Georgia Auto Coverage Tips: Smart Shopping for Drivers

Georgia drivers face real pressure when shopping for auto insurance. Between state requirements, rate increases, and coverage options, it’s easy to make costly mistakes.

At North Point Insurance Group, we’ve helped countless drivers navigate these decisions. This guide breaks down Georgia auto coverage tips so you can shop smarter and protect yourself properly.

Georgia Auto Coverage: Understanding Requirements and Protecting Your Wallet

State Minimums Leave You Exposed

Georgia mandates a minimum of $25,000 in bodily injury coverage per person and $50,000 per incident, plus $25,000 in property damage coverage. These minimums exist to protect others if you cause an accident, but they’re dangerously low. The national average full-coverage premium sits around $2,578 annually, yet Georgia drivers often stop at these minimums to save money. That’s a mistake.

According to The Zebra, Georgia’s average full-coverage policy costs $2,909 annually, or about $243 monthly. Many drivers can upgrade to $50,000 per person and $100,000 per incident in bodily injury coverage for just slightly more, which provides substantially stronger financial protection if you’re at fault in a serious accident. The difference between minimum coverage and adequate coverage often costs less than you’d expect.

Collision and Comprehensive: Protection You Can’t Ignore

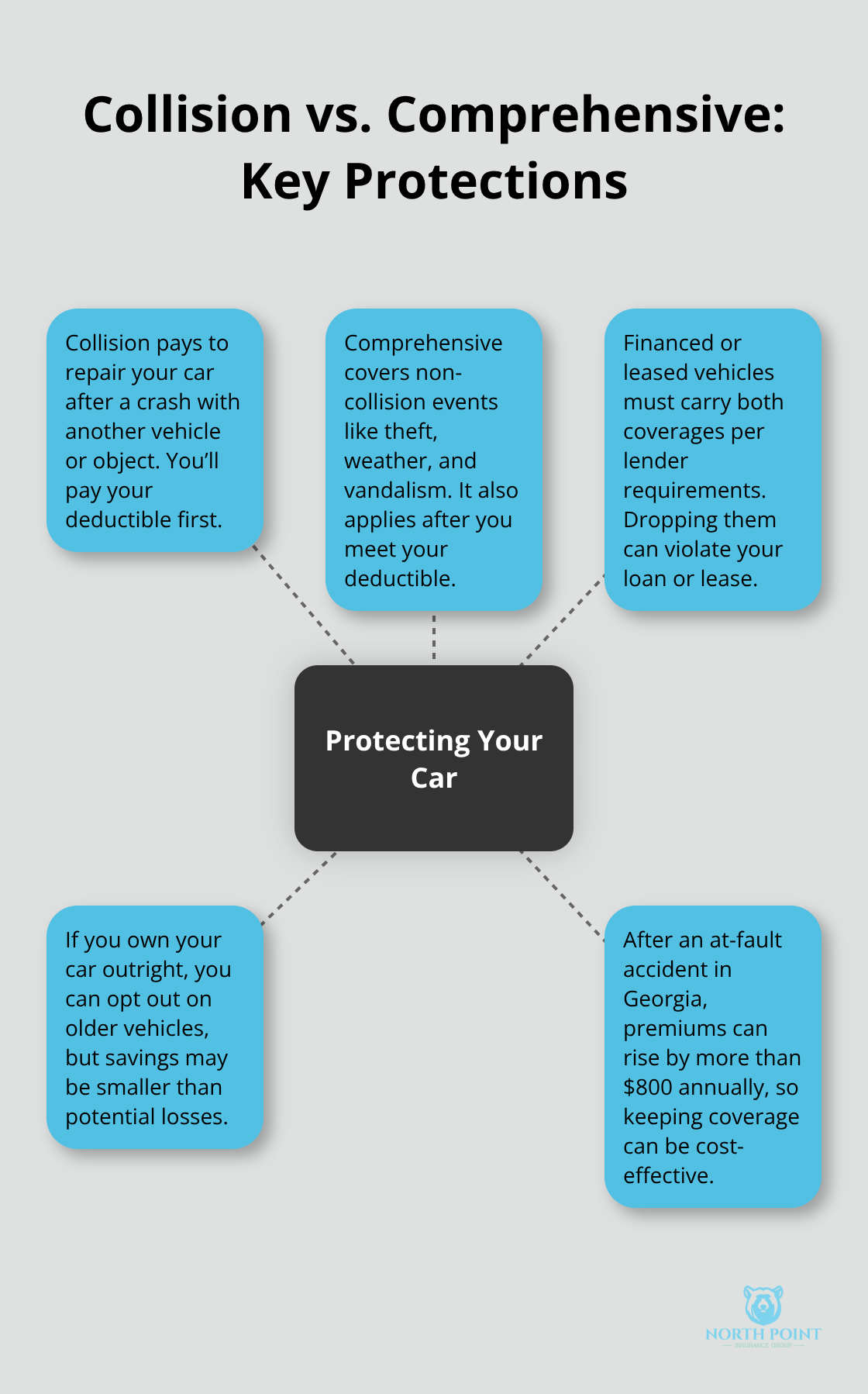

Georgia’s at-fault system means the driver responsible for an accident pays for damages. If you hit another vehicle or cause property damage, your liability coverage pays for their repairs. But what protects your own car? Collision covers damage from accidents with other vehicles or objects; comprehensive covers theft, weather, vandalism, and other non-collision events.

If you financed or leased your vehicle, your lender requires both. If you own your car outright, you have a choice, but dropping these coverages on an older vehicle sometimes costs more than keeping them. After an at-fault accident in Georgia, premiums can rise by more than $800 per year, making the protection you paid for in collision coverage far cheaper than the rate increase that follows a claim.

Uninsured motorist coverage also deserves serious attention. Roughly 20 percent of drivers in high-risk states lack insurance, and Georgia sits in that range. This coverage protects you if an uninsured driver hits you and can’t pay.

How Georgia’s Fault System Shapes Your Rates

Georgia operates under a traditional fault system, not no-fault insurance. Your driving record directly determines your rates. One at-fault accident triggers increases ranging from $897 with Georgia Farm Bureau to over $2,500 with GEICO, according to The Zebra. A DUI carries even steeper consequences-premiums jump by approximately 87 percent on average.

Your ZIP code also matters tremendously because urban areas like Atlanta carry higher rates due to congestion and accident density. These aren’t theoretical factors; they’re the mechanics that insurers use every day to price your policy. Understanding this system means you can anticipate how your choices today-like your driving habits or where you live-will affect tomorrow’s rates.

The Georgia Office of Commissioner of Insurance and Safety Fire can answer specific questions about how accidents or violations affect your coverage options. With these requirements and rate mechanics in mind, the next step involves comparing what different carriers actually charge for the coverage you need.

Finding the Right Coverage at the Right Price

Shop Multiple Carriers to Uncover Real Savings

Georgia drivers have no shortage of rate options, but most never compare them. According to The Zebra, about 49 percent of Georgia drivers feel they’re overpaying for auto insurance, yet the average driver saves roughly $1,245 per year. That’s money left on the table simply because people stick with their current insurer without checking alternatives.

Start by getting quotes from at least four different carriers using the same vehicle information, driving record, and coverage limits across each quote. State Farm ranks as the top overall value in Georgia according to The Zebra, balancing price with customer satisfaction, while Georgia Farm Bureau and Auto-Owners consistently deliver the cheapest liability-only options at around $50 monthly. For full coverage, Georgia Farm Bureau averages $122 monthly, Auto-Owners $142 monthly, and USAA $172 monthly. These aren’t theoretical differences-they’re real money you’ll pay or save based on which carrier you choose.

Don’t switch insurers every six months chasing lower rates. Frequent switching raises underwriting costs and can actually work against you; instead, shop every one to two years or after major life changes like moving, marriage, or a new vehicle.

Deductibles and Coverage Limits Shape Your Protection and Cost

Your deductible choice directly impacts both your monthly premium and your out-of-pocket risk. The standard $500 deductible appears on most policies, but raising it to $1,000 can lower your premium noticeably, while dropping to $250 increases costs substantially. The math works best if you have emergency savings to cover a higher deductible without financial stress.

On coverage limits, Georgia’s $25,000 per person bodily injury minimum is inadequate for most situations; upgrading to $50,000 per person and $100,000 per incident typically costs only $20 to $40 more monthly but provides far superior protection. This modest increase shields you from catastrophic financial exposure if you cause a serious accident.

Discounts Cut Costs Without Sacrificing Protection

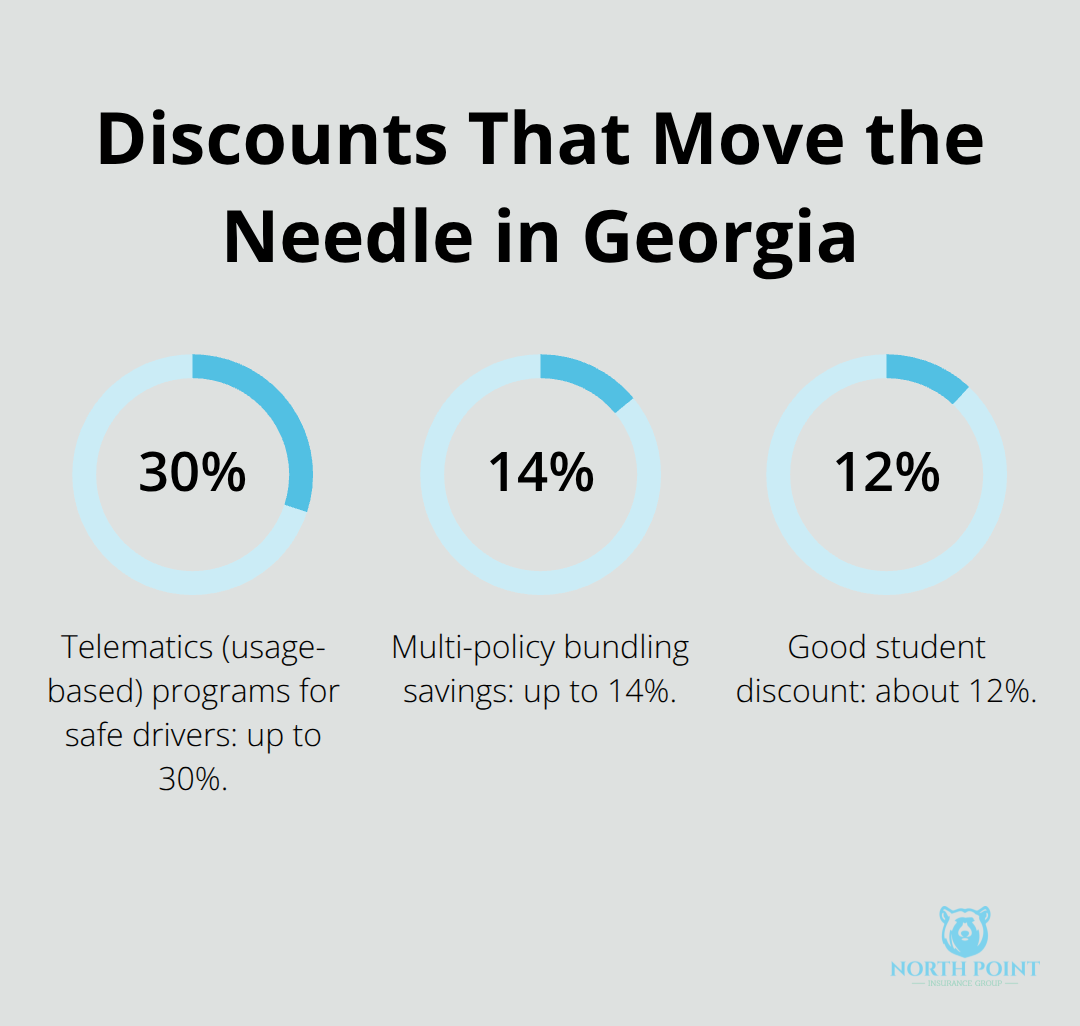

Discounts represent your biggest opportunity to reduce costs without sacrificing coverage. Multi-policy bundling saves up to 14 percent, telematics programs (usage-based insurance) can yield up to 30 percent for safe drivers, good student discounts run about 12 percent, and defensive driving courses shave off another 5 percent. Anti-theft devices, multi-vehicle policies, and paperless billing each trim additional percentages from your premium.

After an at-fault accident in Georgia, expect your rate to jump $800 or more annually depending on your carrier, making these discounts even more valuable as ways to offset future increases before they happen. The carriers you choose and the discounts you stack determine whether you pay $122 monthly or substantially more for the same protection.

Mistakes That Cost Georgia Drivers Real Money

Minimum Coverage Creates Maximum Financial Risk

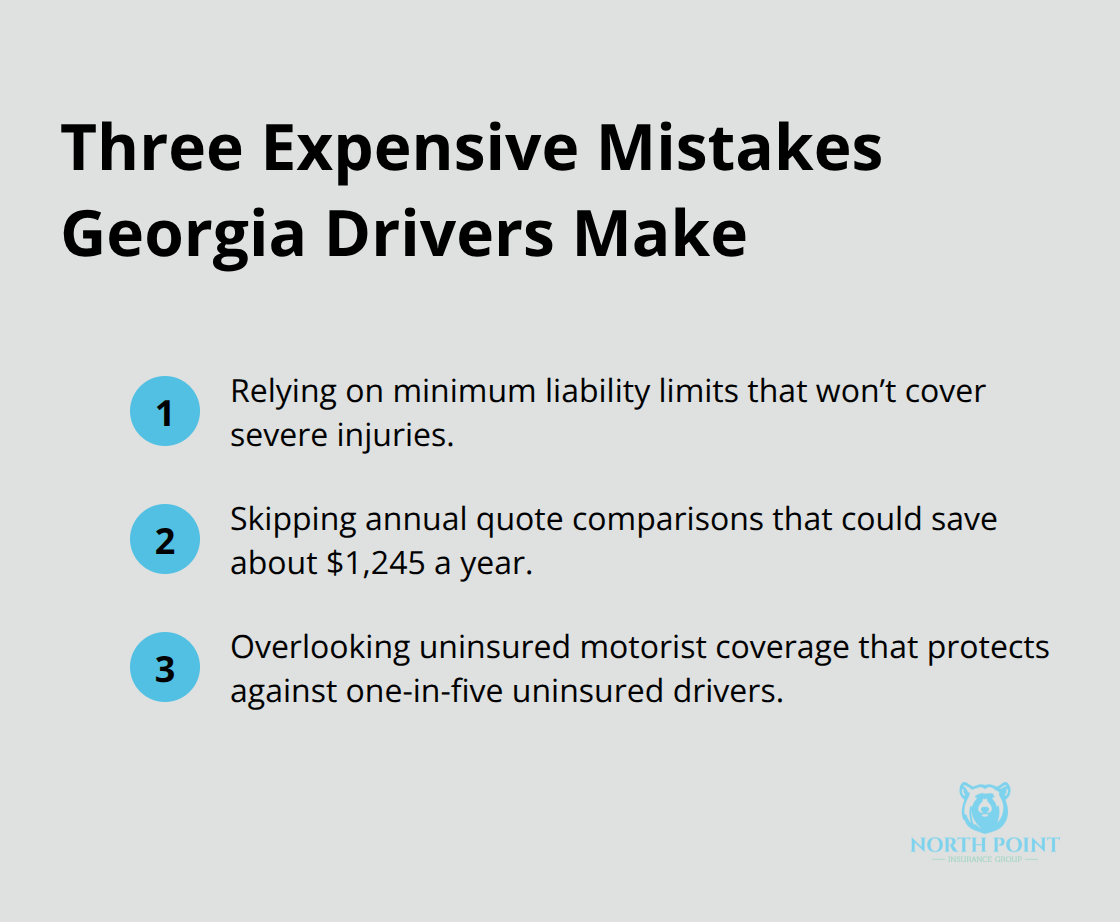

Most Georgia drivers treat auto insurance as a checkbox rather than a financial decision. Georgia’s minimum coverage limits exist for legal reasons, not financial protection. Georgia’s minimum coverage limits of $25,000 per person bodily injury sound adequate until you cause an accident involving serious injuries. Medical costs for a severe injury easily exceed $100,000, leaving you personally liable for the difference.

The Zebra data shows that upgrading from minimum to $50,000 per person and $100,000 per incident costs only $20 to $40 monthly-roughly $240 to $480 annually. A single accident with minimum coverage can cost you tens of thousands out of pocket, making that small upgrade one of the smartest decisions you’ll make. Yet most Georgia drivers never do it. They justify the choice by saying they drive safely, but accidents happen to careful drivers too, and Georgia’s at-fault system means your liability coverage is what protects your assets when they do.

Skipping Annual Rate Reviews Costs Thousands

The second major mistake is treating your auto insurance policy as a set-it-and-forget-it purchase. Georgia drivers who don’t shop annually leave massive savings on the table. According to The Zebra, drivers who compare quotes across carriers save approximately $1,245 per year on average. That’s not a theoretical number-it’s real money.

State Farm ranks as the top overall value in Georgia, but Georgia Farm Bureau costs significantly less for full coverage at around $122 monthly compared to State Farm’s higher premiums. USAA and Auto-Owners also deliver competitive rates for specific driver profiles. The carriers you choose matter enormously, yet most drivers stick with their current insurer without checking alternatives. Shopping every one to two years takes maybe an hour and produces savings that compound year after year.

Overlooking Uninsured Motorist Coverage Leaves You Exposed

Uninsured motorist coverage gets overlooked constantly, despite being essential protection in Georgia where roughly one in five drivers lacks insurance. This coverage costs minimal amounts-often $10 to $20 monthly-but protects you completely if an uninsured driver causes an accident. The combination of staying with an overpriced carrier, carrying inadequate liability limits, and skipping uninsured motorist coverage creates a perfect storm of unnecessary risk and wasted money.

Final Thoughts

Smart Georgia auto coverage tips require three concrete actions: upgrade beyond minimums, shop annually, and add uninsured motorist protection. Georgia’s $25,000 bodily injury minimum leaves you financially exposed for tens of thousands in liability if you cause a serious accident, yet raising limits to $50,000 per person and $100,000 per incident costs only $20 to $40 monthly. Your liability coverage protects your assets when accidents happen, and Georgia’s at-fault system means they will happen to someone.

Shopping every one to two years saves drivers approximately $1,245 annually on average. State Farm, Georgia Farm Bureau, Auto-Owners, and USAA each deliver competitive rates for different driver profiles, but you won’t know which works best for your situation without comparing quotes from at least four carriers. Getting those quotes takes an hour and produces savings that far exceed the time invested.

Uninsured motorist coverage costs minimal amounts yet protects you completely against the roughly one in five Georgia drivers who lack insurance. We at North Point Insurance Group understand that Georgia drivers need clear guidance, not sales pressure, and our local agents shop 20+ carriers to find coverage that matches your actual needs and budget. Contact us to discuss your Georgia auto coverage needs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.