely, and your premium reflects that reality.

Stack Discounts Deliberately for Maximum Savings

Good student discounts combine with bundling your auto policy to a parent’s home or renters policy (10-15% savings on both) and away-at-school discounts when you leave your car home. Combining these discount types can reduce your total annual cost significantly.

Credit score matters too; good credit cuts rates by up to 60% compared to poor credit, so if your score is weak, improving it before requesting quotes pays real dividends.

Act on Timing Before Your Coverage Starts

The timing of these moves matters. Report changes to your insurer immediately-adding yourself to a parent’s policy costs less than getting your own policy, but only if you do it before you need coverage. Waiting until after you pass your driving test or after an accident eliminates negotiating power and locks you into worse rates.

These cost-cutting strategies work only when you implement them before coverage gaps appear. The next step involves understanding what happens when student drivers ignore these savings opportunities and make costly mistakes that no discount can fix.

Common Mistakes Student Drivers Make on Insurance

Most student drivers in Georgia carry one of three fatal gaps in their understanding of insurance. These mistakes cost money, create legal exposure, and leave you dangerously unprotected when accidents happen.

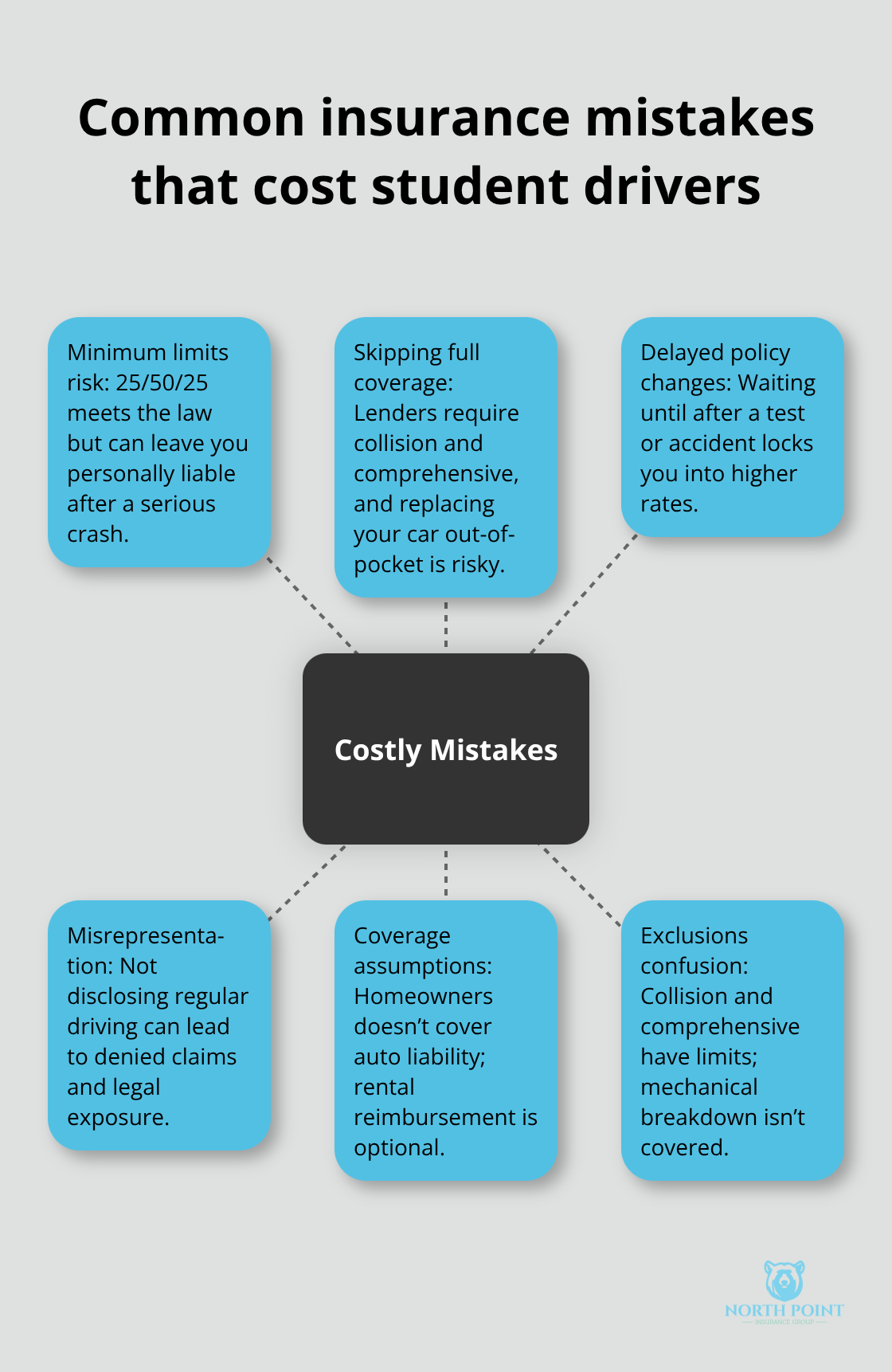

Minimum Coverage Leaves You Personally Liable

Georgia’s 25/50/25 minimum liability satisfies the law but leaves you dangerously exposed if you cause a serious accident. A single collision involving another vehicle and injuries can easily exceed $50,000 in damages, which means you pay anything beyond your coverage limits out of your own pocket. Teen drivers are nearly three times more likely than drivers over 20 to be involved in a fatal crash, yet many student drivers keep liability at the legal minimum and skip collision and comprehensive coverage entirely.

If you finance or lease a vehicle, your lender requires collision and comprehensive anyway. If you own the car outright, you face a harder choice: accept the risk of losing your vehicle completely in an accident, or upgrade your coverage. Upgrading from minimum liability to full coverage adds about $900 per year in premium, but that cost pales against a $150,000 judgment against you personally.

Delayed Policy Changes Lock You Into Higher Rates

Reporting changes to your policy immediately matters far more than most student drivers realize. Adding yourself to a parent’s policy costs substantially less than obtaining your own coverage, but only if you report it before you start driving. Waiting until after you pass your driving test or after an accident eliminates your negotiating power and locks you into worse rates.

Insurance companies can also deny claims if they discover you misrepresented your driving situation. Hiding the fact that you’re now a regular driver on the vehicle creates legal exposure beyond just higher premiums. The company may refuse to pay for damages, leaving you liable for the full amount.

Your Policy Covers Less Than You Think

Many student drivers assume their parents’ homeowners policy covers liability when they cause an accident, but it doesn’t-auto liability is separate. Others think their policy covers rental cars automatically, when in fact rental reimbursement is an optional add-on. Collision coverage doesn’t apply to single-vehicle accidents on private property in some cases, and comprehensive coverage specifically excludes mechanical breakdown.

The only way to know what you’re actually protected against is to read your policy documents or ask your agent directly. An independent agent can explain coverage in plain language so you understand exactly what happens when you file a claim. Getting these three details right before you drive prevents expensive gaps that no discount can fix.

Final Thoughts

Student driver insurance Georgia requires three concrete actions to get right. Shop at least three carriers to find rates that match your actual risk profile, not just the first quote you receive. Stack discounts deliberately by combining good student status, bundling with a parent’s home policy, and enrolling in a usage-based program like RightTrack. Upgrade beyond Georgia’s minimum 25/50/25 liability to full coverage if you can afford it, since teen drivers face three times the crash risk of older drivers and minimum coverage leaves you personally liable for damages that exceed those limits.

The gap between what most student drivers pay and what they could pay is substantial. Implementing these strategies before you start driving locks in lower rates and prevents the costly mistakes that erase savings. Delayed policy changes, misunderstandings about what your coverage actually protects, and driving with inadequate limits create legal and financial exposure that no discount can fix after the fact.

An independent agent shops multiple carriers at once, identifies discounts you’d miss on your own, and ensures your coverage matches your actual situation. Contact North Point Insurance Group to get accurate quotes and clear answers about what student driver insurance Georgia actually costs when you shop smart.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.