Homeowners Deductible Guide: Understanding Your Policy

Your homeowners deductible is one of the most misunderstood parts of your insurance policy. Many homeowners pick a deductible amount without understanding how it affects both their monthly premiums and their wallet when they file a claim.

At North Point Insurance Group, we’ve created this homeowners deductible guide to help you make an informed decision. The right deductible can save you thousands of dollars over time, but only if you choose it strategically.

What Your Deductible Actually Means

Your homeowners deductible is the amount you pay out of your own pocket before your insurance company covers the rest of a claim. If you have a $1,000 deductible and file a claim for $6,500 in roof damage, you pay $1,000 and the insurer pays $4,500. This applies per claim, which matters if you experience multiple losses in the same policy year-you’ll owe the deductible for each one. The Insurance Information Institute reports that most homeowners deductibles range from $500 to $2,500, with many insurers setting minimums at $500 or $1,000. Some homeowners opt for higher deductibles up to $5,000, particularly those with more valuable homes or strong emergency savings. One important point: deductibles only apply to property damage claims. If someone is injured on your property and files a liability claim against you, or if you need to cover their medical expenses, you don’t pay a deductible. Your liability coverage and medical payments coverage operate without deductible requirements.

How Your Deductible Connects to Your Premium

The relationship between deductible and premium is direct and significant. Raising your deductible from $500 to $1,000 can lower your annual premium substantially-in some cases by $1,300 or more, based on 2022 insurance data. Moving to a $2,000 deductible typically saves even more. This trade-off exists because higher deductibles mean you share more of the risk with yourself rather than transferring it all to the insurer. The math is straightforward: insurers charge lower premiums when they know they’ll pay less on average. However, this savings only benefits you if you can actually afford to pay the deductible when a loss occurs. Choosing a $2,500 deductible to save $100 per year makes no sense if you’d struggle to find that $2,500 if your roof gets damaged by hail. The key is aligning your deductible with your actual financial capacity, not just chasing the lowest premium.

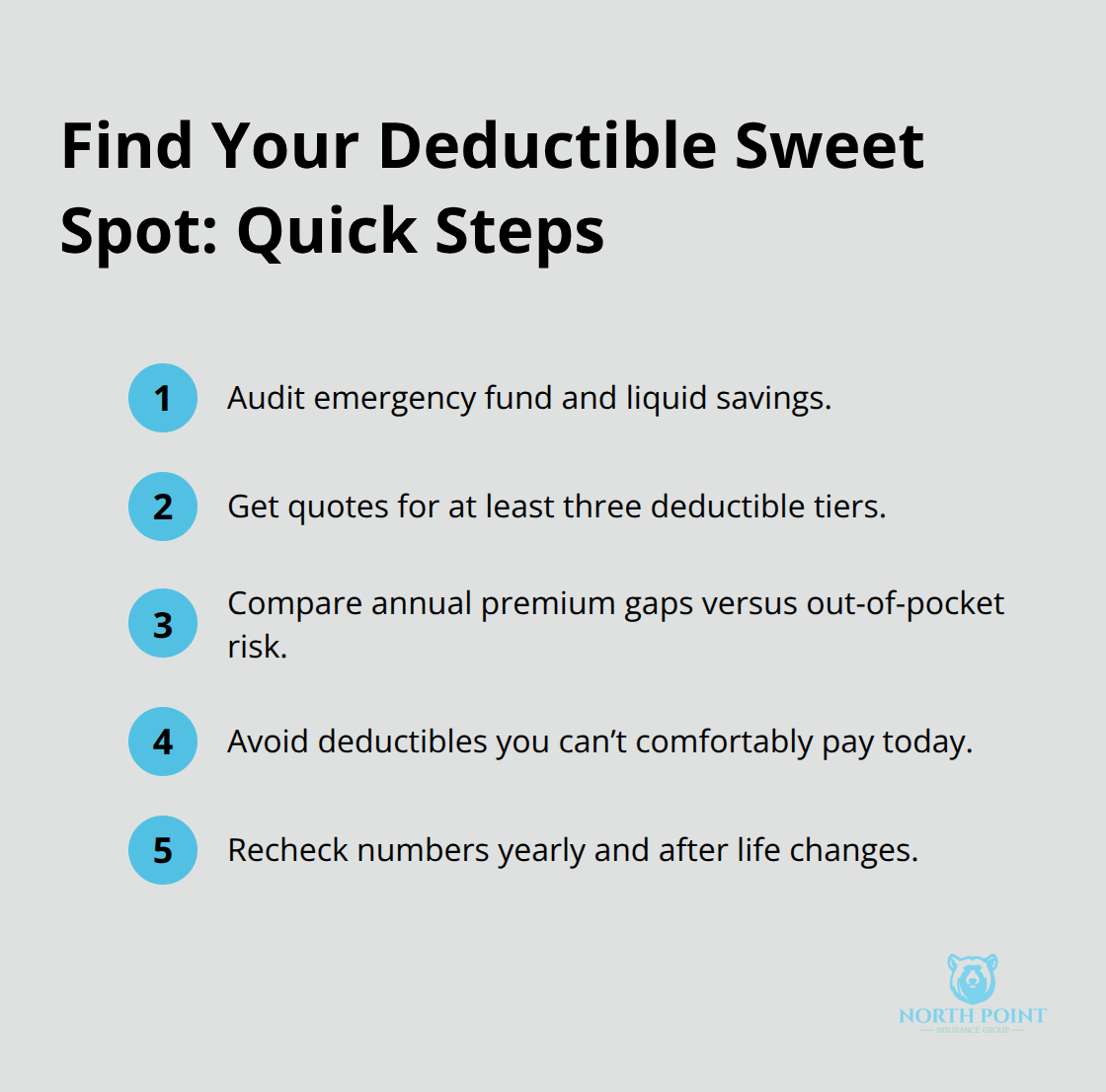

Finding Your Financial Sweet Spot

You need to assess what you can realistically afford to pay out of pocket. Start by looking at your emergency fund and liquid savings. If you have three to six months of expenses saved, you can comfortably handle a higher deductible. If your savings are thin, a lower deductible protects you from financial strain when a claim happens. Calculate the premium difference between deductible options-sometimes the savings between a $500 and $1,000 deductible are modest, making the lower option more sensible. Other times, the gap widens significantly at higher deductible levels, which may justify the increased out-of-pocket risk if your finances allow it. The worst position to be in is selecting a deductible you cannot pay, then facing a claim and having no way to cover your share of the loss.

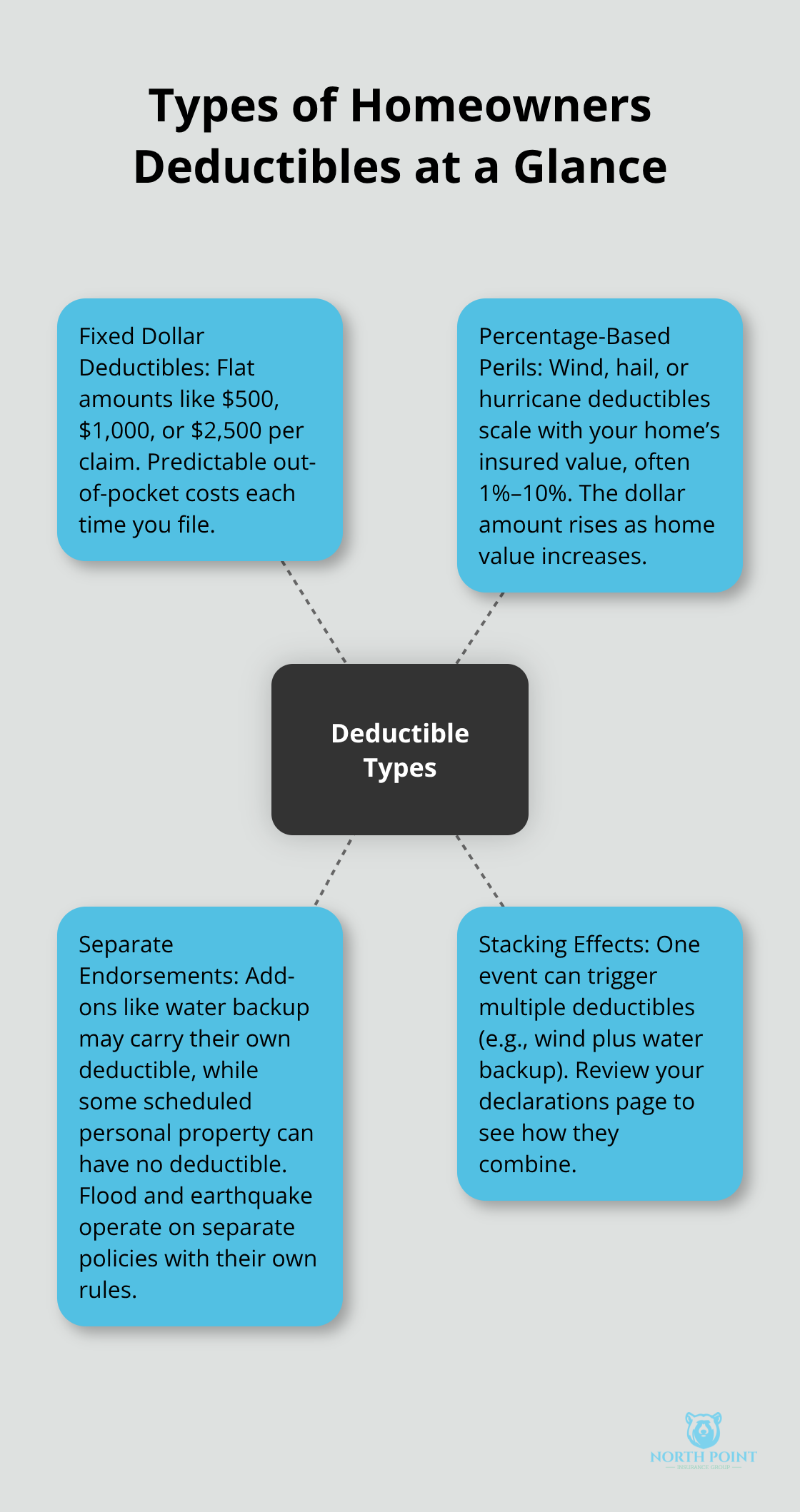

Types of Homeowners Deductibles

Fixed Dollar Deductibles

Homeowners insurance offers different deductible structures, and understanding which one applies to your claim matters when you file. The most common approach is a fixed dollar deductible-a set amount like $500, $1,000, or $2,500 that stays the same regardless of your home’s value or the size of your loss. This flat amount is straightforward: you pay it once per claim, and the insurer covers the rest. You know exactly what you’ll owe when a claim happens.

Percentage-Based Deductibles for Specific Perils

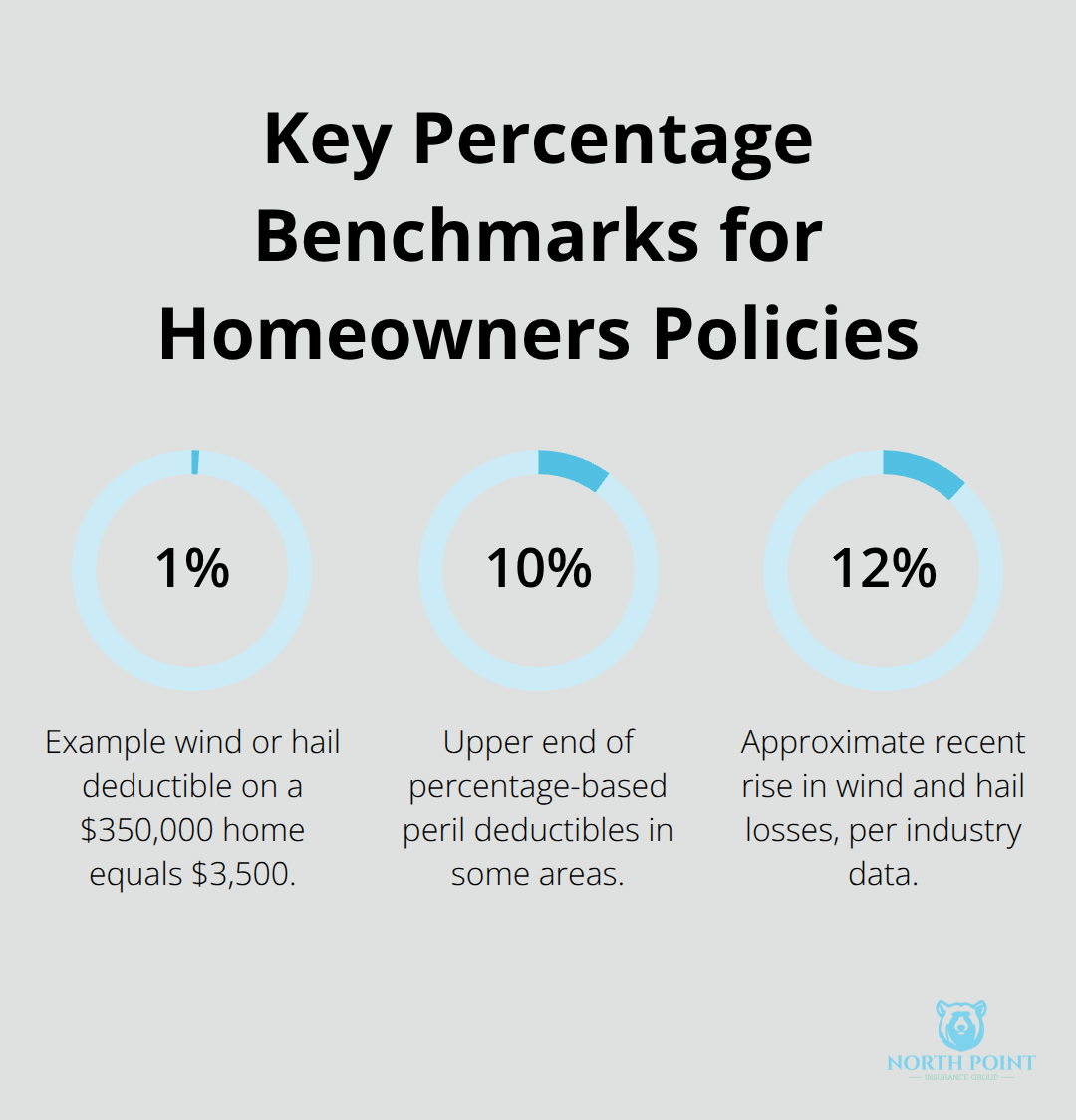

Percentage-based deductibles exist for specific perils, particularly wind, hail, and hurricane damage. These deductibles are calculated as a percentage of your home’s insured value-often 1% to 10% depending on your location and the peril. If your home is insured for $350,000 and you have a 1% wind or hail deductible, that means a $3,500 deductible applies to those specific claims. In high-risk areas like Florida or Tornado Alley, percentage deductibles are increasingly common because they scale with home value.

This trend matters because wind and hail are the most frequent homeowner claim causes.

Separate Deductibles for Endorsements and Add-Ons

You might also encounter separate deductibles for different coverage areas. A water backup endorsement carries its own deductible equal to or higher than your main deductible. Scheduled personal property coverage for jewelry or fine art typically has no deductible, but adding sump pump failure protection might include a $1,000 separate deductible. Earthquake and flood insurance operate entirely outside your standard homeowners policy with their own deductible rules-flood deductibles typically range from $1,000 to $10,000, while earthquake deductibles are usually 5% to 25% of replacement value.

How Multiple Deductibles Stack in a Single Claim

A single claim can trigger multiple deductibles. A hail storm that damages your roof and causes water backup means you’ll owe both your standard deductible and your water backup deductible. Understanding your specific policy’s deductible structure prevents nasty surprises when you need to file.

Check your declarations page carefully to see whether you have fixed deductibles, percentage deductibles, or a combination of both. Once you understand what type of deductible structure your policy carries, the next step is selecting the right deductible amount for your financial situation.

How Much Should Your Deductible Actually Be

Match Your Deductible to Your Emergency Fund

The right deductible isn’t about finding the lowest number or the highest savings. It’s about matching your deductible to what you can actually afford to pay when a loss happens. Start with your emergency fund. If you have three to six months of expenses saved, you have room to absorb a $2,000 or even $2,500 deductible. If your savings cover only one month of expenses, a $500 or $1,000 deductible protects you from financial crisis when your roof gets damaged by hail. This isn’t theory-it’s survival math. Data from 2022 shows that raising your deductible from $500 to $2,000 can save $1,300 or more annually, but that savings evaporates the moment you face a claim you cannot pay.

Calculate the Real Premium Gap Between Deductible Tiers

Next, calculate the actual premium gap between each deductible tier available to you. Sometimes moving from $500 to $1,000 saves only $50 or $75 per year-not worth the extra risk. Other times, the jump to $2,000 or $2,500 saves $300, $400, or more, which justifies the higher out-of-pocket exposure if your finances allow it. Get quotes with at least three different deductible options to see the real numbers for your home. Don’t assume the biggest deductible saves the most money proportionally. The worst financial decision is selecting a deductible based purely on the premium discount, then discovering you lack the cash to cover it when a claim arrives.

Account for Wind and Hail Deductibles in High-Risk Areas

Pay special attention to your wind and hail deductible if you live in Tornado Alley or other high-risk areas. Wind and hail cause the most frequent homeowner claims, with losses rising about 12 percent over recent years according to industry data. A 1 percent wind deductible on a $350,000 home equals $3,500, which stacks on top of your standard deductible if a hail storm damages your roof and causes water backup.

You could owe $5,000 or more in a single event. Many homeowners discover this stacking effect only after filing a claim. Review your declarations page right now to see whether you have a separate wind or hail deductible and calculate the total out-of-pocket cost if multiple coverages are triggered.

Avoid Common Deductible Selection Mistakes

Common mistakes happen when homeowners confuse their deductible with their coverage limit, forget that deductibles apply per claim (not per year), or fail to account for separate deductibles on endorsements like water backup or sump pump failure. Another frequent error is choosing a deductible that looked affordable six months ago but doesn’t match your current financial reality. Life changes-job loss, medical bills, market downturns-can make a $2,000 deductible suddenly unmanageable. Review your deductible choice annually, not just when you renew your policy. Your deductible should shift as your financial circumstances shift.

Final Thoughts

Your homeowners deductible is a financial decision that deserves real attention, not a quick checkbox on your policy form. The right deductible balances premium savings with your actual ability to pay when a loss occurs. Review your current policy declarations page today to confirm your deductible amounts, including any separate wind, hail, or water backup deductibles that might stack in a single claim.

Life circumstances change, and your deductible should change with them. A $2,000 deductible that made sense when you had strong savings might become risky after a job transition or unexpected expense. Check your deductible annually, not just at renewal time, and contact your agent to adjust your coverage before a claim forces the issue.

We at North Point Insurance Group understand that homeowners insurance isn’t one-size-fits-all, and our agents work with you to build a homeowners deductible guide tailored to your home and finances. We shop 20+ carriers to find coverage that matches your actual needs and budget, not just the lowest premium. Visit us at northpointig.com to speak with an agent who can review your specific situation and help you select the right deductible for your circumstances.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.