Auto Coverage Basics: Understanding Your Policy

Most drivers don’t fully understand what their auto policy actually covers. This gap in knowledge often leads to surprises when claims happen or to paying for coverage you don’t need.

At North Point Insurance Group, we’ve seen firsthand how confusion about auto coverage basics costs people money and leaves them exposed to risk. This guide walks you through the essential components of your policy so you can make informed decisions about your protection.

What Your Auto Policy Actually Covers

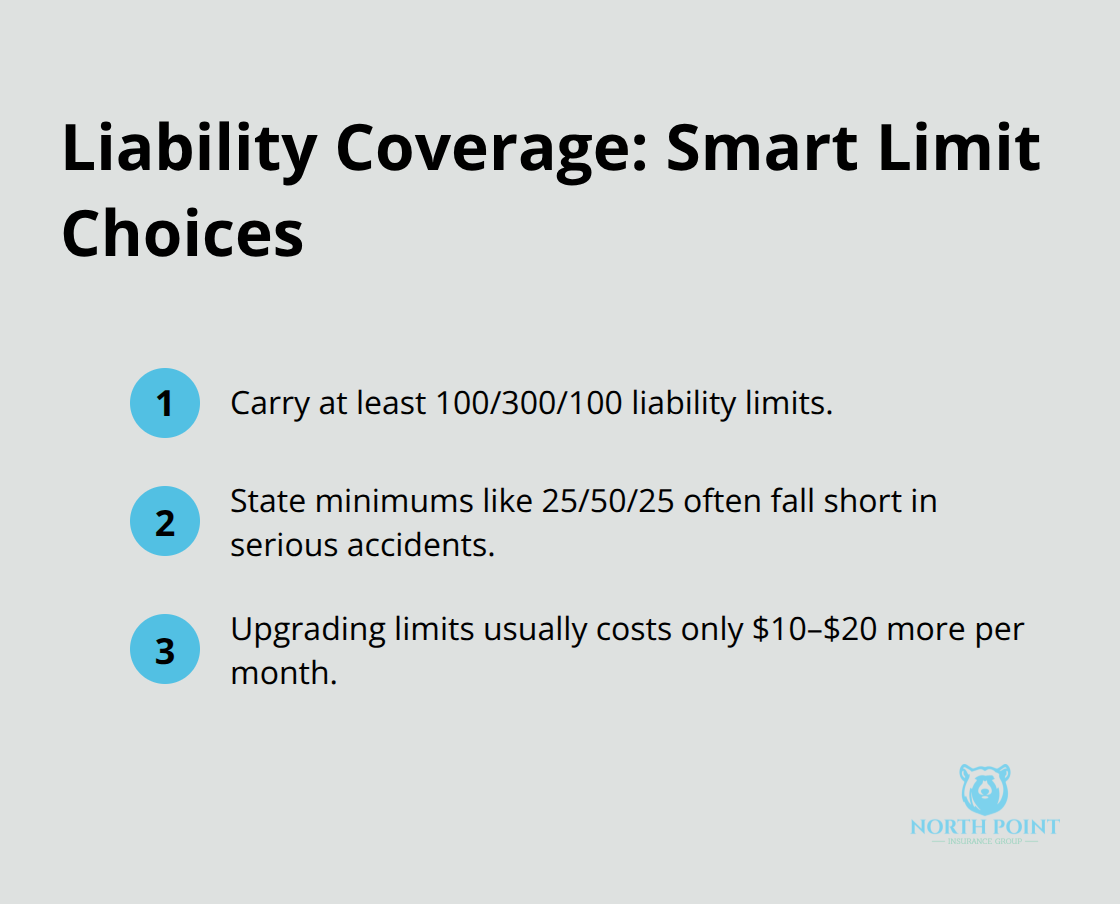

Your auto policy is a contract that protects you from financial losses tied to car-related risks, but most drivers only understand the parts that matter after something goes wrong. Liability coverage forms the foundation-it pays for injury or damage you cause to others, and most states legally require it. According to the National Association of Insurance Commissioners, typical liability splits include bodily injury per person, bodily injury per accident, and property damage limits. A common baseline is 25/50/25, meaning $25,000 per person and $50,000 per accident for bodily injury, plus $25,000 for property damage. However, this minimum often falls short in serious accidents. If you cause a collision that injures multiple people or damages expensive property, state minimums won’t cover the full costs, and the liability becomes yours personally.

Try carrying higher limits than your state requires-at least 100/300/100-because the difference in premium is minimal, usually $10 to $20 per month, while your asset protection increases significantly.

Collision and Comprehensive: Protecting Your Vehicle

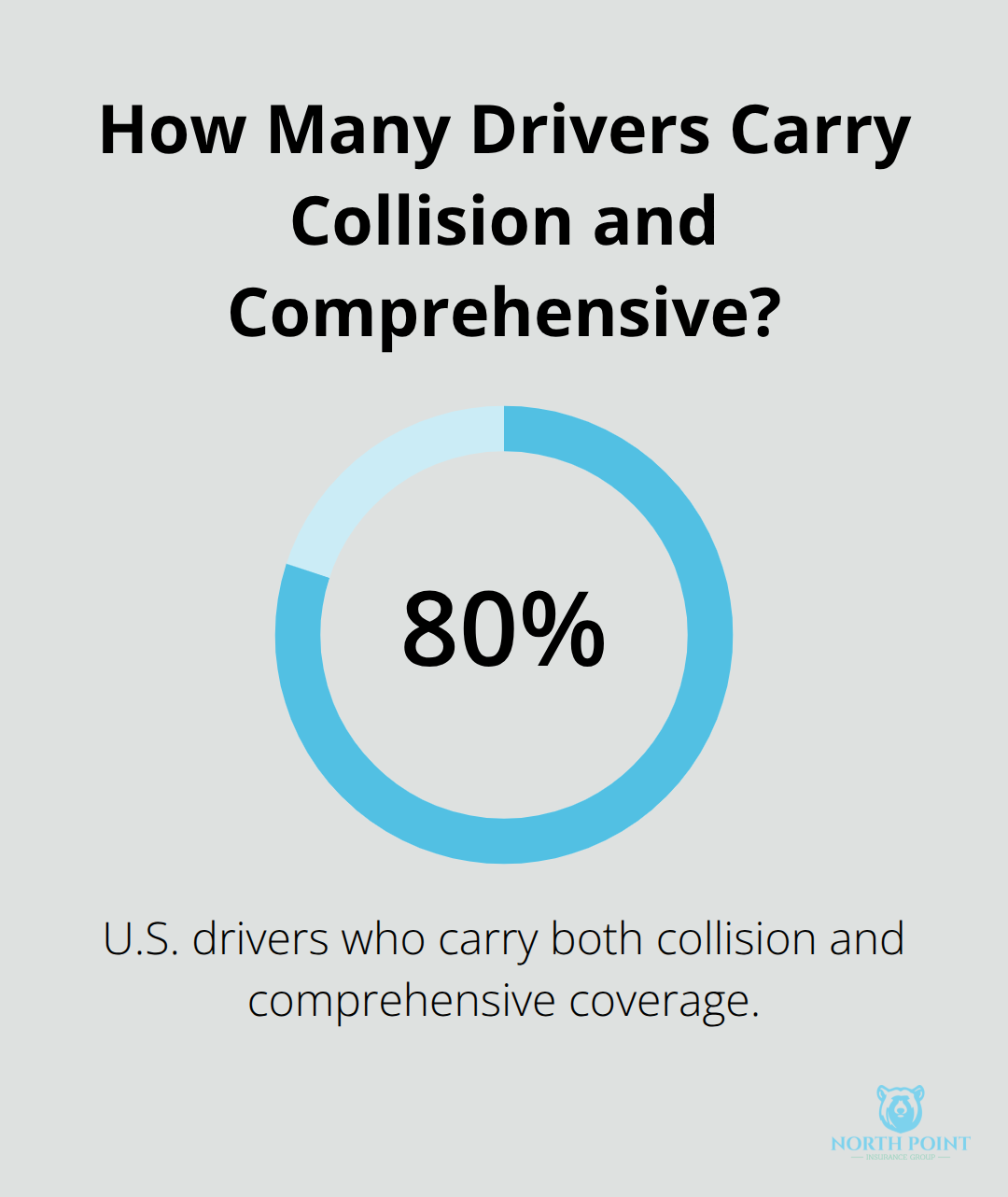

Collision coverage pays to repair or replace your own car after hitting another vehicle or object, while comprehensive covers non-collision damage like theft, vandalism, weather, fire, and animal strikes. Both are optional in most states, but if you’re financing or leasing your vehicle, your lender requires them. The Insurance Information Institute reports that about 80 percent of U.S. drivers carry both coverages, which reflects how essential they are for newer vehicles. Deductibles for these coverages typically range from $500 to $1,000, and you pay this amount out of pocket before your insurer covers the rest.

For example, if a deer damages your car and repair costs $3,000 with a $500 deductible, you pay $500 and your insurer covers $2,500. Comprehensive coverage often includes windshield damage, though some policies offer separate glass coverage with zero deductible-a smart choice if your area experiences frequent hail or debris damage.

Uninsured and Underinsured Motorist Coverage

Uninsured motorist coverage protects you when the at-fault driver carries no insurance or insufficient coverage, which happens more often than most people realize. According to the National Association of Insurance Commissioners, this coverage should match your liability limits-if you carry 100/300/100 liability, carry at least 100/300 uninsured motorist coverage. Many drivers skip this protection to save money, but that’s a serious mistake. If an uninsured driver causes a collision that injures you or damages your vehicle, you’re left with no recovery unless you have uninsured motorist protection. Underinsured motorist coverage fills the gap when the at-fault driver’s insurance limits are too low to cover your damages. Both coverages include property damage protection, which covers damage to your vehicle in a hit-and-run or collision with an uninsured driver. The cost of adding or increasing these coverages is typically $15 to $30 per month, making it one of the most affordable ways to close a critical protection gap.

Now that you understand what your policy covers, the next piece of the puzzle involves how deductibles work and why they have such a direct impact on both your monthly costs and your out-of-pocket expenses when a claim occurs.

How Deductibles Work and Why They Matter

A deductible is straightforward: it’s the amount you pay out of pocket when you file a claim, and your insurer covers everything above that amount. If your comprehensive or collision claim totals $3,000 and your deductible is $500, you pay $500 and your insurer pays $2,500. This applies to each claim separately, not annually, so if you file two claims in one year, you pay the deductible twice. Deductibles typically range from $100 to $2,000, with $500 being the most common choice among drivers.

How Deductibles Affect Your Monthly Costs

The higher your deductible, the lower your monthly premium. Raising it from $250 to $1,000 can reduce your annual costs by $200 to $400 depending on your location and driving record. Conversely, lowering your deductible increases your premium. This trade-off sits at the core of your decision: will you pay more monthly to reduce what you’d owe in a claim, or do you prefer lower premiums and higher out-of-pocket costs if something happens?

Matching Your Deductible to Your Situation

Your deductible choice should reflect two realities: what you can actually afford to pay if a claim occurs, and how likely you are to file one. If you have $2,000 in emergency savings and a clean driving record, a $1,000 deductible makes sense because you’re unlikely to need it and the premium savings are substantial. If you live in an area prone to hail damage or you have a longer commute with higher accident risk, a lower $500 deductible protects you from surprise expenses.

Some insurers now offer disappearing deductibles-your deductible decreases or disappears entirely after a set period without claims or violations-which rewards safe driving over time. Glass coverage deserves special attention: if your area experiences frequent hail or flying debris, paying slightly more for zero-deductible windshield coverage prevents the frustration of paying $250 to $500 out of pocket for a cracked windshield.

Comparing Deductibles Across Quotes

When shopping for coverage, comparing deductibles across quotes matters as much as comparing premiums. A policy with a $500 premium but $1,000 deductible isn’t necessarily cheaper than one at $550 with a $500 deductible if you end up filing a claim. Run the numbers based on your actual situation-your vehicle’s age, your driving habits, and your financial cushion-rather than picking a deductible because it sounds reasonable.

The deductible you select directly shapes what happens when you actually need your coverage. Understanding this connection prepares you to spot the gaps that many drivers overlook-the protections that sound optional but can save you thousands when the unexpected occurs.

Coverage Your Policy Might Be Missing

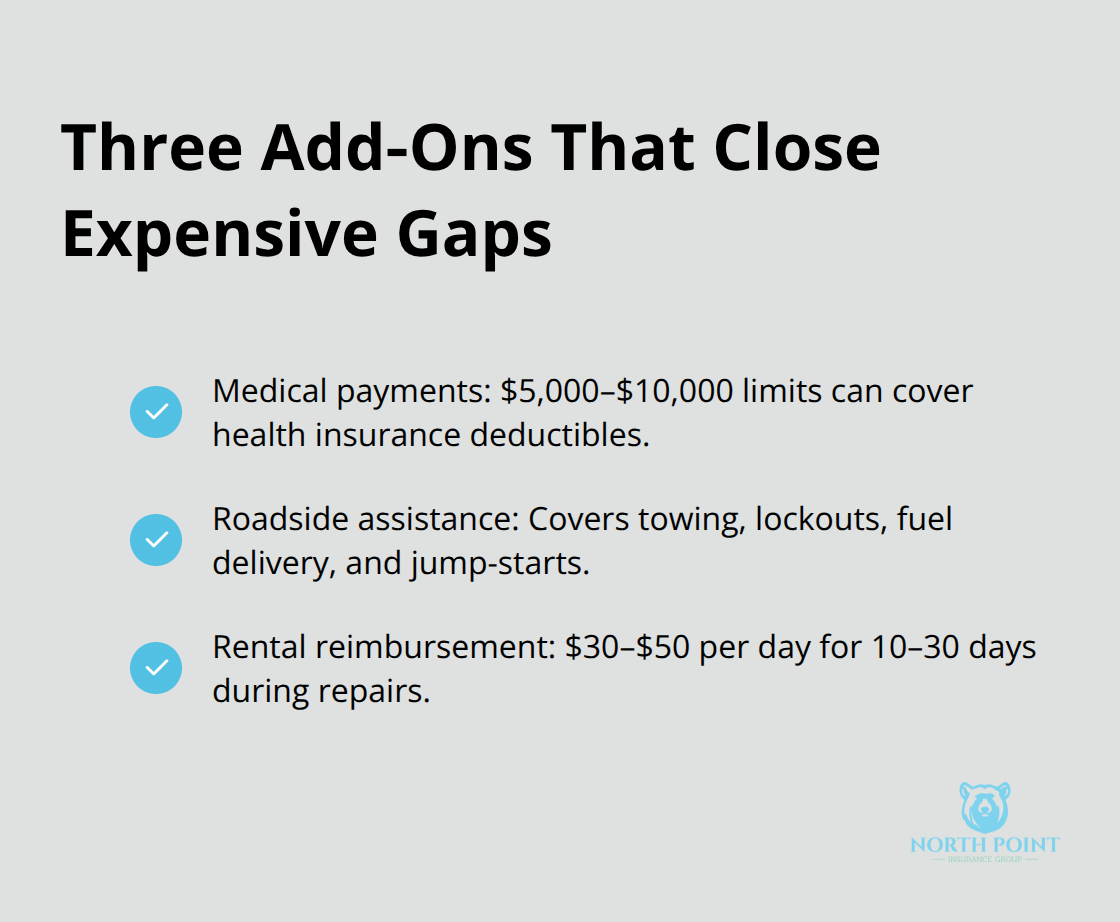

Most drivers focus on liability, collision, and comprehensive coverage because those are the categories their insurer emphasizes. What gets overlooked are the smaller coverages that fill critical gaps when accidents or unexpected situations happen. Medical payments coverage, roadside assistance, and rental car reimbursement sound optional, but they address real costs that standard coverage leaves uncovered. Clients often file claims only to discover they’re personally responsible for expenses they assumed were covered.

Medical Payments Coverage Closes Health Insurance Gaps

Medical payments coverage pays for medical and funeral expenses for you and your passengers regardless of fault, which matters because your health insurance often won’t cover accident-related injuries or may impose deductibles that leave you exposed. If you’re in a collision caused by another driver and your health insurance has a $1,500 deductible, medical payments coverage of $5,000 or $10,000 covers that gap immediately. The cost is typically $15 to $25 per month for solid coverage, making it one of the cheapest protections you can add.

Roadside Assistance Protects Against Unexpected Breakdowns

Roadside assistance and towing coverage becomes essential if you drive an older vehicle or frequently travel long distances. A single towing bill can run $500 to $1,500 depending on distance, and roadside assistance covers not just towing but lockouts, fuel delivery, and jump-starts. Many drivers rely on memberships like AAA, but bundling roadside assistance with your auto policy costs less and coordinates directly with your claim process.

Rental Car Reimbursement Keeps You Mobile

Rental car reimbursement covers the daily cost of a rental vehicle while yours is being repaired after a covered loss, typically at $30 to $50 per day with a maximum duration of 10 to 30 days. Without this coverage, you’re either paying out of pocket for transportation or stuck without a vehicle while repairs take weeks. The annual cost of rental car reimbursement is usually $50 to $100, but a single claim without this coverage can cost you $1,000 or more if repairs take longer than expected.

Audit Your Current Policy for These Gaps

When you review your current policy, check whether these three coverages exist and at what limits. If they’re missing entirely, adding them costs roughly $40 to $60 monthly and eliminates thousands in potential out-of-pocket expenses. Each coverage addresses a specific vulnerability that liability, collision, and comprehensive leave unprotected.

Final Thoughts

Understanding auto coverage basics means recognizing that your policy is only as strong as the decisions you make about it. The coverages you’ve read about-liability, collision, comprehensive, uninsured motorist protection, and the smaller add-ons like medical payments and rental reimbursement-work together to protect your finances and your family. You need to verify they’re actually in your policy at appropriate limits, and you need to understand the trade-offs you’re making with deductibles and premium costs.

The gap between what drivers think they’re covered for and what they actually are covered for costs people thousands every year. Some discover too late that their liability limits won’t cover a serious accident, while others file claims only to realize they’re paying out of pocket for medical expenses or rental cars because they skipped optional coverages to save $30 a month. These aren’t theoretical problems-they happen regularly, and they’re preventable.

Pull out your current policy declarations page and compare it against what you’ve learned here. Check your liability limits, verify your deductible amounts, and confirm whether you have medical payments coverage, uninsured motorist protection, and rental car reimbursement. An independent agent at North Point Insurance Group shops multiple carriers to find coverage that matches your actual needs and budget, not just the cheapest option available, and they explain the trade-offs so your policy reflects your real situation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.