Georgia Umbrella Policy Details: What You Should Know

Your homeowner’s or auto insurance might not be enough if someone sues you for a major accident. That’s where Georgia umbrella policy details come in-they provide extra liability protection when your primary policies hit their limits.

At North Point Insurance Group, we help Georgia residents understand how umbrella coverage works and whether it fits their situation. This guide breaks down what you need to know to protect your assets.

How Umbrella Insurance Fills the Gaps in Your Coverage

What Umbrella Coverage Actually Does

An umbrella policy provides extra liability protection that sits on top of your auto, homeowners, or renters insurance. When someone sues you and the judgment exceeds what your primary policy covers, your umbrella kicks in to pay the difference. This matters because standard homeowners liability maxes out around $500,000, and auto liability often stops at $500,000 per accident. A serious injury claim can easily surpass these limits. In Georgia, umbrella policies typically start at $1 million in coverage, with options to go higher depending on your assets and risk exposure.

Forbes data via ACE Private Risk Services shows the average cost for a $1 million umbrella is about $383 annually for a standard household, making it surprisingly affordable protection.

What Your Umbrella Covers and What It Doesn’t

The policy covers bodily injury claims, property damage liability, legal defense costs, and even defamation or slander lawsuits that exceed your primary limits. What it does not cover matters just as much: your own injuries, damage to your own property, most business-related claims, contract disputes, or intentional harm. This distinction prevents you from thinking you’re protected when you’re actually not.

How the Layering Structure Works

Your primary auto or homeowners policy pays first up to its limit, then the umbrella covers everything above that threshold. For example, if your homeowners liability limit is $500,000 and a claim totals $650,000, you pay the first $500,000 from your homeowners policy, and the umbrella covers the remaining $150,000. This structure means you need adequate underlying coverage to qualify for an umbrella in Georgia. Some policies require a self-insured retention, which functions as a deductible when no other coverage applies.

Coverage Scope and Premium Factors

Most Georgia umbrella policies provide worldwide coverage, meaning protection extends beyond the United States if you’re sued abroad. The premium increases with higher limits: Money.com reports roughly $75 more for each additional $1 million of coverage beyond the base $1 million. Your specific cost depends on location, number of homes and vehicles, desired limit, and your accident and credit history. These variables mean two Georgia households can pay very different premiums for the same coverage amount.

Finding the Right Balance for Your Situation

Shopping multiple carriers helps you find the right balance between protection and cost. An independent agent can review your current policy limits, assess your assets, and match you with carriers that fit your needs and budget. The right umbrella coverage protects your financial future without overextending your premiums.

Who Should Buy Umbrella Coverage in Georgia

Umbrella insurance isn’t just for the wealthy, though high-net-worth individuals absolutely need it. If you have any assets worth protecting-a home, retirement accounts, investment property, or steady income-a liability lawsuit can threaten your financial security. One serious accident can result in a judgment far exceeding your primary policy limits. A homeowner whose guest drowns in the pool, a driver who causes a multi-vehicle crash with severe injuries, or a landlord sued by a tenant faces six or seven-figure claims. Standard homeowners liability caps around $500,000 and auto liability often stops at $500,000 per accident, which means even middle-income earners need umbrella protection. You cannot wait until a lawsuit happens to buy this coverage-you cannot retroactively protect yourself once someone files a claim. The time to act is now, before an incident occurs.

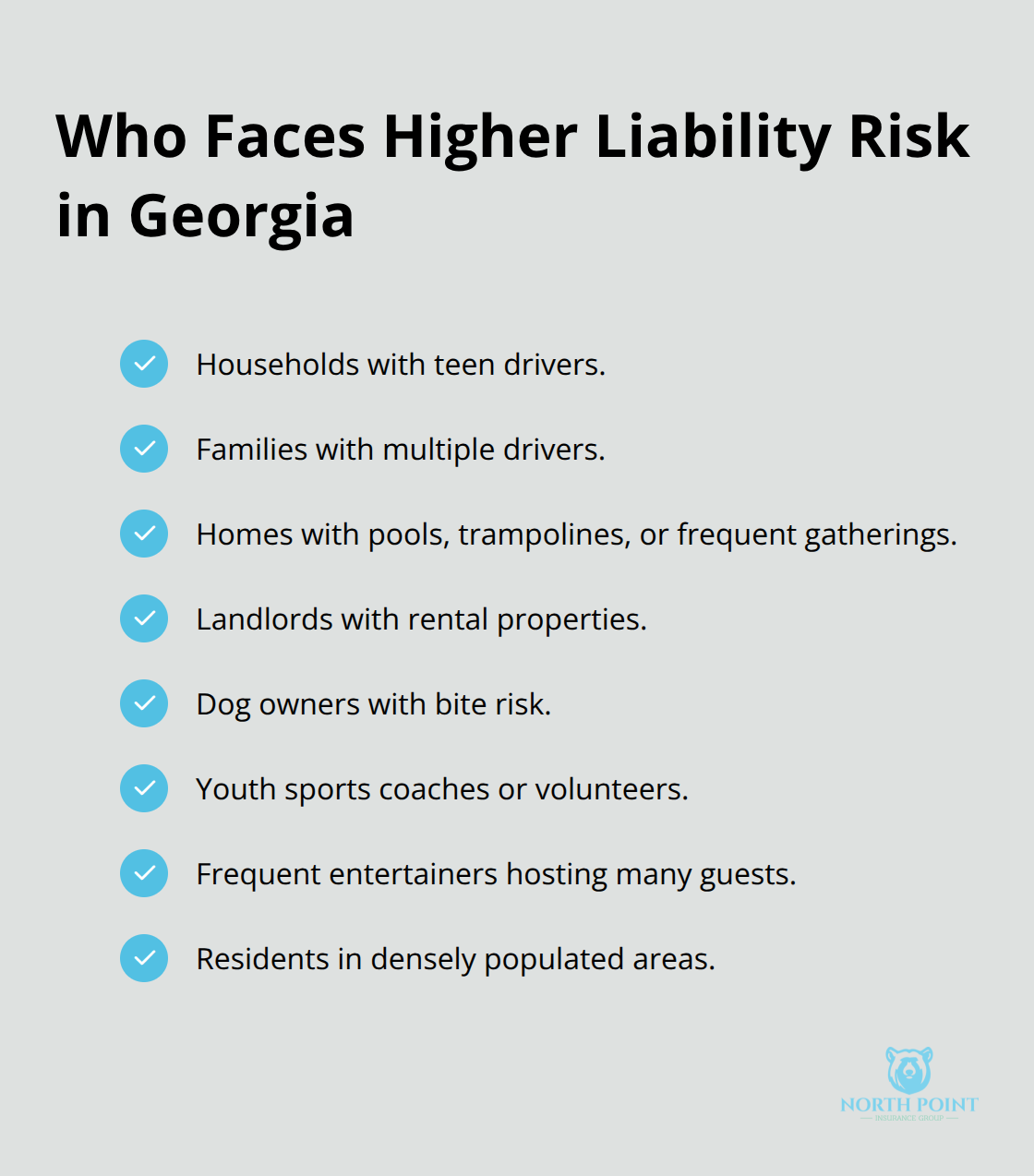

Who Faces the Highest Liability Risk

Parents with teenagers driving the family car should strongly consider umbrella coverage, especially if they have multiple drivers in the household. Young drivers cause more accidents than other age groups, and insurance companies charge higher premiums to reflect that risk. Homeowners who host gatherings, have pools, or own trampolines face significant exposure because guests can suffer injuries on your property and hold you liable. Landlords with rental properties need umbrella protection since tenants can sue for injuries, property damage, or alleged negligence. Pet owners whose dogs bite someone or cause injury also face real liability exposure.

High-risk scenarios like coaching youth sports, frequently entertaining guests, or living in a densely populated area increase the likelihood of being sued. If any of these situations apply to you, an umbrella policy isn’t optional-it’s essential asset protection.

Calculating the Right Coverage Amount

The amount of umbrella coverage you need depends on your total taxable assets and income potential. Someone with a $500,000 home, $200,000 in retirement savings, and a stable income should carry at least $1 million in umbrella coverage. If you have multiple properties, significant investments, or high earning potential, $2 million becomes more appropriate. High-net-worth individuals with multiple homes, investment portfolios, or substantial liquid assets should consider $5 million or higher. Georgia umbrella policies typically start at $1 million, with options extending to much higher limits depending on your situation. The cost difference between $1 million and $2 million coverage is modest, making it affordable to increase protection as your assets grow.

How Your Agent Helps You Find the Right Fit

An independent agent can review your specific situation, calculate your total assets at risk, and recommend the right coverage level without overprotecting or underprotecting your finances. This personalized approach matters because two Georgia households with similar assets may face different liability exposures based on their lifestyle, property features, and family composition. Your agent shops multiple carriers to find competitive rates and coverage options that align with your needs. The next step involves understanding what costs you’ll actually pay and which coverage limits Georgia insurers offer.

What Georgia Umbrella Policies Actually Cost

A $1 million umbrella policy costs around $383 annually for a standard household with one home and two vehicles, according to Forbes data via ACE Private Risk Services. This price point surprises most people-umbrella protection costs far less than expected, so cost should not prevent you from buying coverage. If you want $2 million in coverage instead, you’ll pay roughly $75 more per year, making doubled protection quite affordable. Your exact premium depends on several real factors: your location within Georgia, the number of homes and vehicles you own, your desired coverage limit, and your accident and credit history. Two Georgia households with identical coverage amounts will pay significantly different premiums because insurers weight these variables differently.

When you request quotes, you’ll see this variation immediately-one carrier might charge $280 annually while another charges $420 for the same $1 million limit. This is why shopping multiple carriers matters. Mercury Insurance offers umbrella coverage in Georgia as little as $1 per day for a $1 million policy, though actual rates depend on your specific situation including the number of insured assets, teen drivers, and liability history. The key insight is that umbrella insurance remains affordable even when you increase coverage limits, so price alone should not determine how much protection you buy.

How Premium Factors Affect Your Rate

Location within Georgia influences your premium because some areas face higher litigation risk or more frequent claims. The number of homes and vehicles you own directly impacts your rate since each property represents potential liability exposure. Your accident history matters significantly-carriers charge higher premiums to drivers with prior claims or violations. Credit history also plays a role, as insurers view credit scores as predictors of claim likelihood. These variables combine to create your personalized rate, which is why two identical $1 million policies can cost different amounts annually. Shopping quotes from multiple carriers reveals these differences and helps you find the best value for your situation.

Coverage Limits That Match Your Georgia Assets

Georgia insurers typically offer umbrella policies starting at $1 million, with the ability to increase coverage as your assets grow. Some carriers like Travelers provide limits up to $10 million, while others like Chubb serve high-net-worth clients with coverage extending to $100 million through their Masterpiece Excess Liability Insurance product. For most Georgia residents, $1 million covers basic protection adequately. If you own multiple properties, have substantial investment accounts, or earn a high income, $2 million to $5 million becomes more appropriate. The decision should reflect your total taxable assets plus your future earning potential-not just what you own today.

Policy Customization and Special Coverage Options

Most Georgia umbrella policies include a self-insured retention, which functions as a deductible when no underlying coverage applies, though this rarely affects typical claims since your auto and homeowners policies usually trigger first. Customization options vary by carrier, so your agent can tailor the policy to your specific risk profile. Some policies include worldwide coverage as standard, extending protection if you’re sued abroad. Others offer specialized add-ons like libel and slander coverage for additional premiums. The coverage you select should reflect your actual lifestyle and assets, not generic recommendations.

Final Thoughts

Georgia umbrella policy details matter because they determine whether your assets stay protected when a serious lawsuit hits. Standard homeowners and auto policies leave you exposed once claims exceed their limits, typically around $500,000 each. An umbrella policy fills that gap affordably, starting at roughly $383 annually for $1 million in coverage, so cost should never prevent you from buying this protection.

Most Georgia residents benefit from at least $1 million in protection, though those with multiple properties or significant assets should consider $2 million or higher. The cost difference between coverage levels remains modest-increasing your limit from $1 million to $2 million adds only about $75 per year. Shopping multiple carriers reveals significant price variations for identical coverage, which is why working with an agency that accesses numerous insurers matters.

Contact North Point Insurance Group to schedule a coverage review and receive quotes from carriers that fit your needs and budget. Our local agents in Alpharetta understand Georgia’s specific liability landscape and help you navigate umbrella coverage options without the impersonal call-center experience. We shop multiple carriers to find tailored coverage that protects your financial future at competitive pricing.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.