Auto Insurance Options Georgia: Find the Right Coverage

Georgia requires all drivers to carry auto insurance, but choosing the right auto insurance options in Georgia can feel overwhelming. We at North Point Insurance Group know that understanding your coverage choices matters-it protects your finances and keeps you legal on the road.

This guide walks you through Georgia’s insurance requirements, the types of coverage available, and what factors affect your rates. By the end, you’ll know exactly what coverage you need.

Understanding Georgia’s Auto Insurance Requirements

State Minimum Coverage Limits and Liability Laws

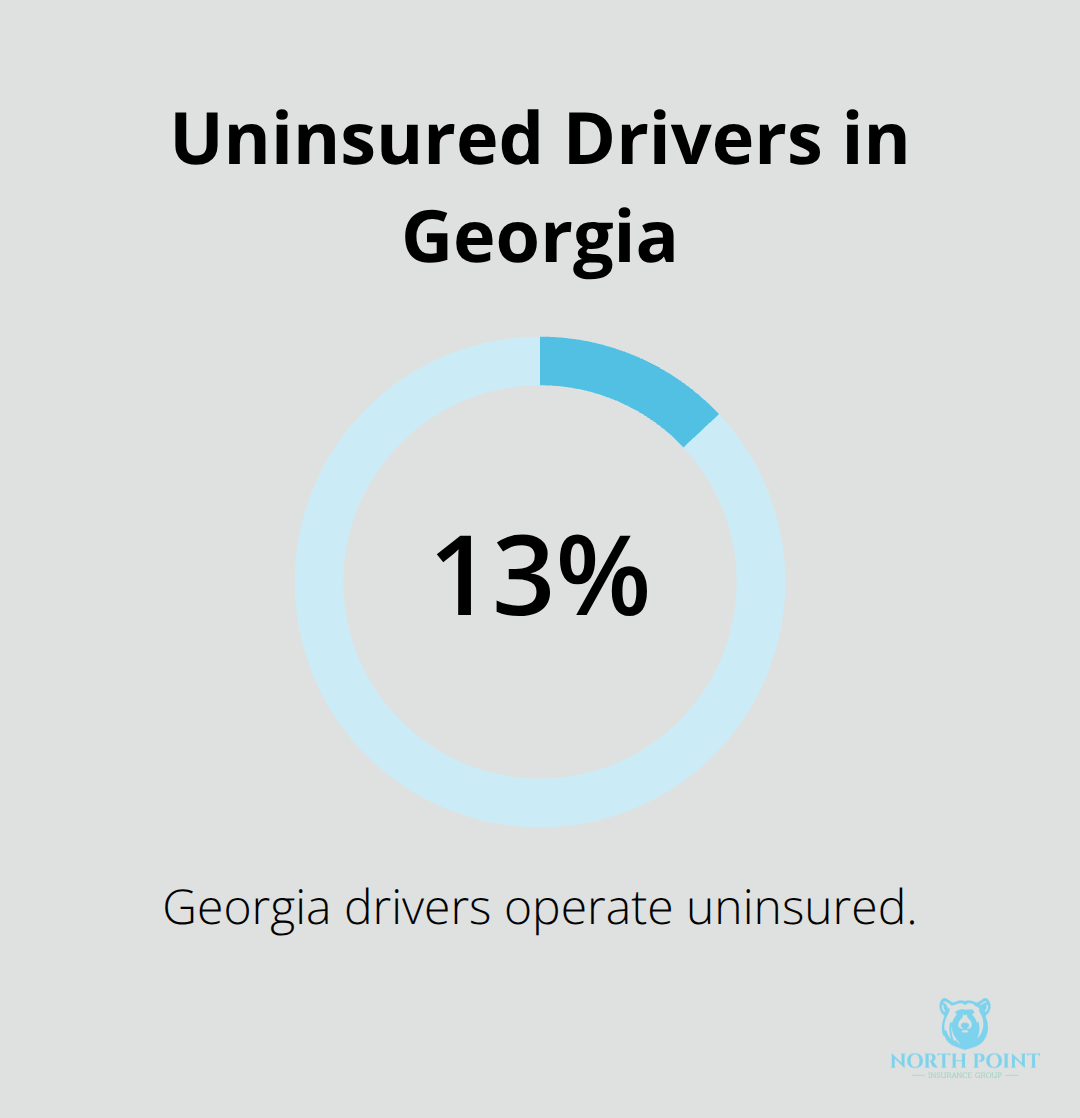

Georgia requires all drivers to carry auto insurance with specific minimum limits. The state mandates $25,000 per person and $50,000 per accident for bodily injury liability, plus $25,000 for property damage liability-the 25/50/25 formula that serves as your legal floor. You also must carry uninsured motorist coverage, though Georgia allows you to reject it in writing (a risky choice given how many uninsured drivers operate on Georgia roads). The state’s verification system tracks your coverage electronically: when you purchase a policy, your insurer reports it directly to Georgia’s database, so you cannot slip through unnoticed.

Penalties for Driving Uninsured in Georgia

Driving without insurance carries serious consequences in Georgia. The state suspends your license immediately upon conviction, assesses a $200 minimum fine plus court costs, and can impose up to 12 months in jail for repeat violations. If you cause an accident while uninsured, you become personally liable for all damages-medical bills, vehicle repairs, lost wages, and more. A single crash could cost tens of thousands of dollars out of your pocket, far exceeding what insurance would have cost annually.

How Georgia’s Insurance Verification System Works

Georgia’s electronic monitoring system tracks all active policies in real time. When you purchase coverage, your insurer reports it to the state’s database within days. This automated system flags uninsured vehicles during traffic stops or accident investigations. The Georgia Department of Insurance Consumer Services Division handles complaints about coverage issues and can be reached at 404-656-2070 or 800-656-2298 (Monday–Friday, 8 a.m. to 5 p.m. ET).

Shopping for Coverage and Verifying Insurers

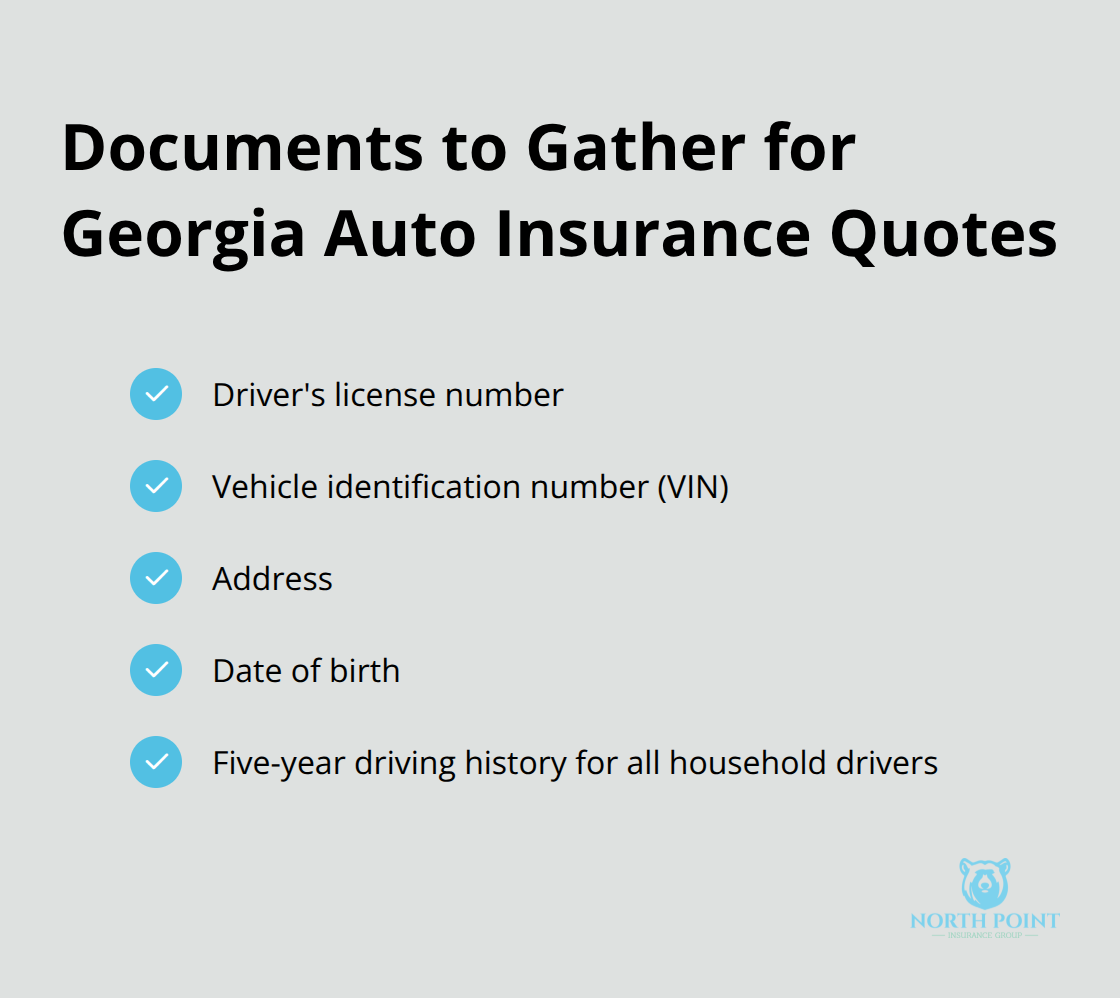

Georgia’s average car insurance cost is $3,281 annually or $273 per month according to Experian data from February 2026. That premium makes shopping essential-comparing quotes from multiple carriers using identical coverage levels can save you hundreds annually. When you request quotes, prepare your driver’s license number, vehicle identification number, address, date of birth, and your five-year driving history for all household drivers. Before you buy, verify the insurer and agent are licensed through Georgia.gov’s License Lookup tool, because purchasing from an unlicensed company is illegal and voids your coverage.

Discounts and Policy Review

Read your policy carefully after purchase since it’s a legal contract outlining exactly what’s covered and what isn’t. Many carriers offer bundle discounts that reduce premiums significantly-combining auto with home or renters insurance, for example, or qualifying for good-student or safe-driver discounts. The state publishes premium comparison data to help you make informed decisions, and independent ratings from J.D. Power and AM Best indicate which carriers deliver reliable claims handling alongside competitive pricing. Understanding these coverage options and rate factors positions you to select the right protection for your situation.

Types of Auto Insurance Coverage Available

Liability Coverage: Your Legal Foundation and Financial Shield

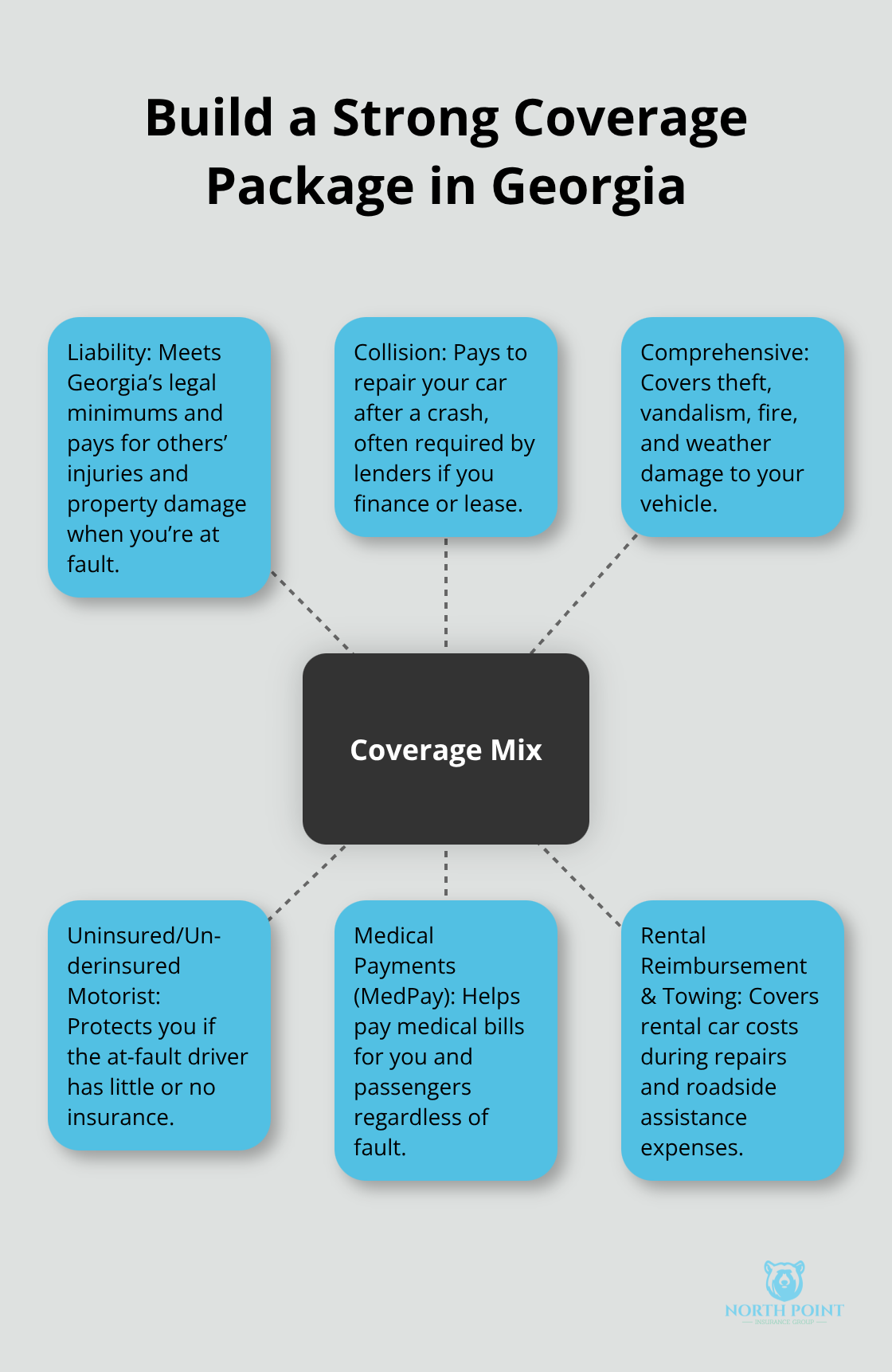

Liability coverage is where Georgia’s legal requirements start, but it’s also where most drivers stop thinking-and that’s a mistake. The state mandates bodily injury liability of $25,000 per person and $50,000 per accident, plus $25,000 for property damage, but these limits barely cover a serious accident. If you cause a crash that injures multiple people or damages an expensive vehicle, the 25/50/25 minimum leaves you personally responsible for thousands in medical bills, lost wages, and repair costs that exceed your coverage.

Try carrying at least $100,000 per person and $300,000 per accident in bodily injury coverage, plus $100,000 in property damage-roughly double the state minimum. This higher coverage costs only marginally more monthly but protects your wages, home, and future earnings if a lawsuit follows an accident you cause.

Collision and Comprehensive: Protecting Your Vehicle

Collision and comprehensive coverage protect your own vehicle rather than others’ property. Collision covers damage from crashes, while comprehensive handles theft, vandalism, fire, and weather-neither is legally required in Georgia unless your lender or leasing company mandates it. If you financed or leased your vehicle, expect the lender to require collision coverage with a specific deductible, often $500 or $1,000.

The choice between these deductibles matters financially: a $1,000 deductible lowers your monthly premium by roughly 15–25% compared to $500, but you’ll pay more out of pocket if you file a claim. Drivers with clean records and vehicles worth under $10,000 might skip collision and comprehensive, accepting the risk of total loss rather than paying premiums on a depreciating asset. Conversely, drivers with accidents or violations on their record, or those financing newer vehicles, should carry full coverage to avoid financial catastrophe.

Uninsured and Underinsured Motorist Protection

Uninsured and underinsured motorist coverage protects you when another driver causes an accident but carries insufficient or no insurance-Georgia requires it, though you can reject it in writing. The reality is brutal: roughly 13% of Georgia drivers operate uninsured, meaning one in eight vehicles on the road could leave you uncompensated for injuries and vehicle damage.

Georgia allows you to carry uninsured motorist coverage at or above your bodily injury limits; matching your UM limits to your BI limits protects you against the same injury costs regardless of who caused the accident.

Optional Coverages That Fill Critical Gaps

Medical payments coverage (MedPay) and rental reimbursement are optional but practical additions. MedPay covers medical expenses for you and passengers after any accident, regardless of fault, and typically costs $5–15 monthly for $5,000 in coverage. Rental reimbursement reimburses daily rental car costs while your vehicle is repaired, usually capping at $30 per day for up to 30 days, and costs roughly $10 monthly.

These coverages sound minor until you’re injured in an accident not your fault and face $10,000 in medical bills while waiting for the other driver’s insurer to process your claim, or you’re without transportation for two weeks while repairs take place. Towing and labor coverage covers roadside assistance-towing, lockouts, jump-starts, and fuel delivery-and typically runs $5–10 monthly for $100 in coverage. If you drive an older vehicle prone to breakdowns or live far from service stations, this coverage prevents a $200 tow bill from derailing your budget.

Matching Coverage to Your Situation

Your driving record and vehicle value should guide your coverage decisions. The Georgia Department of Insurance publishes premium comparison data, and independent ratings from J.D. Power and AM Best help you identify carriers offering reliable claims handling alongside competitive pricing for the coverages you choose. Once you understand what each coverage protects, the next step involves identifying which rate factors most heavily influence your premiums-and how to control them.

Factors That Affect Your Auto Insurance Rates in Georgia

How Your Driving Record Impacts Premiums

Your driving record is the single biggest lever you control, and it’s worth understanding exactly how much damage one accident or violation causes. A single at-fault accident increases your premium by 25–40% for three to five years, while a speeding ticket typically adds 10–15% annually. Multiple violations compound aggressively: two accidents within three years push your rate up 50–75% compared to a clean record. Independent data shows that drivers with clean records pay roughly $200–250 monthly for full coverage in Georgia, while those with one accident pay $280–320. This gap widens further with multiple incidents.

Maintaining a clean driving record saves you thousands over a decade. If you’ve already accumulated violations, some carriers offer accident forgiveness programs that prevent your first accident from raising your rate, though these programs vary by carrier and come with eligibility restrictions. Progressive, for instance, offers three different accident forgiveness options, giving you flexibility in how you structure your policy.

Vehicle Type, Age, and Safety Features

Vehicle choice affects your premium substantially because insurers price based on claim history for each make and model. A 2023 Honda Civic costs significantly less to insure than a 2023 Dodge Charger because the Civic generates fewer collision and theft claims historically. Safety features like automatic emergency braking, adaptive headlights, and anti-theft systems lower premiums by 5–15% because they reduce accident frequency and theft risk. Conversely, high-performance vehicles, luxury cars, and models with expensive repair costs command higher premiums regardless of your driving record.

Location, Credit Score, and Coverage Limits

Location within Georgia matters more than many drivers realize: urban ZIP codes like Atlanta’s core generate 20–40% higher premiums than suburban or rural areas due to higher accident frequency, theft rates, and medical costs. A $200 monthly premium in Alpharetta might reach $280 in downtown Atlanta for identical coverage and driving record.

Credit score influences your rate in Georgia because insurers correlate financial responsibility with driving behavior; drivers with credit scores below 620 pay roughly 30–50% more than those above 750. This relationship holds true even if your driving record is spotless. Coverage limits you select directly determine your premium: jumping from the state minimum 25/50/25 to 100/300/100 in bodily injury and property damage costs roughly 15–25% more monthly but provides substantially better financial protection.

Deductible Selection and Rate Trade-Offs

Deductible selection on collision and comprehensive coverage creates another trade-off: raising your deductible from $500 to $1,000 reduces your monthly premium by 15–25%, but you’ll pay that thousand-dollar amount out of pocket if you file a claim. Drivers with clean records and vehicles worth under $10,000 might skip collision and comprehensive, accepting the risk of total loss rather than paying premiums on a depreciating asset. Conversely, drivers with accidents or violations on their record, or those financing newer vehicles, should carry full coverage to avoid financial catastrophe.

Final Thoughts

Selecting the right auto insurance options Georgia requires matching your coverage to your actual risk, not just buying the cheapest policy available. Carrying only state minimums leaves you exposed to tens of thousands in personal liability if you cause a serious accident, while jumping to 100/300/100 bodily injury and property damage limits costs only marginally more monthly but shields your wages and assets from lawsuits. Similarly, collision and comprehensive coverage protects your vehicle investment, uninsured motorist coverage guards against Georgia’s 13% uninsured driver population, and optional coverages like medical payments and rental reimbursement fill gaps that could otherwise derail your finances after an accident.

Shopping multiple carriers for competitive rates is non-negotiable because premiums vary dramatically across insurers for identical coverage. Georgia’s average full-coverage premium sits around $273 monthly, but individual quotes range from $162 to $301 depending on the carrier and your profile. Gather quotes from at least three carriers using the same coverage levels, deductibles, and limits so you compare apples to apples, and ask each carrier about bundling discounts, good-driver discounts, telematics programs like Progressive Snapshot or Geico DriveEasy that reward safe driving, and loyalty discounts if you switch from another insurer.

Contact North Point Insurance Group today to secure the right coverage and stop overpaying for auto insurance. Our local Alpharetta agents work with multiple carriers to find coverage that matches your needs and budget without the call-center runaround. We handle the quote comparison, explain exactly what each coverage protects, and answer your questions about deductibles, limits, and discounts so you understand your policy before signing.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.