Georgia Boat Insurance Basics: What You Need to Know

Georgia boat insurance basics aren’t optional-they’re a legal requirement and financial safeguard every boat owner needs. Whether you’re navigating inland lakes or coastal waters, the right coverage protects your investment and shields you from liability claims.

At North Point Insurance Group, we’ve helped countless Georgia boat owners find policies that match their specific needs. This guide walks you through the coverage types, selection process, and practical steps to get properly protected.

Why Georgia Boat Insurance Really Matters

Georgia doesn’t legally require boat insurance for private recreational vessels, but that absence of law doesn’t mean you can skip coverage. Lenders will demand comprehensive and collision protection if you finance your boat, marinas will require liability proof before they let you dock, and one serious accident will wipe out your assets far faster than any premium you’ll ever pay. The average Georgia boat insurance policy costs about $344 per year-roughly $29 monthly-which is genuinely cheap protection against a lawsuit that could cost you hundreds of thousands of dollars. If someone gets injured on your boat or you damage another person’s watercraft or dock, liability claims escalate quickly, and without coverage, you’re personally responsible for every penny.

When Accidents Cost More Than Years of Premiums

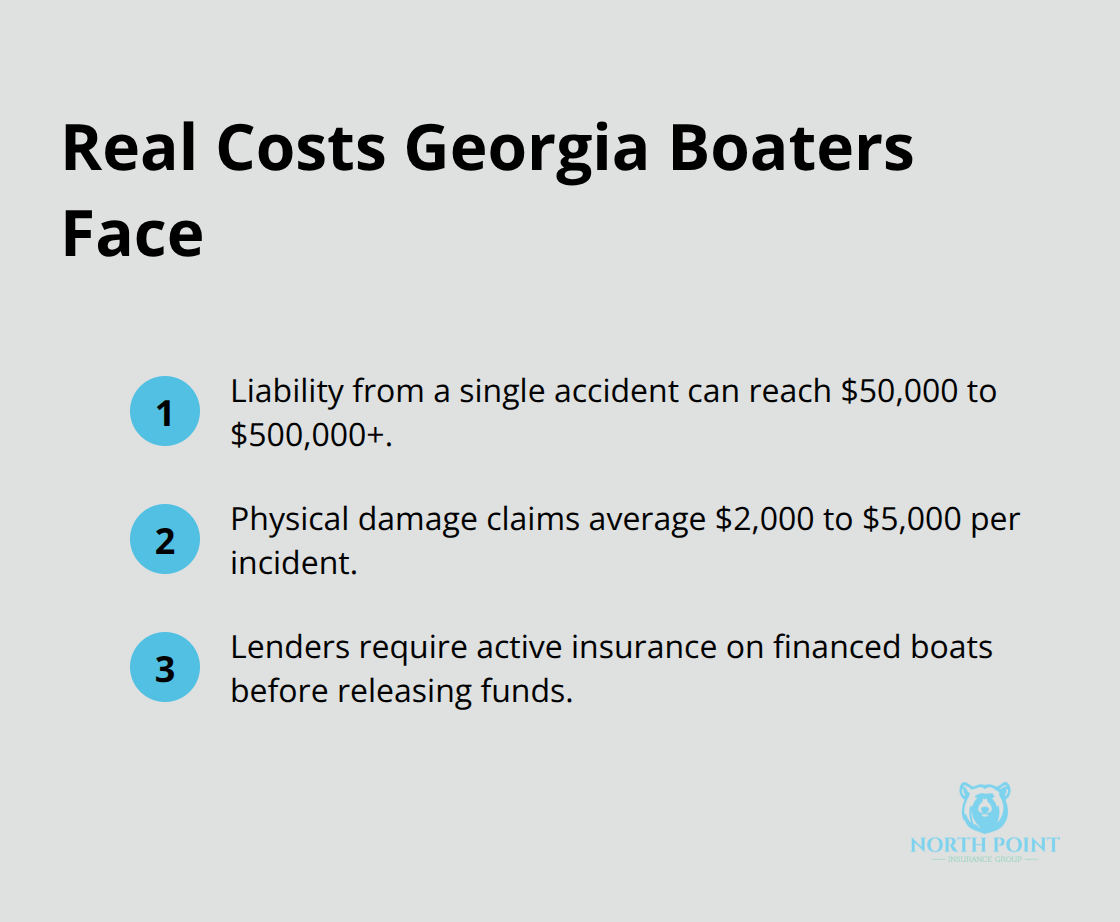

A single boating accident can result in $50,000-$500,000+ in liability claims. Without insurance, you face full liability, and creditors can pursue wage garnishment and asset seizure for years. Comprehensive coverage protects against theft, vandalism, weather damage, and fire-real risks on Georgia’s lakes and coastal waters where storms strike without warning. Collision coverage handles damage from hitting other boats, docks, or underwater objects, which happens more often than most boat owners expect.

Physical damage claims average $2,000 to $5,000 per incident, according to industry data, making hull coverage far cheaper than self-insuring. If your boat is financed, your lender won’t release the loan until you maintain active coverage, so you’re paying for insurance anyway-the only question is whether you’re buying enough.

Liability Forms Your Foundation

Bodily injury and property damage liability should anchor your policy. Try a minimum of $300,000 in liability limits, though $500,000 makes more sense if you frequently have guests aboard or own a higher-value vessel. Georgia boaters born after January 1, 1998 must complete a state-approved boater education course to operate motorized vessels, and taking that course reduces your premium by 5 to 15 percent while improving your safety knowledge. Your policy should cover medical payments for passengers injured on your boat regardless of fault, protecting you from guest lawsuits. Uninsured boater coverage shields you if another boat operator causes damage and carries no insurance-a genuine risk on Georgia waters where not all boaters carry adequate protection.

Why Coverage Gaps Leave You Exposed

Your homeowners policy won’t cover your boat. Standard homeowners insurance excludes most motorized vessels and on-water use, leaving you completely unprotected if you rely on that coverage. Marinas and lenders recognize this gap and require proof of dedicated boat insurance before they’ll work with you. One accident without proper coverage transforms a manageable insurance claim into a personal financial catastrophe that follows you for years. The next section walks you through the specific coverage types that actually protect your boat and your wallet.

Types of Boat Insurance Coverage Explained

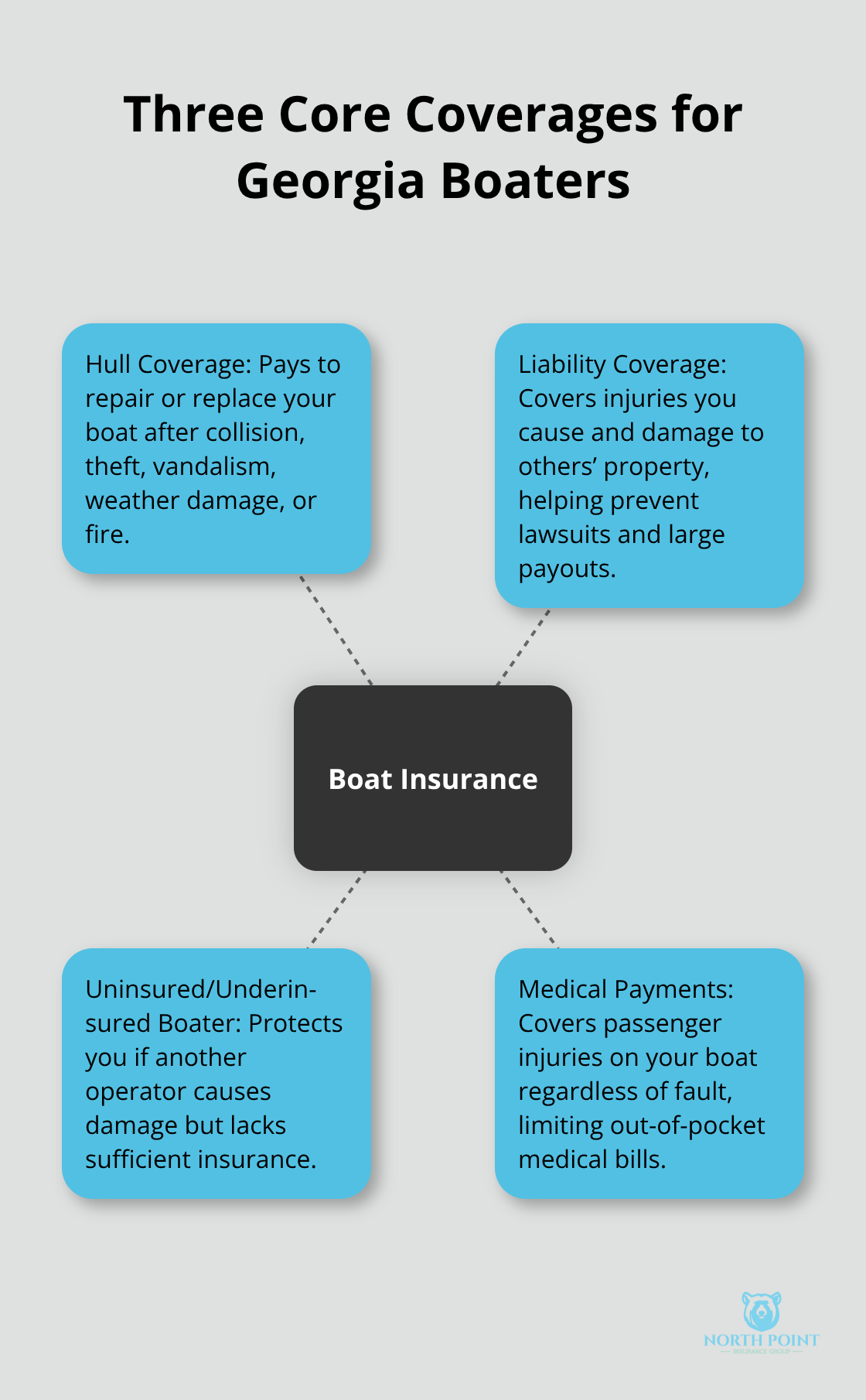

Hull coverage pays to repair or replace your boat after collision, theft, vandalism, weather damage, or fire-the physical damage that threatens your investment. You’ll choose between actual cash value, which depreciates your boat’s worth over time, or agreed value, which locks in a set payout amount before a loss occurs. Agreed value makes sense for newer boats or well-maintained vessels because you avoid depreciation arguments with your insurer after an accident.

Hull Coverage Protects Your Boat’s Physical Value

The average Georgia boat owner pays $200 to $350 annually for pontoon coverage and $250 to $450 for fishing boats, according to industry pricing data, with hull protection forming the bulk of that cost. If you finance your boat, your lender demands comprehensive and collision coverage as a condition of the loan, so you’re purchasing this protection regardless-the smarter move is selecting agreed value to protect your actual investment. Deductibles matter tremendously here: choosing a $1,000 deductible instead of $500 can cut your premium by 10 to 15 percent, but only if you can afford that out-of-pocket cost after an accident.

Most Georgia boaters underestimate how often collisions happen on lakes and near docks, where underwater obstacles, shallow water, and tight spaces create constant risk. Physical damage claims average $2,000 to $5,000 per incident, according to industry data, making hull coverage far cheaper than self-insuring.

Liability Coverage Shields You From Lawsuits

Liability coverage protects you when you injure someone or damage their property while operating your boat. Bodily injury liability covers medical expenses, lost wages, and pain-and-suffering claims if a passenger gets hurt or you hit another boat’s operator, while property damage liability covers repairs to docks, other watercraft, or equipment you damage. Try a minimum of $300,000 in combined liability limits, though $500,000 makes stronger sense if you host guests frequently or own a high-value vessel.

Medical payments coverage operates independently of liability and covers your passengers’ injuries regardless of fault, eliminating guest lawsuits before they start-this coverage costs roughly $30 to $50 annually and prevents thousands in legal expenses. Uninsured and underinsured boater coverage shields you when another operator causes damage but carries insufficient or zero insurance, a genuine threat on Georgia waters where compliance rates remain inconsistent.

Uninsured Boater Coverage Fills Critical Gaps

This coverage typically costs $50 to $100 per year and covers your medical expenses, lost income, and damage to your boat when an uninsured boater hits you, making it essential protection that many boat owners foolishly skip. A single boating accident can result in $50,000-$500,000+ in liability claims, and without uninsured boater protection, you face full liability if the other operator carries no insurance. Your policy should cover medical payments for passengers injured on your boat regardless of fault, protecting you from guest lawsuits and unexpected medical bills that accumulate quickly after an accident.

Understanding these three core coverage types gives you the foundation to select a policy that actually matches your boat and your boating habits. The next step involves assessing your specific boat’s value, how you use it, and what coverage limits make sense for your situation-decisions that directly impact both your premium and your protection level.

Picking the Right Coverage for Your Boat

Choosing boat insurance isn’t about finding the cheapest policy-it’s about matching coverage to your actual boat, how you use it, and what you can afford to pay out of pocket after a loss. Most Georgia boat owners make this decision backwards, starting with price instead of starting with their boat’s value and replacement cost. The right approach begins with honest answers about three things: what your boat actually costs to replace, how you use it, and what deductible you can realistically afford.

Start With Your Boat’s Details

If your boat is financed, your lender has already made some of these decisions for you by demanding comprehensive and collision coverage, but you still control the coverage limits and deductible levels that directly impact your premium. Start by gathering your boat’s hull identification number, registration documents, current market value, and details about where you store it and how often you use it. Industry data shows pontoon boats in Georgia run $200 to $350 annually for coverage, while fishing boats average $250 to $450 per year-but these numbers swing dramatically based on your boat’s horsepower, age, and whether you choose actual cash value or agreed value coverage.

If your boat is newer or well-maintained, agreed value coverage pays the full insured amount and eliminates depreciation arguments after a loss, making it worth the slightly higher premium compared to actual cash value, which pays a depreciated amount and leaves you short if an accident occurs.

Compare Quotes Across Multiple Carriers

Comparing quotes across multiple carriers matters far more than most boat owners realize because premium variation for identical coverage can exceed 40 percent between insurers. Request quotes from at least three carriers and be specific about your boat’s details-rushing through this process or providing vague information produces useless quotes that don’t reflect your actual cost. When you compare quotes, pay attention to what’s included versus what’s optional: towing coverage, fuel spill liability, wreck removal, and fishing equipment protection all cost extra, and bundling your boat policy with auto or homeowners coverage typically saves 10 to 25 percent according to industry data.

Select Deductibles That Match Your Budget

The deductible selection directly controls your monthly payment, and choosing a $1,000 deductible instead of $500 can cut your premium by 10 to 15 percent, but only make that trade if you can genuinely afford to pay $1,000 out of pocket after an accident without financial strain. Set your liability limits based on your assets and guest exposure-$300,000 represents the bare minimum, but $500,000 or higher makes sense if you frequently host passengers or own significant assets that creditors could pursue after a lawsuit.

Local independent agents shop multiple carriers to find real price differences and coverage options tailored to your specific boat and boating habits, delivering personalized guidance that call centers simply can’t match.

Final Thoughts

Georgia boat insurance basics protect your investment and your assets from the financial devastation that follows a single accident. A $344 annual policy costs roughly $29 monthly and shields you from liability claims exceeding $500,000, wage garnishment, and asset seizure that lasts for years. Without coverage, one collision transforms your boat from an asset into a liability that creditors pursue relentlessly.

Hull coverage handles collision, theft, weather damage, and fire, while liability shields you from lawsuits when you injure someone or damage property. Uninsured boater coverage protects you when another operator carries insufficient insurance-a genuine risk on Georgia waters where compliance remains inconsistent. These three coverage types form your complete defense against the threats Georgia boaters face most often.

Contact North Point Insurance Group today to receive a personalized quote that matches your boat and your budget. Our agents deliver the personal, professional guidance that transforms boat insurance from a confusing obligation into straightforward protection you actually understand. We handle the comparison work so you don’t waste hours on the phone getting generic quotes that don’t reflect your situation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.