Boat Insurance Deductibles Georgia: Understanding Your Costs

Boat insurance deductibles in Georgia directly affect how much you’ll pay out of pocket when you file a claim. The deductible you choose can save you hundreds on premiums or cost you thousands if an accident happens.

At North Point Insurance Group, we help boat owners understand these trade-offs so you can make the right choice for your situation. This guide breaks down everything you need to know about deductibles and how to pick the amount that fits your budget and boat.

Boat Insurance Deductibles in Georgia: What You Actually Pay

How Deductibles Work in Your Boat Insurance

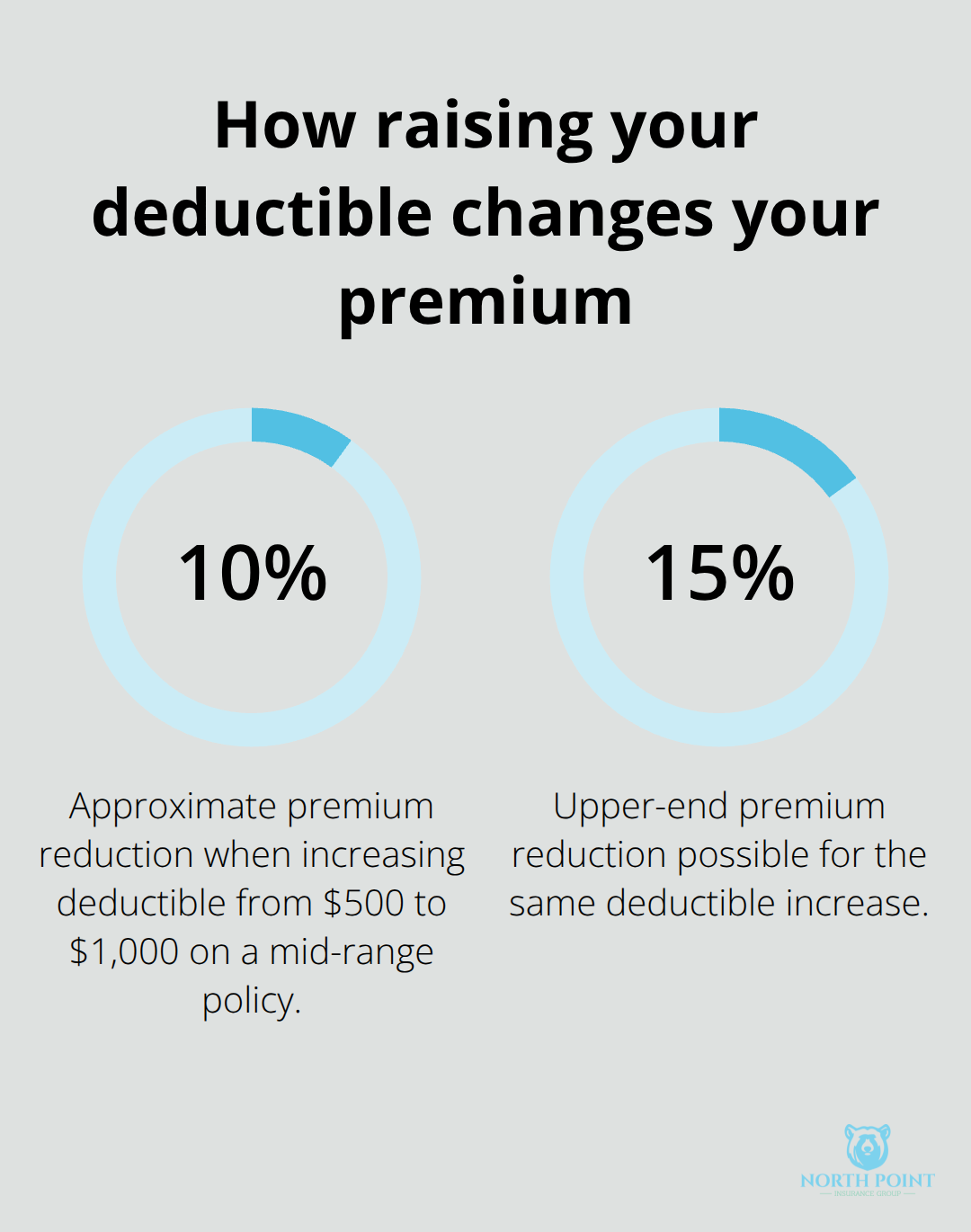

A boat insurance deductible is the amount you pay out of pocket when you file a claim, and your insurer pays the rest. If your boat suffers $5,000 in damage and you have a $1,000 deductible, you cover the first $1,000 and the insurance company covers the remaining $4,000. The relationship between deductibles and premiums is straightforward: higher deductibles lower your annual premium, while lower deductibles raise it. In Georgia, boat owners typically choose deductibles ranging from $500 to $2,500, though some policies allow deductibles as low as $250 or as high as $5,000. Increasing your deductible from $500 to $1,000 can reduce your premium by 10–15%, which adds up to $35–$50 annually on a mid-range policy. For boaters with solid emergency funds and clean claims histories, this trade-off makes financial sense.

The Math Behind Your Deductible Decision

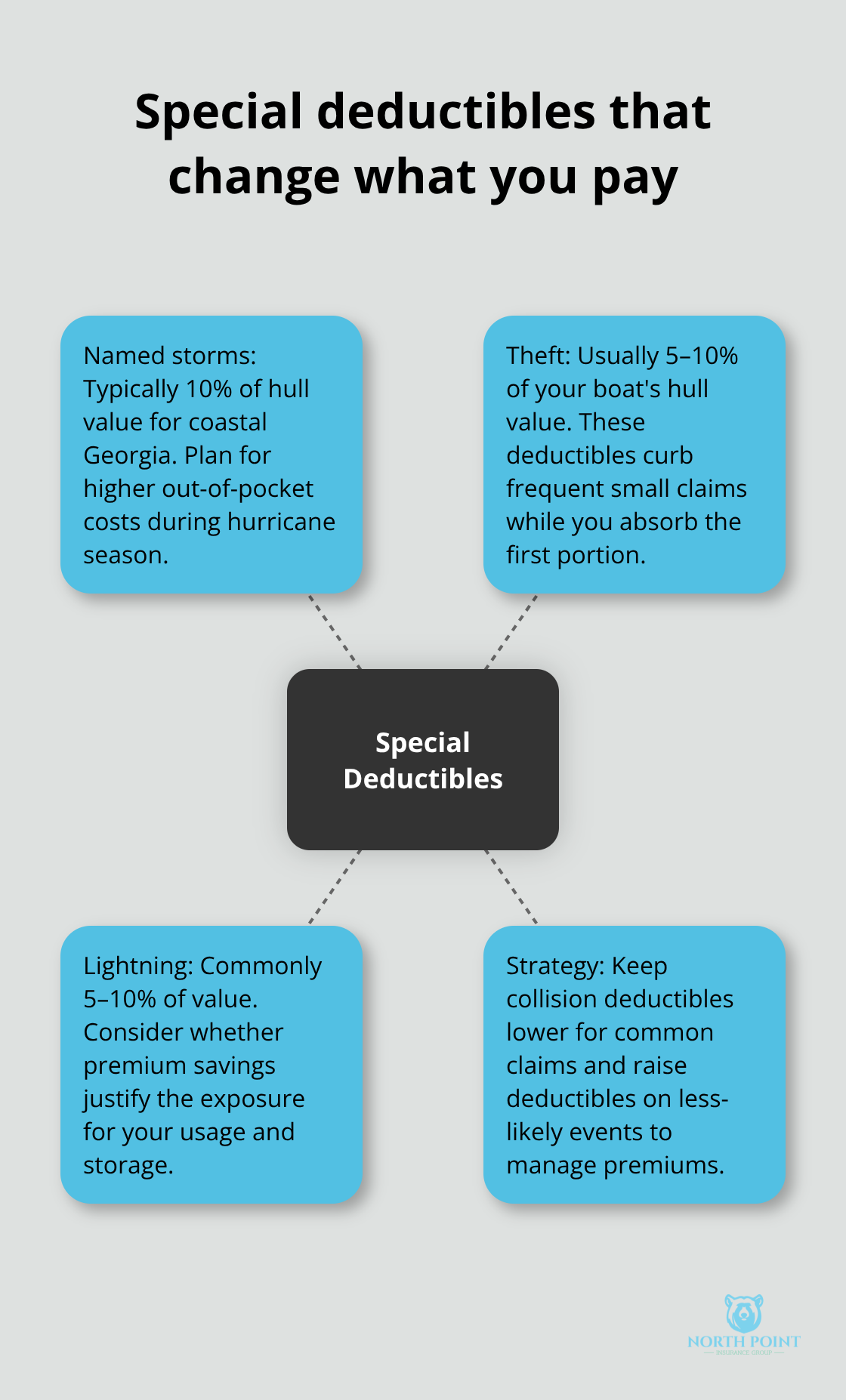

Physical damage claims in Georgia average $2,000–$5,000 per incident, meaning most boaters never hit their deductible in any given year. If you file a claim for $3,000 in damage with a $500 deductible, you pay $500; with a $1,000 deductible, you pay $1,000. Over five years without a claim, that higher deductible saves you money-you pocket $175–$250 in premium reductions. However, special deductibles apply to specific loss types. Theft and lightning damage typically carry deductibles of 5–10% of your boat’s hull value, and named storm deductibles run 10% of hull value, especially along Georgia’s coast. A $50,000 boat facing a named storm deductible means you pay $5,000 out of pocket for hurricane damage. This reality matters most for coastal Georgia boaters who must weigh whether the premium savings justify the risk exposure.

Matching Your Deductible to Your Financial Reality

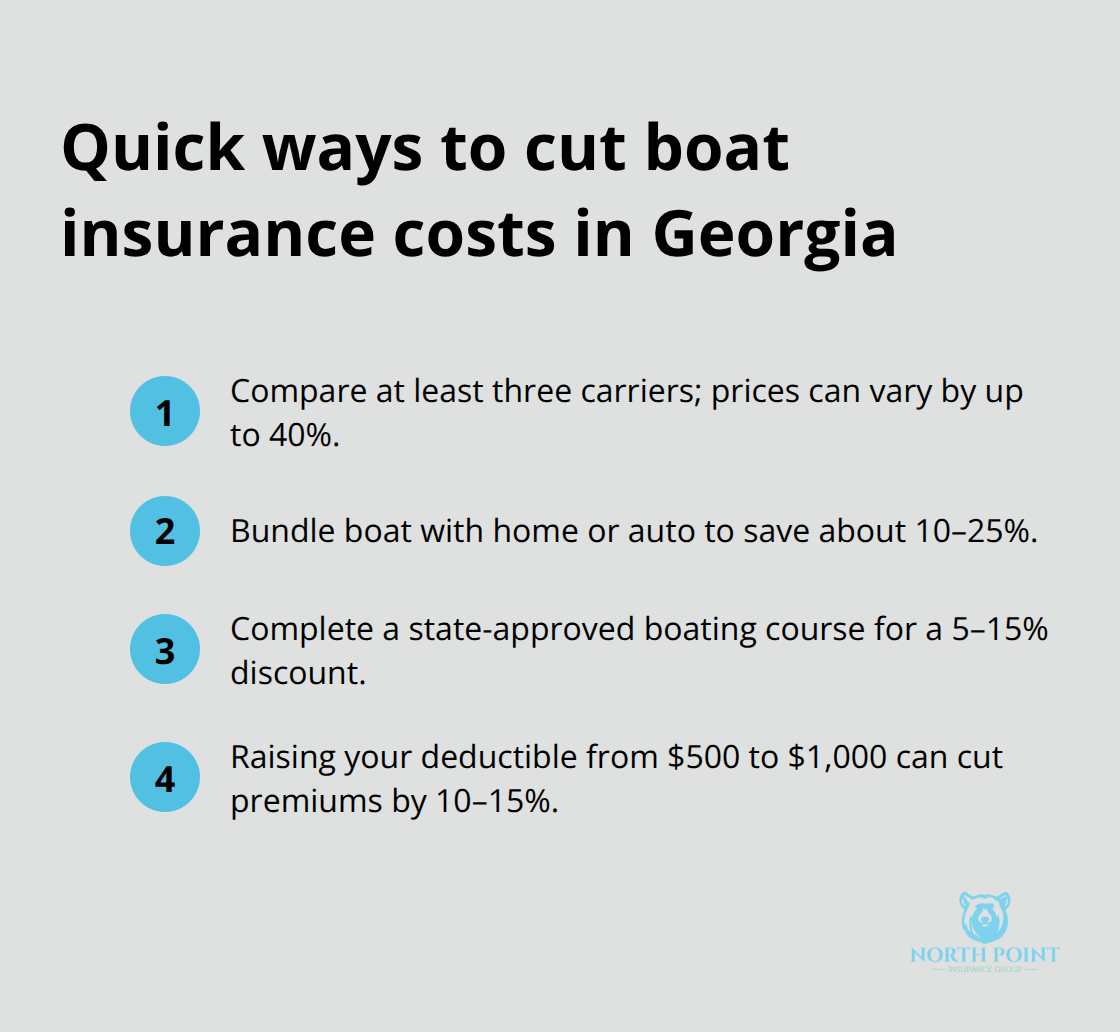

Your financial situation should drive your deductible choice more than anything else. If you have $3,000–$5,000 in readily available savings and rarely use your boat in rough conditions, a $1,500 or $2,000 deductible is reasonable and saves you money monthly. If you finance your boat, lenders typically require comprehensive and collision coverage, but they don’t dictate deductible amounts-that choice remains yours. Newer or well-maintained boats work well with agreed value hull coverage paired with a moderate $1,000 deductible, which strikes a balance between affordability and protection. Conversely, if your boat sits in dry storage most of the year or docked at a secure marina, theft and weather risk drop significantly, making a higher deductible acceptable. Boaters born after January 1, 1998 who complete a state-approved boating education course can reduce premiums by 5–15%, which sometimes offsets the savings from raising your deductible. The key is honesty: pick a deductible you can actually afford to pay if something goes wrong, not the one that looks cheapest on paper.

Special Deductibles That Change Your Out-of-Pocket Costs

Named storms, theft, and lightning each carry their own deductible structure separate from your standard collision or comprehensive deductible. Named storm deductibles (typically 10% of hull value) apply specifically to hurricane or tropical storm damage along Georgia’s coast, creating a significant out-of-pocket expense during storm season. Theft deductibles (5–10% of hull value) protect insurers from frequent small claims while you absorb the first portion of any theft loss. Lightning damage follows similar logic, with deductibles ranging from 5–10% of your boat’s value.

Understanding these separate deductibles prevents surprises when you file a claim-you’ll know exactly what you owe before damage occurs. This knowledge helps you decide whether to accept higher deductibles on less-likely events (like lightning) while keeping lower deductibles on more common claims (like collision). Your next step involves comparing quotes from multiple carriers to see how different deductible levels affect your specific boat and coverage needs.

Coverage Types and What You Actually Pay When You File

Collision Coverage: Your Most Common Claim

Collision coverage protects your boat from damage caused by impact with another boat, dock, or object, and it accounts for most Georgia boat owner claims. Your collision deductible directly determines your out-of-pocket cost after an accident-a $500 deductible means you pay $500 toward repairs, while your insurer covers the rest. Fishing boats and pontoons in Georgia typically carry collision deductibles ranging from $500 to $1,500, with premiums dropping roughly 10–15% when you increase from $500 to $1,000. The math favors cautious operators: physical damage claims average $2,000–$5,000 per incident, so your deductible rarely consumes your entire claim payout.

Comprehensive Coverage and Named Storm Deductibles

Comprehensive coverage handles theft, fire, weather, and vandalism-the losses you cannot control. Georgia coastal boaters face named storm deductibles of 10% of hull value on top of standard comprehensive deductibles, meaning a $50,000 boat requires a $5,000 out-of-pocket payment for hurricane damage. This two-tier deductible structure catches many boat owners off guard, so understanding it before storm season arrives prevents financial shock. Theft and lightning deductibles typically run 5–10% of your boat’s hull value, creating additional out-of-pocket expenses for these specific loss types.

Liability Coverage: Where Deductibles Matter Less

Liability coverage pays for injuries or property damage you cause to others, and most policies carry no deductible on liability claims themselves. Instead, your liability deductible applies to your own defense costs in certain situations, not to the injured party’s settlement. This distinction matters because liability claims can range from $50,000 to $500,000 or more depending on severity, making your liability limits far more important than your deductible. Georgia boaters should maintain at least $300,000 in liability coverage, with $500,000 or higher recommended if you frequently host guests or operate a high-value vessel.

Balancing Deductibles Across Coverage Types

Choosing deductibles across these three coverage types requires balancing premium savings against real claim frequency and your ability to pay. If your boat sits in secure marina storage most of the year, raising your comprehensive deductible to $1,500 makes sense because theft and weather risk drop significantly, saving you $50–$75 annually. Conversely, collision deductibles should stay lower if you actively operate your boat in busy waterways where fender-benders happen-paying $500 out of pocket beats paying $1,500 when accidents are more likely. Bundling boat coverage with auto or home policies saves 10–25% overall, which often covers the difference between deductible levels and gives you flexibility to choose lower deductibles without breaking your budget.

Shopping Multiple Carriers for Real Savings

Named storm deductibles along Georgia’s coast are non-negotiable and high, so if you operate near the coast, accept that expense as part of your actual cost of ownership rather than trying to game the system with higher standard deductibles elsewhere. The strongest move involves comparing quotes from multiple carriers with identical coverage and deductible combinations-expect price variations up to 40% for the same boat and same deductible, which means shopping around saves far more than tweaking deductibles alone. Once you understand how these deductible structures affect your specific boat and usage patterns, you can move forward with confidence to assess your boat’s value and risk factors.

How to Match Your Boat’s Value and Risk to the Right Deductible

Know Your Boat’s True Market Value

Choosing a deductible means matching three concrete realities: what your boat is worth, what risks it actually faces, and what you can afford to pay immediately if damage occurs. Start by prioritizing recent listings and past sales to estimate your boat’s current market value, not its listing price. Pull your boat’s hull ID and registration, then check recent sales of identical models in Georgia to establish accurate value. This step matters because undervaluing your boat leads to agreed value disputes after a claim, while overvaluing it inflates your premiums unnecessarily.

Assess Your Actual Risk Based on Storage and Usage

Next, assess your actual risk exposure based on where and how you operate the boat. A boat stored year-round in dry storage at a secure facility faces minimal theft and weather risk, making a $1,500 or $2,000 deductible financially smart because comprehensive claims rarely happen. A boat operated frequently in busy coastal Georgia waters near Savannah or St. Simons Island faces collision risk from congestion, docking incidents, and weather, which argues for keeping collision deductibles at $500 or $750 to minimize out-of-pocket costs when accidents occur. Coastal operators also must accept that named storm deductibles run 10% of hull value regardless of your choices-a $40,000 boat means $4,000 out of pocket for hurricane damage-so don’t waste premium savings elsewhere trying to offset that unavoidable cost.

Match Your Deductible to Your Financial Reserves

Your emergency fund size should directly determine your deductible floor. If you have $2,000 in readily accessible savings, a $1,500 deductible is reasonable; a $500 deductible is not because paying it after a claim would deplete your financial cushion entirely. Conversely, if you maintain $8,000 or more in emergency reserves and your boat is financed, a $2,000 deductible paired with agreed value hull coverage makes sense because you’re protected against both catastrophic loss and the depreciation disputes that plague actual cash value claims. Boaters who complete a state-approved boating education course receive 5–15% premium discounts, which sometimes outweighs deductible increases in total cost.

Compare Multiple Quotes Across Deductible Tiers

The real decision comes down to comparing actual quotes from multiple carriers with identical boat specifications and coverage combinations. Get quotes at three different deductible tiers-say $500, $1,000, and $1,500-from at least three carriers to see which combination delivers the lowest total annual cost plus manageable out-of-pocket exposure. This comparison reveals whether saving $40 per year on premiums by raising your deductible from $500 to $1,000 is worth the extra $500 you’d pay if a claim occurs. Our agents at North Point Insurance Group shop 20+ carriers to surface these exact comparisons, helping you identify which deductible truly fits your boat, usage, and budget rather than settling for what looks cheapest in isolation.

Final Thoughts

Boat insurance deductibles in Georgia force you to choose between lower monthly premiums and higher out-of-pocket costs when damage strikes. Your boat’s value, storage location, and emergency fund size should drive this decision far more than the premium savings alone. Named storm deductibles along Georgia’s coast run 10% of your hull value regardless of your choices, so coastal operators must accept that reality as part of ownership costs rather than trying to offset it with higher deductibles elsewhere.

Shopping quotes from multiple carriers at three different deductible tiers reveals which combination delivers the lowest total annual cost plus manageable out-of-pocket exposure. Price variations reach up to 40% for identical coverage across carriers, meaning comparison shopping saves far more than tweaking deductibles alone. Bundling boat coverage with auto or home policies saves 10–25% overall, and completing a state-approved boating education course reduces premiums by 5–15%, both of which give you flexibility to choose lower deductibles without stretching your budget.

We at North Point Insurance Group shop 20+ carriers to surface these exact comparisons and help you identify which deductible truly fits your boat, usage, and budget. Contact North Point Insurance Group today to get quotes tailored to your boat and see how the right deductible choice protects both your finances and your peace of mind on the water.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.