Auto Policy Quotes Georgia: Compare and Save

Georgia drivers face real pressure to find affordable coverage without sacrificing protection. Auto policy quotes in Georgia vary wildly depending on your age, driving history, and vehicle-sometimes by hundreds of dollars annually.

We at North Point Insurance Group know that comparing multiple quotes is the fastest way to cut your premiums. This guide walks you through exactly how to evaluate quotes, understand what affects your rate, and lock in savings.

Why Georgia Quotes Matter Right Now

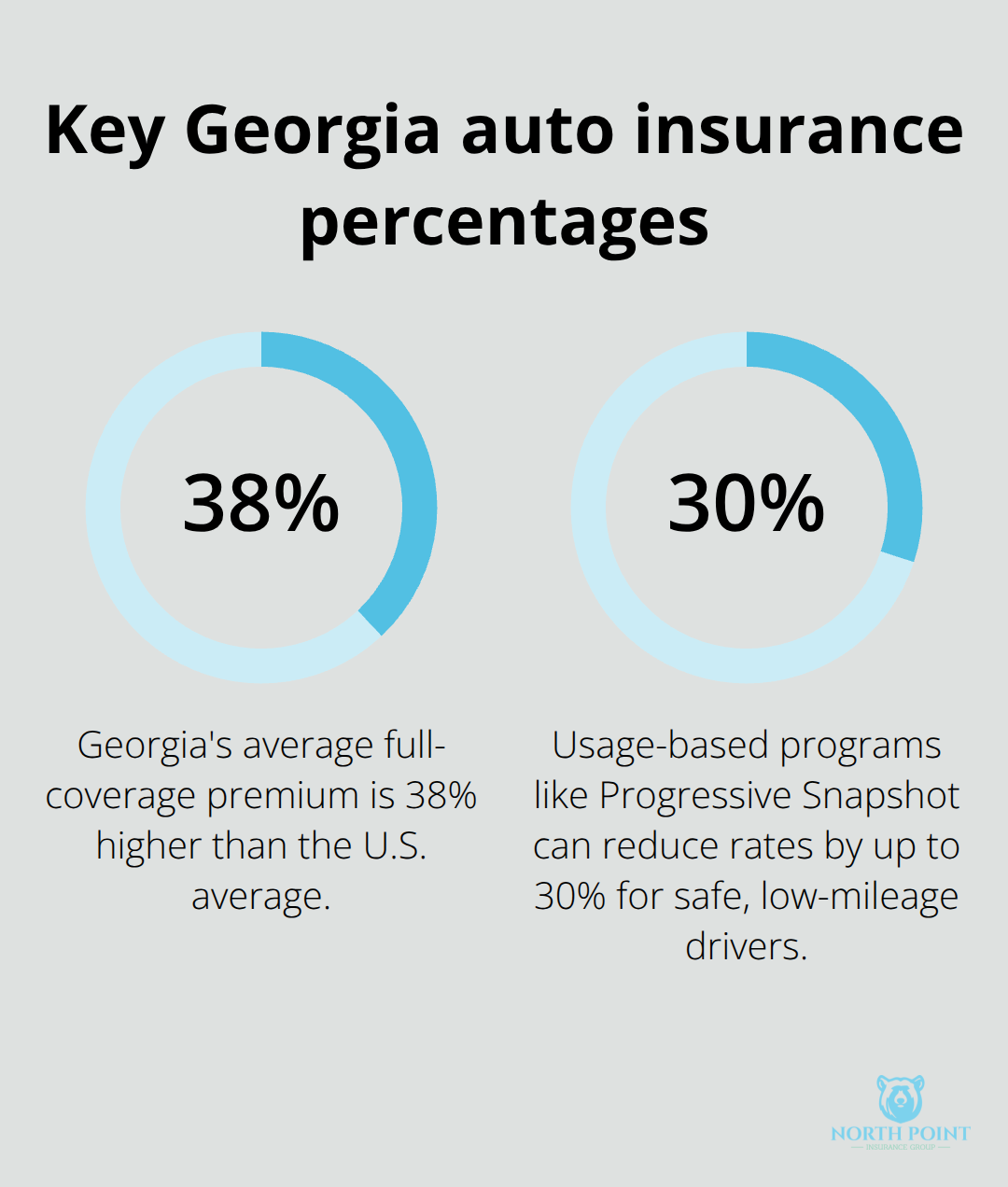

Georgia drivers spend about 2% of household income on auto insurance compared to roughly 1.5% nationally. That gap adds up fast-the state’s average full-coverage premium sits around $2,868 per year, roughly 38% higher than the U.S. average. Between 2014 and 2022, Georgia’s auto policy costs rose 5.6%, outpacing the national increase of 3.3%.

This isn’t random. Georgia ranks 47th in affordability nationwide, and the state consistently ranks high in vehicle thefts with 28,171 cars stolen in 2022–2023. A high share of underinsured motorists and frequent injury claims drive costs upward across the board.

Why Quotes Reveal Hidden Savings

Getting quotes isn’t optional in Georgia-it’s the only way to know whether you’re overpaying. State law requires minimum coverage of $25,000 per person and $50,000 per accident for bodily injury, plus $25,000 for property damage. Many drivers stop there and miss the real cost-saving opportunity. Comparison shopping reveals how much different insurers charge for the exact same coverage level, and the differences are substantial. Experian’s 2026 data shows minimum-coverage costs ranging from around $177 per month with Root to $251 with The General. Full-coverage quotes swing even wider: Travelers at roughly $188 monthly versus Elephant at $388. Those aren’t typos-a single carrier choice can cost you over $2,400 annually on full coverage alone.

How Your Driving Record Sets Your Price

Insurers weight your driving history heavily because it predicts future claims. A clean record significantly lowers your premium, while even one speeding ticket within three years may not raise rates-but two or more tickets typically do. At-fault accidents hit harder and usually raise premiums, though increases aren’t permanent with most carriers. The key detail most drivers miss: not-at-fault accidents and single-car accidents have variable impact depending on your insurer and Georgia’s specific rules, which is why quotes matter even after a fender-bender. Getting quotes from multiple carriers after any accident shows you which insurers treat your history most fairly. Some carriers forgive small claims more readily than others, and you won’t know your options without shopping.

Age and Location Create Price Tiers

Younger drivers face steeper rates partly because the CDC notes teens are almost three times more likely to be in a fatal crash than drivers aged 20 and older. Good Student discounts can offset some of this premium burden when eligible. Location within Georgia creates another pricing layer. Atlanta’s congestion and crime contribute to higher premiums, and urban areas with dense populations amplify accident risk. City-level monthly premiums in Georgia range from around $282 in Lawrenceville to $404 in Stone Mountain according to Experian data. Even within Atlanta, neighborhoods differ. These location-based differences disappear if you don’t compare quotes-you’ll simply accept whatever rate your current insurer offers without knowing whether a competitor charges 20% less in your specific ZIP code.

The differences in what you pay hinge on factors you can’t control (age, location) and factors you can (driving record, coverage choices). Understanding this split matters because it shapes which quotes to prioritize and how to read them.

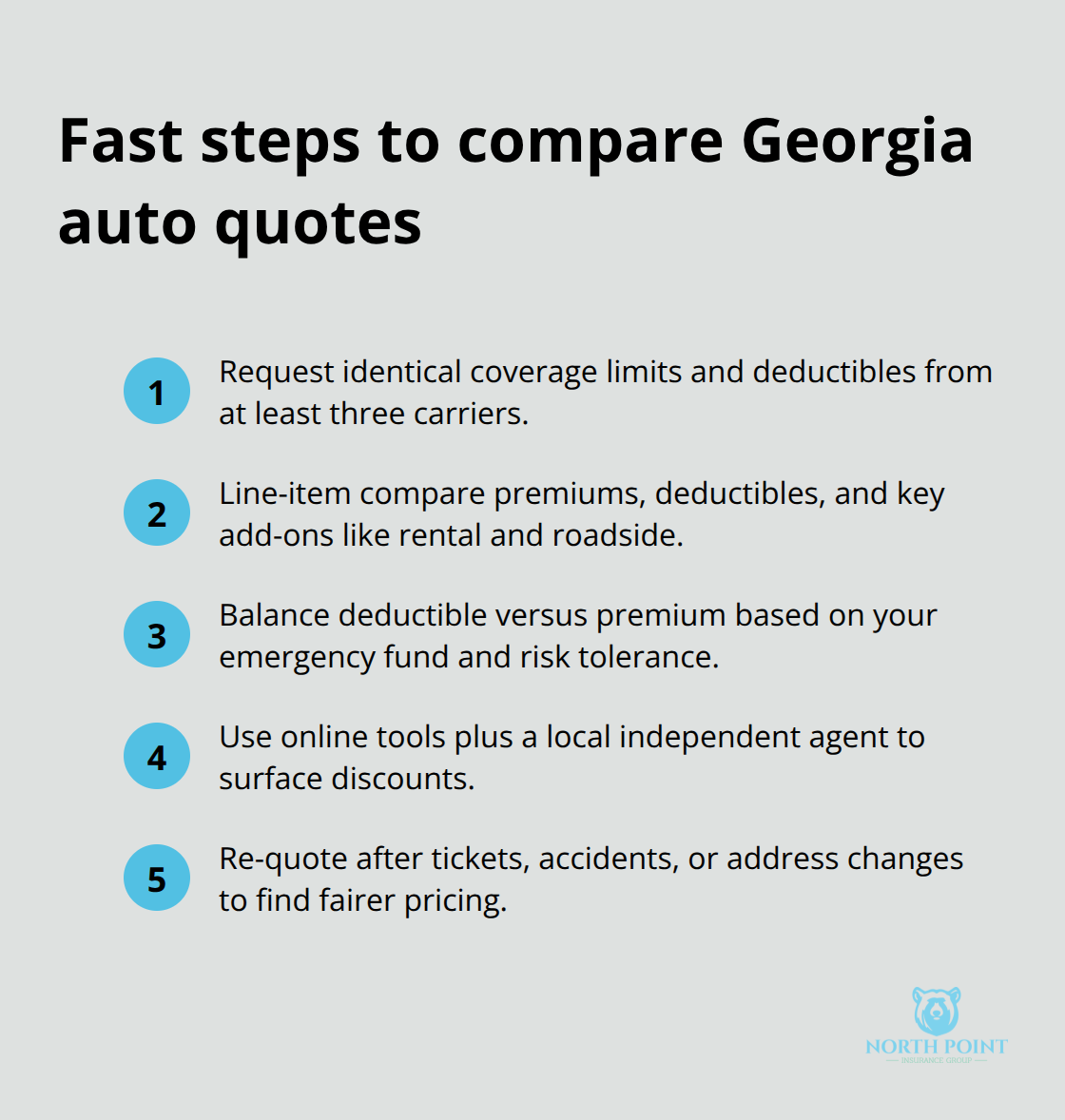

How to Compare Georgia Auto Quotes Without Wasting Hours

Comparing quotes means more than collecting a handful of numbers and picking the lowest one. Georgia’s insurance market has wide price swings because carriers weight risk factors differently, and a cheap quote on bare-bones coverage won’t protect you if an accident drains your savings. The real skill is evaluating what each quote actually covers and whether the deductible-to-premium trade-off matches your financial situation.

Request Identical Coverage Across All Quotes

Start with at least three quotes using the same coverage levels across all carriers. Experian’s 2026 data shows that full-coverage quotes in Georgia range from Travelers at roughly $188 monthly to Elephant at $388 monthly for the same driver profile. That $200-per-month gap isn’t random pricing-it reflects how each carrier assesses Georgia’s high theft rate, litigation costs, and accident frequency.

When you request quotes, specify identical liability limits above Georgia’s $25,000/$50,000 minimum, the same collision and comprehensive deductibles, and the same vehicle. This apples-to-apples approach exposes real rate differences instead of coverage variations masking price. Many drivers quote $500 deductibles without realizing they could drop to $250 for only $30 more monthly, or jump to $1,000 and save $40. The right deductible depends on your emergency fund-if you can’t pay $1,000 out-of-pocket after an accident, a lower deductible protects you from financial stress even if premiums cost slightly more.

Use Online Tools and Local Agents Together

Online quoting tools let you compare more than 30 carriers at once, which beats calling individual insurers and waiting for callbacks. However, online tools work best when you also talk to a local agent because Georgia’s rate complexity-urban versus rural pricing, local claim patterns, and insurer-specific discounts-sometimes reveals savings tools alone miss.

An independent agent shops multiple carriers on your behalf and explains which discounts actually apply to your situation, whether that’s bundling auto with home, paying in full, or using a usage-based program like Progressive Snapshot. Many Georgia drivers qualify for discounts they don’t know exist: continuous coverage discounts for maintaining uninterrupted insurance, online purchase discounts, and good-driver discounts. A local agent catches these faster than online forms because they know which carriers in Georgia offer what.

Look Beyond the Bottom-Line Premium

After collecting three to five quotes, don’t just compare the bottom-line premium. Read what each quote includes for roadside assistance, rental coverage limits, and uninsured motorist protection. Some carriers charge extra for 24/7 roadside assistance while others bundle it; some offer $30-per-day rental coverage while others offer $45. These add-ons shift your true cost and claim experience if you need them.

The cheapest quote that excludes rental coverage becomes expensive the day your car is in the shop and you need a loaner. Location within Georgia also affects which add-ons matter most-drivers in Atlanta face higher theft risk, making comprehensive coverage more valuable than drivers in rural areas might think. Your vehicle’s repair costs and safety features influence whether a carrier’s pricing reflects your actual risk profile or simply applies a broad formula. These details separate a quote that looks cheap from one that actually protects your finances.

The next step involves understanding which rate factors you can control and which ones you cannot, so you know where to focus your savings efforts.

What Really Drives Your Georgia Auto Insurance Rate

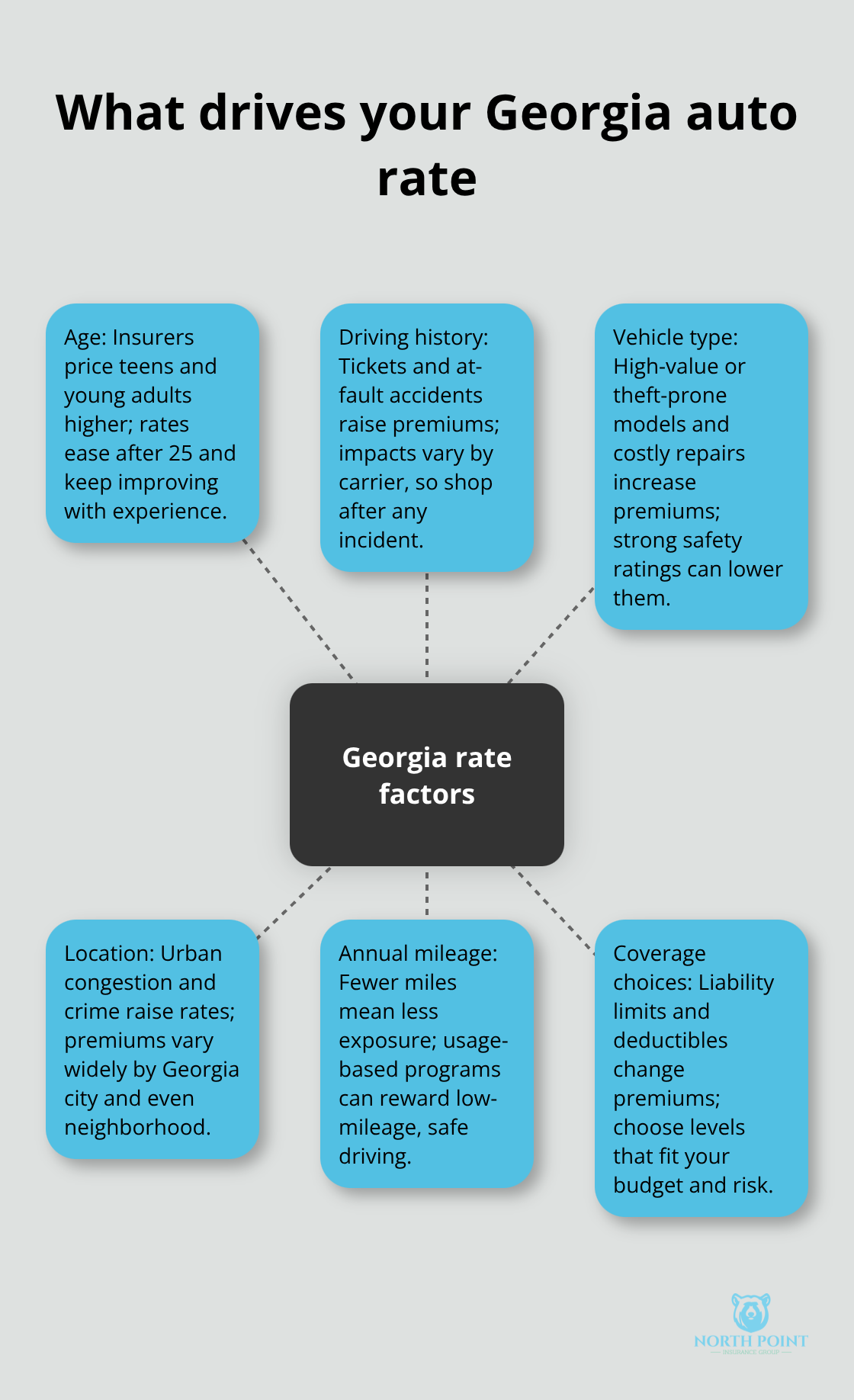

Your age, vehicle, location, and annual mileage create the foundation of your Georgia insurance quote. Understanding how each factor works lets you spot where savings actually hide. Georgia’s insurance market punishes certain risk profiles heavily while ignoring others, which means two drivers with identical ages and vehicles can pay wildly different premiums based on one detail.

Age and Driving History Set Your Starting Point

Age matters most for teens and young adults because the CDC confirms teens face almost three times higher risk of fatal crashes than drivers aged 20 and older. Insurers charge dramatically higher rates before age 25 to reflect this risk. That penalty softens significantly after 25 and continues dropping through your 30s and 40s. A 19-year-old might pay $400 monthly for full coverage while a 35-year-old with the same vehicle and driving record pays $180, but this age premium isn’t permanent.

If you’re young, your actual rate depends heavily on whether you qualify for Good Student discounts. Carriers offer these when you maintain a 3.0 GPA or higher. Your driving history compounds the age factor because a single accident or two speeding tickets within three years can add $50 to $100 monthly to what you already pay. At-fault accidents hit harder than not-at-fault claims, though Georgia rules vary by insurer. This is exactly why you need quotes from at least three carriers after any accident to see which one treats your history most fairly.

Vehicle Type and Repair Costs Shape Your Premium

Vehicle type and repair costs determine whether an insurer sees your car as low-risk or expensive to fix. Georgia’s high theft rate makes this calculation sharper than in most states. Sports cars, convertibles, and high-value vehicles like Teslas cost more to insure because repair and replacement expenses run higher. Even standard sedans differ in premium based on safety ratings and theft frequency.

The make and model of your car influences premiums due to repair costs and safety features. A vehicle with strong crash-test ratings and modern safety technology may qualify for lower rates than an older model with the same market value. Theft-prone vehicles cost more to insure across Georgia, particularly in urban areas where theft risk peaks.

Location Within Georgia Creates Dramatic Price Tiers

Your location within Georgia creates pricing tiers that most drivers completely miss because they never compare quotes across different ZIP codes. Experian data shows monthly premiums ranging from $282 in Lawrenceville to $404 in Stone Mountain for identical coverage. Atlanta itself varies by neighborhood based on theft, accident frequency, and population density. Urban areas with congestion naturally cost more than rural zones, but the gap between one Atlanta neighborhood and another can hit $50 to $100 monthly.

Living in more densely populated areas increases risk for theft or vandalism, raising premiums for comprehensive and collision coverages. Atlanta’s traffic, congestion, and crime contribute to higher premiums, though they are not the sole factors. Georgia ranks ninth in vehicle thefts nationwide, which pushes comprehensive coverage costs upward statewide.

Annual Mileage and Usage Patterns Lower Your Rate

Annual mileage directly affects your premium because more time on the road means higher accident exposure. Someone driving 25,000 miles yearly pays more than someone driving 8,000 miles. Progressive’s usage-based Snapshot program lets you lower your rate by up to 30 percent if you drive safely and infrequently, which proves that insurers reward low-mileage drivers willing to prove their habits.

If you work from home or drive only occasionally, mentioning low annual mileage to agents during quote requests often triggers better pricing that online tools miss. Usage-based pricing personalizes your rate based on actual driving habits, so safer driving can lower your premium significantly. This approach works particularly well for Georgia drivers who can document low mileage or safe driving patterns through monitoring programs.

Final Thoughts

Saving money on Georgia auto insurance starts with one action: comparing quotes from multiple carriers. Experian’s 2026 research shows full-coverage premiums swinging from $188 monthly with Travelers to $388 with Elephant for identical driver profiles-that $240-per-month gap equals $2,880 annually. Minimum-coverage quotes range from $177 with Root to $251 with The General, meaning your carrier choice alone determines whether you pay $2,124 yearly or $3,012 for the same protection level.

Georgia drivers already pay 38% more than the national average for auto insurance, but you control which carrier you select and how you structure your coverage. Request identical coverage across at least three quotes so you compare apples to apples, not coverage variations that mask true price differences. Talk to a local agent alongside online tools because Georgia’s rate complexity-urban versus rural pricing, local claim patterns, and insurer-specific discounts-reveals savings that online forms miss.

Your driving record, vehicle type, location within Georgia, and annual mileage all influence your rate, but only the quote comparison reveals how much each carrier weights these factors. One insurer might charge $50 more monthly because they heavily penalize your location while another barely adjusts for it. We at North Point Insurance Group shop multiple carriers to find you competitive pricing tailored to your actual situation, and our local agents understand Georgia’s insurance landscape and catch discounts that online tools miss.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.