Georgia Landlord Insurance Basics: Essential Guidance

Owning rental property in Georgia comes with real financial risk. Standard homeowners insurance won’t protect you from tenant-related claims or lost rental income, leaving your investment vulnerable.

We at North Point Insurance Group help landlords understand what Georgia landlord insurance basics actually cover. This guide walks you through the protection you need and how to find the right policy for your situation.

What Your Georgia Landlord Policy Actually Covers

Georgia landlord insurance protects three critical areas that standard homeowners policies ignore: your building, your liability exposure, and your rental income. Dwelling coverage pays for repairs to the structure after fire, wind, hail, vandalism, or other covered perils. Since Georgia has experienced 134 major weather disasters since 1980, this protection matters. If a tenant causes damage beyond normal wear and tear, vandalism coverage typically reimburses you up to limits like $100,000, depending on your policy form. Other structures coverage extends protection to detached garages, sheds, and fences at rates up to 100% of your dwelling limit.

Liability protection is where landlord policies diverge sharply from homeowners coverage. If a tenant or visitor is injured on your property and sues you, landlord liability coverage pays medical bills, legal costs, and settlements up to your policy limit-typically $1,000,000 on standard policies. Tenant injury lawsuits frequently exceed six figures and can threaten your personal assets without proper coverage.

Why Loss of Rent Coverage Prevents Financial Collapse

Fair Rental Value coverage reimburses you for lost rental income when a covered event makes the property uninhabitable. If your rental earns $2,000 monthly and a fire forces tenants out for three months of repairs, this coverage replaces approximately $6,000 in lost rent while you handle repairs and mortgage payments continue. Without this protection, you absorb those costs entirely, which strains most landlords’ cash flow.

Some enhanced policies go further by covering ongoing expenses like property taxes, utilities, and mortgage payments during vacancy, not just forgone rent. Eviction and legal fee reimbursement coverage, available on many Georgia policies, covers court costs when you must legally remove a tenant-addressing a gap that standard homeowners policies leave wide open.

Additional Coverages That Protect Against Real Risks

Water backup coverage protects you from sewer backups and heavy rain damage, a practical addition given Georgia’s climate patterns. Vacancy coverage maintains your protection if the property sits empty for 30 to 60 days or longer between tenants, preventing coverage lapses during turnover periods. Building code coverage pays for code-compliant upgrades required after a covered loss, which matters for older Georgia properties facing modern compliance expenses.

Flood insurance requires a separate policy through the National Flood Insurance Program or private carriers because standard landlord policies exclude all flood damage. High-risk coastal areas like St. Simons Island face landlord premiums around $4,206 annually versus homeowners rates near $3,365, reflecting significant flood exposure that demands separate flood protection.

Understanding what your policy covers sets the foundation for selecting the right protection level. The next step involves recognizing why standard homeowners insurance falls short and what specific gaps landlord policies fill.

Why Standard Homeowners Insurance Won’t Protect Your Rental

Homeowners Policies Explicitly Exclude Rental Properties

Your homeowners policy explicitly excludes rental properties, and insurers enforce this restriction aggressively. If you file a claim on a property you rent out and the insurer discovers tenants live there, they can deny the claim entirely and cancel your policy. Homeowners policies are priced and underwritten for owner-occupied homes only, where the policyholder lives on-site and maintains the property personally. The moment tenants move in, the risk profile changes fundamentally. Tenants have less financial incentive to prevent damage, wear and tear accelerates, and liability exposure multiplies. Insurers know this, which is why they simply refuse to cover rental properties under standard homeowners forms. Georgia landlords who attempt to use homeowners insurance for rental properties discover this gap only when they need the coverage most-after a loss occurs and the claim gets denied.

Liability Coverage Falls Short for Tenant-Related Claims

Liability protection in homeowners policies covers injuries that happen on your property when you’re negligent, but the coverage is minimal and excludes tenant-related claims entirely. If a tenant’s guest slips on your stairs and sues, a homeowners policy won’t cover it because the injury occurred at a rental property. Homeowners liability typically maxes out around $300,000 to $500,000, far below what a serious injury lawsuit demands. Tenant injury cases regularly exceed $1,000,000 in damages, and without landlord liability coverage, your personal assets become the target. Georgia has experienced 134 major weather disasters since 1980, meaning property damage claims are common. When a fire damages your rental and tenants lose their belongings and income, they often sue the landlord. Your homeowners policy won’t defend you in these situations.

Lost Rental Income Creates Unmanageable Financial Gaps

Lost rental income represents another massive gap that homeowners policies ignore completely. Homeowners policies never reimburse you for rent you fail to collect, whether because the property is uninhabitable after a covered loss or because you must evict a tenant who stops paying. A three-month repair period on a property earning $2,000 monthly costs you $6,000 in lost income that your homeowners policy ignores. Without landlord insurance, you absorb those costs entirely while your mortgage payments and property taxes continue. These gaps aren’t minor oversights-they expose you to financial ruin on the exact risks landlords face most often.

Understanding these exclusions reveals why landlord insurance exists as a separate product category. The right policy addresses each of these gaps directly, and selecting that coverage requires assessing your specific property and risk profile.

How to Choose Your Georgia Landlord Insurance Policy

Start with three specific pieces of information about your rental property: its replacement cost (not market value), the monthly rent you collect, and any outstanding mortgage balance. Replacement cost matters because Georgia construction costs have risen significantly, and underinsuring by even 20% triggers coinsurance penalties that reduce your payout substantially. Contact a local contractor or use online estimators to establish a realistic rebuild figure. Next, identify your property’s risk factors. Properties in high-crime Atlanta areas qualify for burglar alarm and security camera discounts that can reduce premiums by 5-15%. Coastal rentals like those on St. Simons Island face premiums around $4,206 annually for landlord coverage versus $3,365 for homeowners policies due to hurricane and flood exposure, so flood risk assessment is non-negotiable.

Properties with reinforced roofs, storm shutters, or sump pumps qualify for additional discounts that can lower your annual cost by several hundred dollars. Older homes may need building code coverage to handle compliance upgrades after a loss, adding modest cost but preventing expensive surprises. Properties sitting vacant for extended periods between tenants require explicit vacancy coverage or a separate vacant property policy that costs roughly 120% more than standard landlord coverage.

Comparing Policy Forms and Coverage Levels

Georgia landlords choose between three main policy tiers. DP-1 covers basic perils like fire, lightning, wind, and hail but excludes theft and vandalism, making it unsuitable for most rental situations. DP-2 adds vandalism, burglary, frozen pipes, and electrical damage while including fair rental value coverage, running approximately $1,280 annually across Georgia on average. DP-3 provides comprehensive protection with higher liability limits and broader add-ons, costing more but covering nearly all risks except flood and earthquake.

Your choice depends entirely on your tenant profile and property condition. Properties with strong tenant screening-checking credit history and eviction records-support lower premiums because insurers view screened tenants as lower risk. Increasing your deductible from $500 to $1,000 cuts premiums roughly 10-15%, but only if you maintain emergency funds to cover that deductible when claims occur.

Bundling and Comparing Quotes

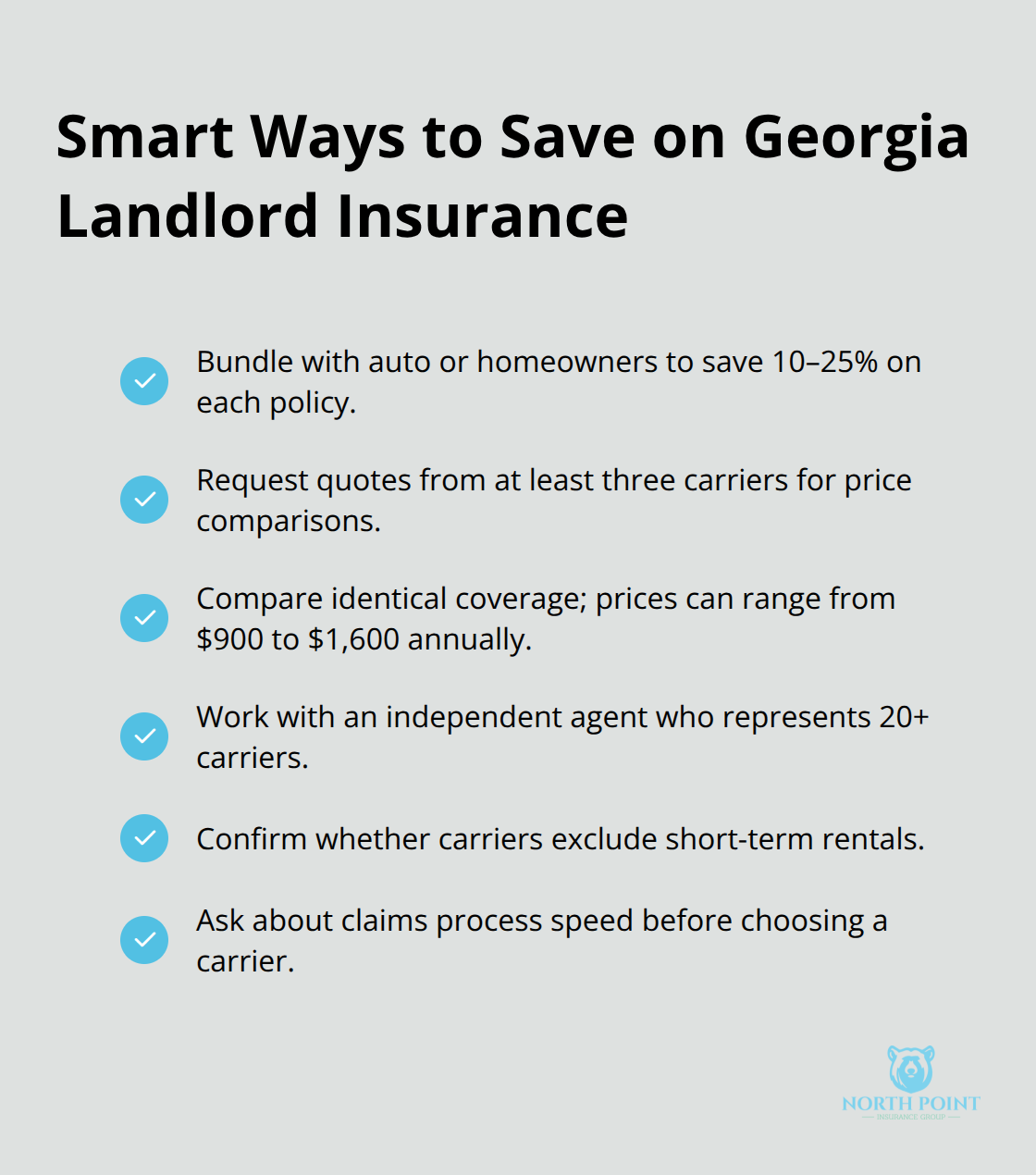

Bundling landlord insurance with your auto or homeowners policy typically saves 10-25% on each policy, making it worth asking about during quotes. Quotes from at least three carriers reveal significant price variations; identical coverage can range from $900 to $1,600 annually depending on the insurer’s appetite for rental properties.

An independent agent who represents 20+ carriers beats calling individual insurers because they know which companies offer the best rates for Georgia’s specific risks and which ones exclude short-term rentals or have slow claims processes.

Working with an Independent Agent

GEICO, State Farm, Obie, and Allstate all serve Georgia landlords, but each has different strengths. GEICO offers 97% customer satisfaction and bundling discounts but can be challenging for claims filing. State Farm provides customizable coverage but may cost more for certain property types. Obie processes quotes quickly online but limits phone support to weekdays. An independent agent navigates these tradeoffs for you and handles policy comparisons without charging you directly.

Ask your agent specifically about non-occupied dwelling coverage if you plan extended vacancy, rent guarantee insurance to protect against tenant non-payment, and whether your policy covers loss of rental income during disputes or evictions. Require all quotes in writing with coverage limits, deductibles, and exclusions clearly stated so you compare actual protection, not just price. Annual policy reviews with your agent matter because replacement costs climb yearly in Georgia, and underinsurance becomes more likely without adjustment.

Final Thoughts

Georgia landlord insurance basics protect your rental investment against three financial threats that standard homeowners policies ignore: property damage, liability exposure, and lost rental income. A single fire, tenant injury lawsuit, or extended vacancy can drain your cash reserves and threaten your personal assets without proper coverage. The right policy covers your building structure, tenant-related liability claims that exceed six figures, and the rent you lose when repairs force tenants out.

Selecting the right coverage starts with knowing your property’s replacement cost, monthly rental income, and specific risk factors. Georgia’s 134 major weather disasters since 1980 make dwelling protection non-negotiable, while coastal properties face hurricane and flood exposure that demands separate flood insurance. Properties in high-crime areas qualify for security discounts, and reinforced roofs or storm shutters lower your annual premium by several hundred dollars. Your tenant screening quality matters too-landlords who check credit history and eviction records often qualify for better rates because insurers view screened tenants as lower risk.

DP-2 policies averaging around $1,280 annually across Georgia provide solid protection for most landlords, while DP-3 offers comprehensive coverage for higher-value properties. Bundling with auto or homeowners insurance typically saves 10-25%, and comparing quotes from at least three carriers reveals significant price variations on identical coverage. We at North Point Insurance Group help Georgia landlords navigate these decisions with personalized guidance from local agents who understand your property’s unique risks, and our independent agency shops multiple carriers to find coverage that matches your needs and budget.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.