Auto Insurance Shopping Georgia: Get the Best Deals

Auto insurance shopping in Georgia doesn’t have to be overwhelming. We at North Point Insurance Group know that finding affordable coverage means understanding your options and comparing what’s actually available to you.

This guide walks you through the process step by step, from gathering the right information to identifying the discounts that lower your premiums.

How to Compare Auto Insurance Quotes in Georgia

Understand What Coverage Types You Need

Getting quotes from multiple insurers is the only way to see what Georgia auto insurance actually costs for your specific situation. Experian’s March 2026 data shows Georgia drivers pay an average of $3,198 annually, but that number masks huge variation-someone in Augusta might pay $2,360 while an Atlanta driver pays $3,112 for the same coverage. The difference comes down to what each insurer charges for your exact profile, and since carrier pricing formulas are proprietary, you cannot predict what one company will quote without asking.

Start by deciding whether you need minimum coverage or full coverage. Georgia’s legal minimum is $25,000 bodily injury per person, $50,000 per accident, and $25,000 property damage, but Nationwide reports average bodily injury claims hit $26,501-meaning minimum coverage leaves you exposed. Full coverage adds collision and comprehensive protection, averaging $3,694 annually versus $2,324 for minimum coverage.

Prepare Your Information for Quotes

Once you know what type of coverage makes sense for your vehicle and risk tolerance, you must gather specific details before requesting quotes. Have ready your vehicle’s year, make, model and VIN; your annual mileage; your driver’s license number; how many drivers live in your household; any accidents or violations in the past three years; and your desired deductible amounts. Providing identical information to each insurer ensures apples-to-apples comparisons instead of wildly different quotes based on different assumptions.

Request Quotes from Multiple Carriers

Request quotes from at least three to five carriers because pricing varies dramatically. According to Experian data, the cheapest full-coverage carriers in Georgia are Travelers at $2,236 annually, Mercury at $2,918, and Root at $2,965-but these same carriers may price significantly higher for your specific profile depending on your age, driving record, location and credit history. If you have a clean driving record, you can expect rates around $2,954 annually for full coverage, but one accident jumps that to $3,383, and three or more violations push it to $3,821.

Credit history matters too: drivers with good credit average $106 monthly with the cheapest options, while those with poor credit pay $176 monthly even with the most affordable carriers. Don’t skip regional insurers like Georgia Farm Bureau or Central Insurance-they often offer lower rates than national carriers plus extra perks unavailable elsewhere.

Compare More Than Just Price

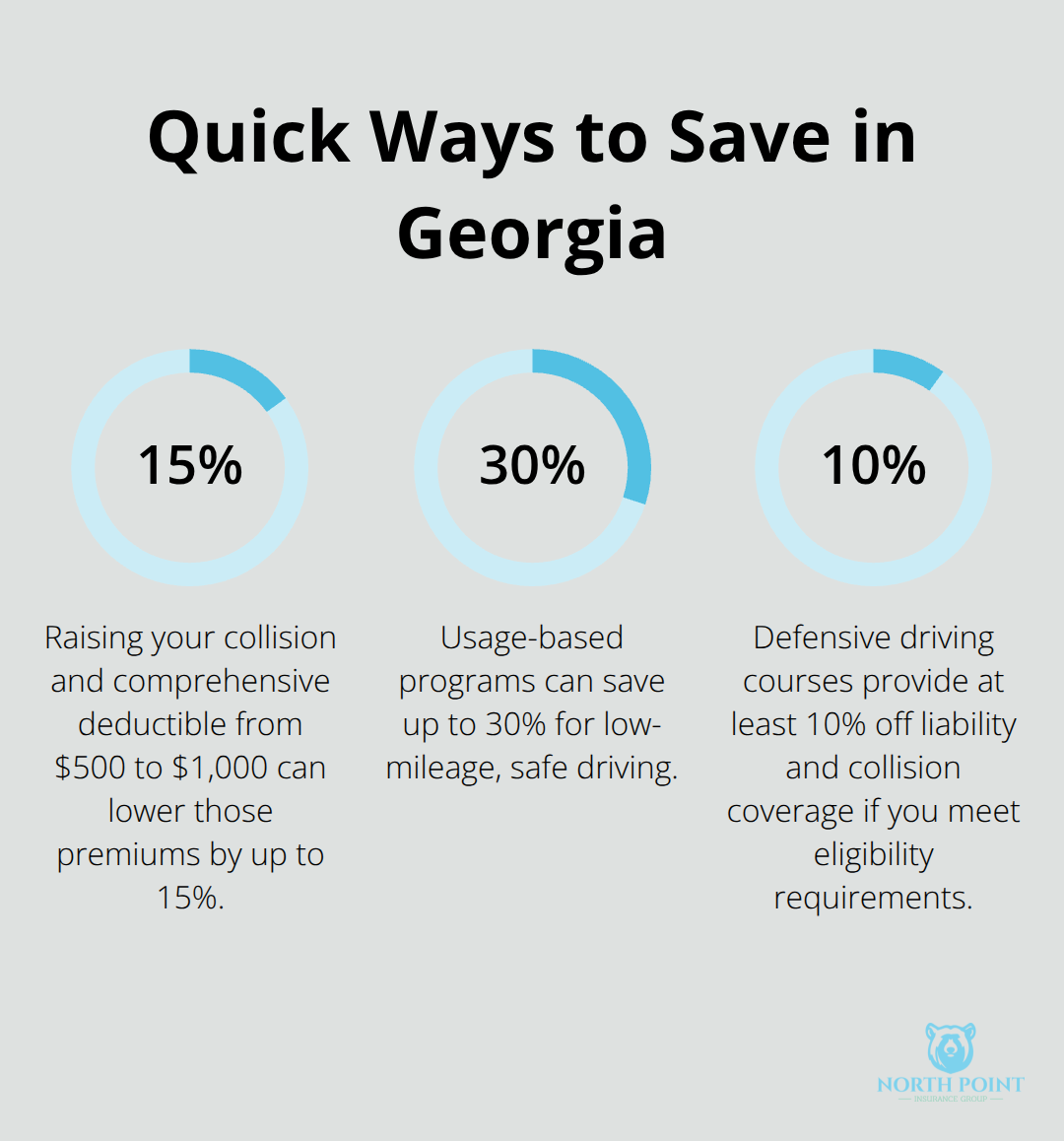

Once you have quotes in hand, you must compare not just price but also deductible options, coverage limits, and available discounts. Raising your deductible from $500 to $1,000 typically lowers collision and comprehensive premiums by 10–15%, a meaningful reduction if you can afford the higher out-of-pocket cost. Set a yearly reminder to shop again before your renewal date, since rates fluctuate based on weather events, population growth, and repair costs in your area.

With your quotes compared and your best options identified, the next step involves understanding what actually drives your rates up or down-and how your personal profile shapes the premiums you’ll pay.

Factors That Affect Your Auto Insurance Rates in Georgia

Your Driving Record and Claims History

Your driving record is the single biggest factor insurers use to price your policy, and the numbers prove why they care so much. According to Experian data, a clean driving record gets you rates around $2,954 annually for full coverage, but one accident jumps that to $3,383. Three or more violations push you to $3,821 annually-a $867 difference between clean and problematic records that stays in your pocket if you avoid violations and at-fault claims.

Even a speeding ticket alone raises premiums significantly, so defensive driving matters financially. Georgia allows defensive driving course discounts of at least 10% on liability and collision coverage if you meet the requirements. For drivers 25 and older, this means no moving violations and no at-fault claims in the past three years plus completion of six hours of instruction. The course pays for itself quickly if you qualify.

Insurers also examine whether you filed claims previously. A history of claims signals higher future risk, so avoiding collisions and comprehensive claims keeps your rates competitive.

Vehicle Type and Safety Features

Your vehicle’s make, model, year and built-in safety features directly influence what you pay monthly. A car equipped with anti-theft devices and modern safety features costs less to insure than an older vehicle without them because theft and accident costs are lower. Insurers factor in the vehicle’s repair costs and safety ratings when they calculate your premium, which explains why two drivers insuring different cars receive different quotes from the same company.

Age, Gender, Credit History, and Location

Age and gender matter significantly-young drivers around age 20 face $205 monthly for full coverage even with the cheapest carriers, while Gen X drivers pay around $104 monthly and senior drivers around $123 monthly. These differences reflect actuarial data on crash frequency by age group.

Credit history in Georgia affects premiums substantially. Drivers with good credit pay $106 monthly with affordable carriers while those with poor credit pay $176 monthly with the best options available to them. Marital status also plays a role since insurers view married drivers as slightly lower risk, though the effect is smaller than driving record or credit history.

Location within Georgia matters enormously. Augusta averages $2,360 annually while Atlanta averages $3,112 for identical coverage because urban areas have higher accident rates, theft risk and repair costs. These factors combine to create your individual rate, which is why two drivers in the same household can receive vastly different quotes from the same insurer.

Understanding how insurers calculate your premium sets the stage for the next critical step: identifying which discounts and strategies actually reduce what you owe each month.

How to Actually Lower Your Georgia Auto Insurance Premiums

Knowing what drives your rates up is only half the battle-the other half involves taking concrete action to reduce what you actually pay each month. Small changes in how you structure your coverage or which discounts you claim can save hundreds annually. The strategies that work best aren’t theoretical; they’re grounded in real numbers and real savings available to you right now.

Bundle Your Auto Policy with Other Coverage

Bundle home and auto insurance in Georgia and receive up to 13.9% on your insurance. This single move often produces the largest savings for most households. If you add an umbrella policy to your bundle, you may increase your discounts further. The process takes minimal effort-most insurers calculate bundled rates within minutes once you request a quote.

Raise Your Deductible to Match Your Budget

Raising your collision and comprehensive deductible from $500 to $1,000 typically lowers those specific premiums by 10 to 15 percent. This strategy works only if you can afford the higher out-of-pocket cost when you file a claim. Calculate whether the annual savings justify the increased deductible before you commit to this change.

Leverage Usage-Based Insurance and Safety Features

If you drive fewer than 10,000 miles annually, usage-based insurance programs track your mileage and safe driving habits, potentially saving you 10 to 30 percent. Anti-theft devices and modern safety systems reduce your comprehensive and collision costs because insurers know these features lower claim frequency and severity. Adding these protections to your vehicle pays dividends through lower premiums.

Improve Your Credit and Take Defensive Driving Courses

Credit history influences premiums substantially in Georgia, with drivers maintaining good credit paying roughly $70 monthly less than those with poor credit. Reviewing your credit report and disputing errors costs nothing but can reduce your rates significantly. Georgia’s defensive driving course discount provides at least 10 percent off liability and collision coverage, and the six-hour course costs far less than what you’ll recover in premium savings within a single year.

Shop Annually and Compare Across Carriers

The most powerful strategy remains comparison shopping before each renewal-rates fluctuate based on weather patterns, population growth in your area, and repair costs, meaning a carrier that quoted you $1,500 last year might quote $1,800 this year while a competitor quotes $1,400 for identical coverage. Setting a calendar reminder to shop annually takes 30 minutes but captures savings that compound year after year. Comparing quotes from regional carriers like Georgia Farm Bureau or Central Insurance alongside national companies matters because regional insurers often price differently and offer perks unavailable elsewhere. Don’t assume the cheapest quote is your best option-verify that coverage limits match across quotes, that deductibles are identical, and that available discounts align with your household situation before you decide.

Final Thoughts

Auto insurance shopping in Georgia requires you to request quotes from multiple carriers because rates fluctuate based on weather, population changes, and repair costs in your area. A carrier quoting you $1,500 this year might quote $1,800 next year while a competitor offers $1,400 for identical coverage. Your driving record, credit history, vehicle type, and location shape your rates, but bundling policies, raising deductibles strategically, and completing defensive driving courses all reduce what you actually pay each month.

Start by gathering your vehicle details, driving history, and desired coverage limits, then request quotes from at least three to five carriers, including regional insurers like Georgia Farm Bureau alongside national companies. Compare not just price but deductible options, coverage limits, and available discounts to verify that each quote includes identical information. The difference between a driver who shops around and one who doesn’t often exceeds $500 annually, money that stays in your pocket when you take these steps seriously.

North Point Insurance Group can simplify your auto insurance shopping Georgia process by connecting you with competitive pricing and tailored coverage that matches your actual needs. As an independent agency based in Alpharetta, they shop multiple carriers to find options that fit your household and explain which discounts apply to your situation. Contact them to secure the right policy at the right price.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.