Home Insurance Deductible Guide: How Much Can You Pay

Your home insurance deductible is one of the most misunderstood parts of your policy. Many homeowners pick a number without understanding how it affects their monthly premiums or what happens when they file a claim.

At North Point Insurance Group, we’ve helped thousands of homeowners find the right deductible for their situation. This guide walks you through the numbers, the trade-offs, and the practical decisions that matter.

What Your Home Insurance Deductible Actually Costs You

How Your Deductible Works in a Claim

Your home insurance deductible is the amount you pay out of pocket when you file a claim. If a pipe bursts and causes $8,000 in damage, and your deductible is $1,000, you write a check for $1,000 and the insurance company covers the remaining $7,000. That deductible applies per claim, which means if you have two separate losses in one year, you pay the deductible twice. The deductible only applies to covered losses, so if damage falls outside your policy’s coverage or the repair cost is less than your deductible, you receive no payout at all. This is why a $300 water leak with a $500 deductible means you pay the full $300 yourself-filing a claim would be pointless.

The Premium Savings You Get from Higher Deductibles

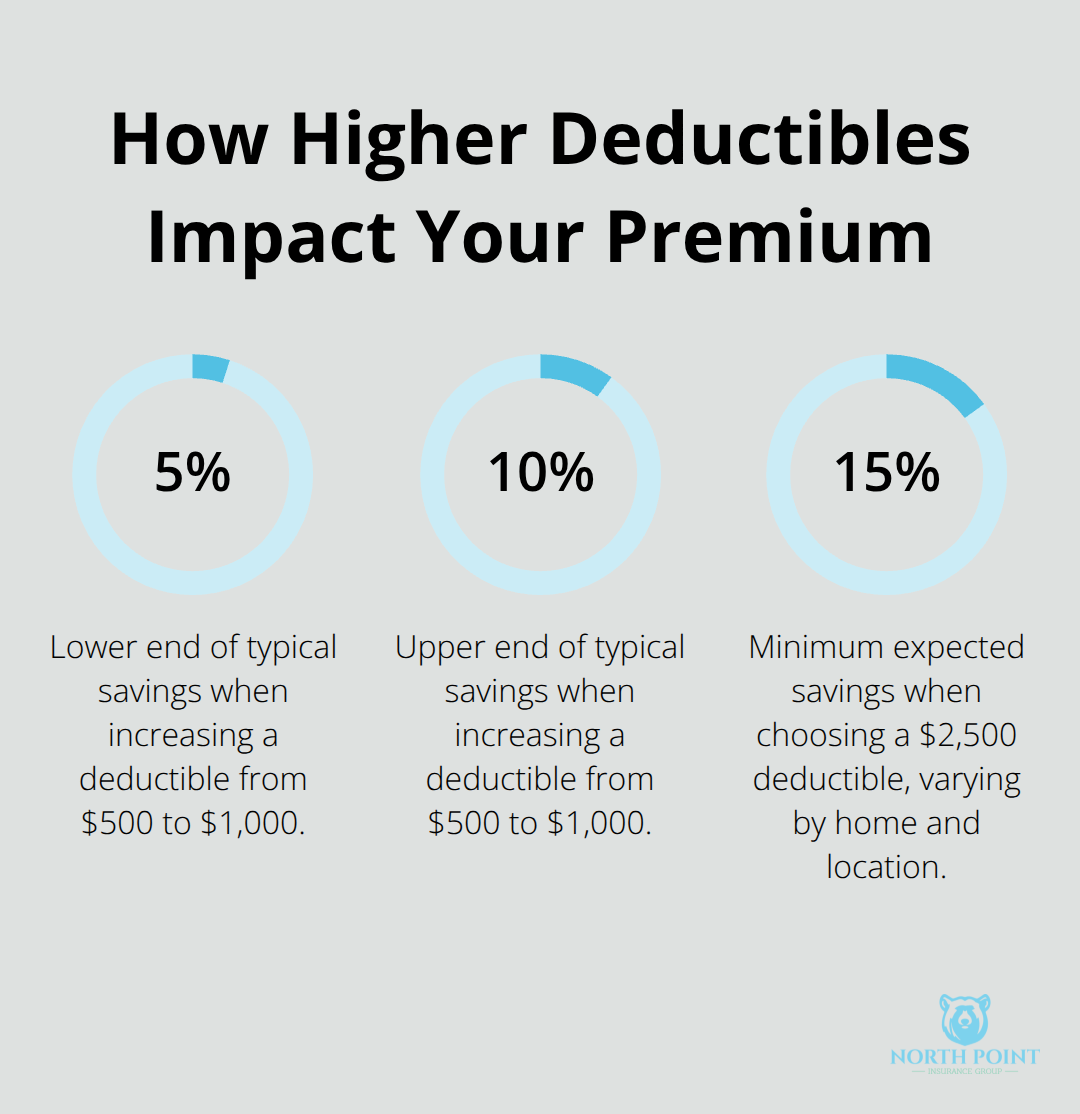

Higher deductibles directly lower your annual premium. Raising your deductible from $500 to $1,000 typically cuts your premium by 5% to 10%, according to real-world comparisons. Move to a $2,500 deductible and you could see savings of 15% or more depending on your location and home value. A homeowner shopping for coverage in Northern California received a quote of $1,200 per year with a $5,000 deductible from one carrier and $1,560 per year with a $1,000 deductible from another.

The trade-off is real: you save monthly but expose yourself to larger out-of-pocket costs when damage happens. This inverse relationship means your job is figuring out where the sweet spot sits for your finances, not picking the lowest premium or the lowest deductible.

Flat Deductibles and Percentage-Based Deductibles

Most homeowners encounter a flat deductible, typically ranging from $500 to $2,500. You pick a number, and that’s what you pay on any covered claim. However, weather-related damage-wind, hail, hurricanes-often triggers a separate percentage-based deductible instead. If your home’s replacement cost is $300,000 and you have a 1% hurricane deductible, you’d pay $3,000 out of pocket for storm damage rather than your standard $1,000 flat deductible. Earthquake and flood deductibles work the same way. These percentage deductibles can range from 1% to 10% of your home’s insured value depending on your location and risk level.

Coverages That Carry No Deductible

Some coverages carry no deductible at all-liability protection, medical payments coverage, and additional living expenses typically have zero deductibles across most policies. Before you settle on a deductible strategy, check whether your policy includes these hidden disaster deductibles, because they dramatically change your total out-of-pocket exposure during the events that matter most. Understanding what you actually owe in different scenarios sets the stage for the next critical decision: which factors should influence your deductible choice.

What Really Determines Your Deductible

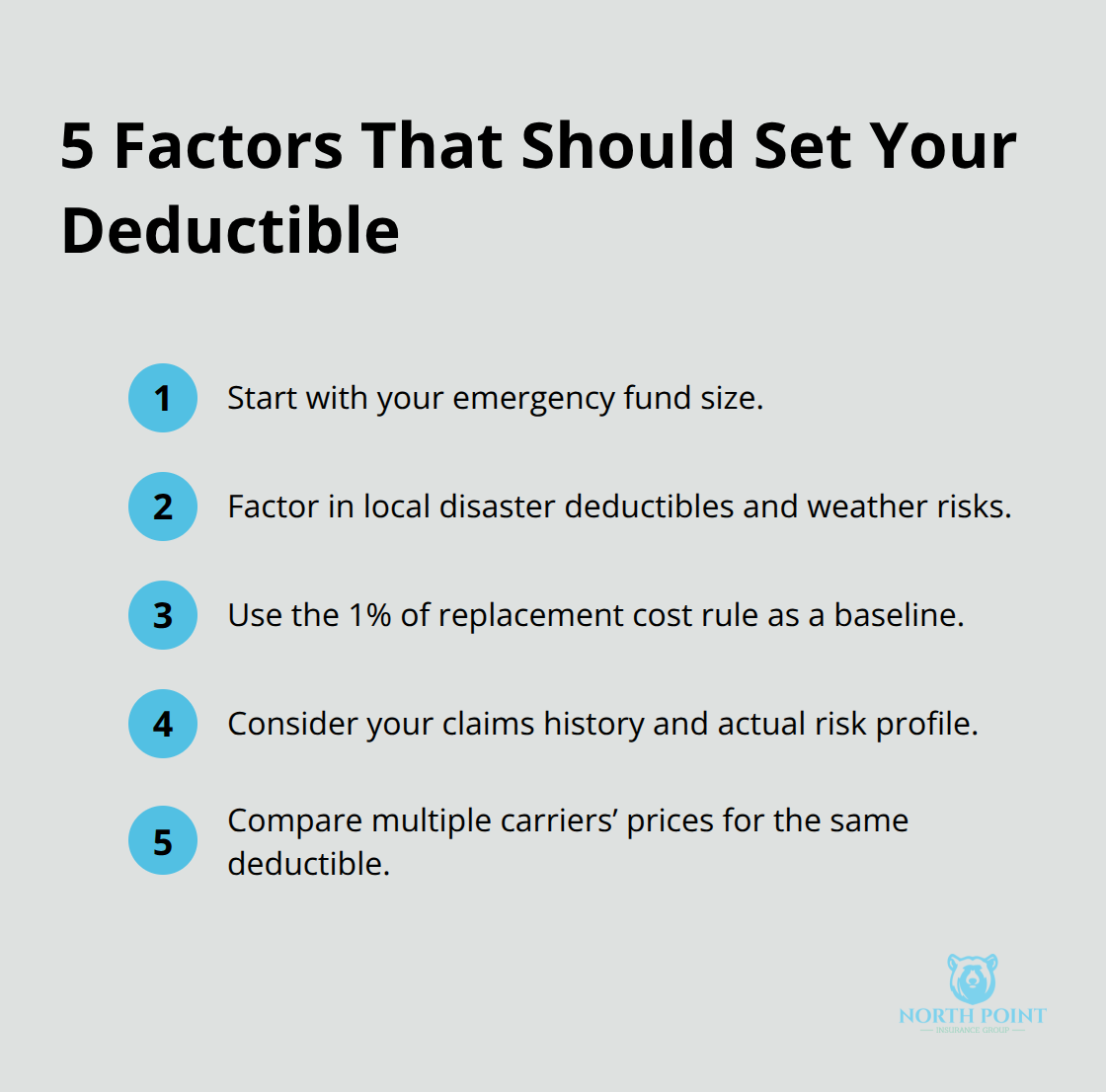

Your emergency fund size should be the first number you examine when choosing a deductible. If you have $3,000 in savings, a $2,500 deductible is realistic; a $5,000 deductible leaves you vulnerable. The rule is straightforward: your deductible should never exceed what you could replenish within a few months after paying it. If an unexpected $8,000 pipe burst happens and you drain your entire emergency fund to cover a $5,000 deductible, you’ve eliminated your financial cushion exactly when you need it most. Most people underestimate how long it takes to rebuild savings after a major claim, so set your deductible conservatively relative to what you actually have available.

Where You Live Changes Everything

Location matters more than most homeowners realize. If you live in an area prone to hurricanes, hail, or wildfires, the percentage-based deductibles on those specific perils can dwarf your standard flat deductible. A homeowner in coastal Florida might face a 5% hurricane deductible on a $400,000 home, meaning $20,000 out of pocket for storm damage. In that scenario, a low flat deductible of $500 provides almost no real protection because the hurricane deductible supersedes it. Conversely, if you live in a low-risk weather area with minimal earthquake or flood exposure, a $1,500 or higher flat deductible paired with a lower premium makes financial sense.

The 1% Rule as Your Starting Point

The 1% rule-setting your deductible at roughly 1% of your home’s replacement cost-works well as a starting point. For a $300,000 home, that’s a $3,000 deductible, which typically balances premium savings against major-loss protection. However, this rule breaks down in high-risk zones where disaster deductibles already force you into larger out-of-pocket amounts. Test this approach by comparing quotes at the 1% level against higher and lower deductibles to see which premium difference justifies the extra out-of-pocket exposure.

Claims History and Your Actual Risk Profile

Your claims history directly affects your deductible strategy. If you’ve filed three water-damage claims in five years, filing small claims repeatedly costs more in lost discounts and premium increases than it saves. In that case, a higher deductible discourages unnecessary claims and keeps your premium stable. Conversely, if you’ve never filed a claim and your home sits in a stable neighborhood with no major weather threats, a high deductible cuts your annual cost significantly without meaningful risk.

How Carriers Set Their Own Deductible Rules

Different insurance companies set minimum deductibles based on your zip code and home characteristics. Some carriers won’t quote below $1,000 in certain areas, while others offer $250 or $500 minimums. When you shop around-and you should always get multiple quotes-you’ll see that the same deductible produces different premiums across carriers. A $1,000 deductible might cost $1,200 annually with one company and $1,500 with another. That $300 difference matters more than minor deductible tweaks, which is why comparing options across multiple insurers reveals the real value of your deductible choice rather than settling on a number in isolation.

Picking Your Deductible Without Guessing

Start with What You Can Actually Afford

The moment you start comparing quotes, you’ll see that deductible choice splits into two competing pressures: lower your monthly payment or lower your out-of-pocket risk. Most homeowners chase the lowest premium and pick a $5,000 deductible without asking whether they could actually write that check after a loss. That’s backward. Start instead with your bank account. If you have $8,000 in liquid savings, a $2,500 deductible works. If you have $3,000, stop at $1,500. The math is simple: your deductible should be something you could replenish within three months of paying it without destroying your financial stability. A $5,000 deductible that saves you $200 annually means nothing if one claim wipes out your emergency fund and leaves you vulnerable for months.

Test the Real Dollar Difference

Run quotes at three different deductible points-say $750, $1,500, and $2,500-and look at the actual annual premium difference. If moving from $1,500 to $2,500 saves only $80 per year, that extra $1,000 of exposure isn’t worth the savings. If it saves $300, the math shifts in favor of the higher deductible. The key is seeing the trade-off in concrete numbers, not picking a deductible in a vacuum. Different carriers price the same deductible change differently, so comparing options across multiple insurers reveals which choice delivers real value.

Verify Your Coverage Limits Match Your Home’s Cost

Coverage limits deserve equal attention because they work differently than deductibles. Your deductible is what you pay; your coverage limit is the maximum your insurer pays. A $300,000 dwelling coverage limit means the insurance company won’t pay more than $300,000 to rebuild your home, regardless of actual costs. Many homeowners set deductibles based on premium alone without checking whether their coverage limits match their home’s replacement cost. In high-inflation markets like coastal areas, a home valued at $500,000 might cost $650,000 to rebuild today. A $400,000 dwelling limit leaves a $250,000 gap that you’d cover yourself. In this scenario, obsessing over a $500 versus $1,000 deductible choice is pointless-you’re already massively underinsured. Request a replacement cost estimate from your carrier and compare it to what you’d actually spend to rebuild. If there’s a gap, raising coverage limits matters far more than tweaking deductibles.

Adjust Your Deductible as Your Life Changes

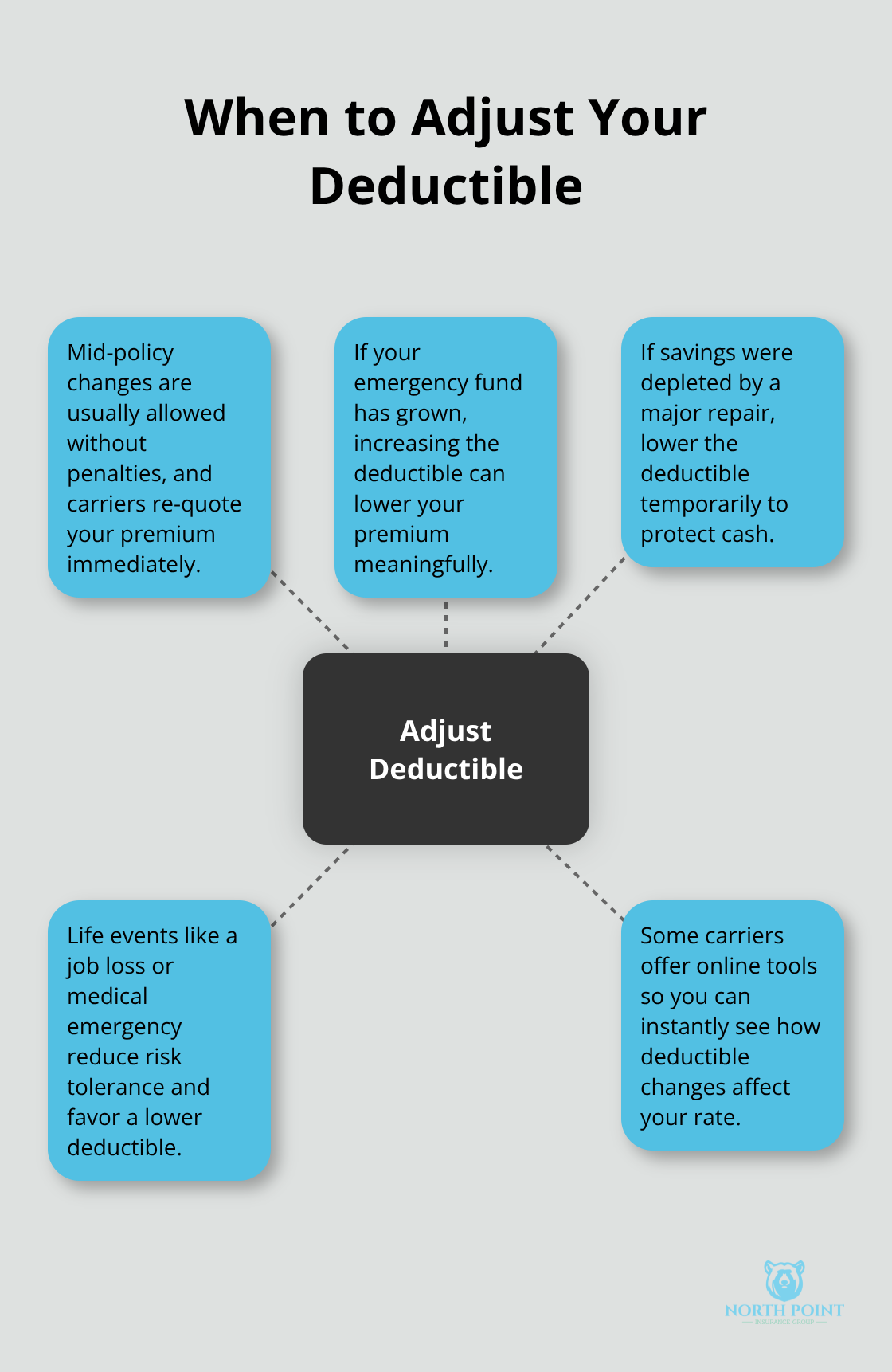

Most carriers allow deductible changes mid-policy without penalties and will re-quote your premium immediately. This flexibility means you can test your assumptions. If you picked a $1,500 deductible based on guesswork and your emergency fund has grown to $6,000, shifting to $2,500 and pocketing the premium savings makes sense. Conversely, if a major repair depleted your savings, lowering your deductible from $2,000 to $750 protects you until you rebuild reserves, even if premiums rise temporarily. The trap most homeowners fall into is never revisiting their choice. You pick a deductible when you buy your policy and leave it for five years while your financial situation changes completely. Life events matter here: a job loss, a medical emergency, or a major home repair that drains savings all shift your actual risk tolerance.

Some carriers offer online quote tools that let you instantly see how deductible changes affect your rate, so you can make informed decisions without calling an agent.

Shop Around When You Adjust

Shop around when you adjust your deductible because different carriers price the same change differently. A $1,000 to $1,500 shift might cost you $50 more annually with one company and save $30 with another. The carrier that underpriced your original quote might overprice the adjustment, making it worth switching entirely. A deductible that looks good on paper can create genuine hardship when a claim arrives and you’re scrambling to cover it. Pick a number you can actually afford to pay, verify your coverage limits match your home’s true replacement cost, and revisit both annually as your finances and local construction costs shift.

Final Thoughts

Your home insurance deductible choice comes down to one principle: pick a number you can actually afford to pay when damage happens. The lowest premium doesn’t deliver real value if it forces you into a deductible that would drain your emergency fund, so test the actual dollar difference between options before you commit. A $500 annual savings means nothing if it comes with a $5,000 deductible you cannot cover.

Your deductible isn’t permanent, and most carriers allow mid-policy changes without penalties. A job loss, inheritance, major home repair, or growing emergency fund all shift what deductible makes sense for you, so revisit your choice whenever your financial situation changes. Rising construction costs in your area may also require coverage limit adjustments even if your deductible stays the same.

The final step is getting quotes from multiple carriers at your target deductible, since different insurers price the same deductible differently. We at North Point Insurance Group work with 20+ carriers to find coverage that matches both your budget and your actual risk. Contact us when you’re ready to test your assumptions against real quotes and discover which option delivers genuine value for your situation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.