Boat Policy Options Georgia: What Fits Your Vessel

Georgia boaters face real decisions when it comes to protecting their vessels. The right boat policy options in Georgia depend on your specific situation-your boat type, where you operate, and how often you’re on the water.

At North Point Insurance Group, we’ve helped countless boat owners find coverage that actually matches their needs. This guide walks you through the main coverage types available and how to pick the right combination for your situation.

Coverage Types That Actually Protect Your Boat

Liability Coverage Forms Your Foundation

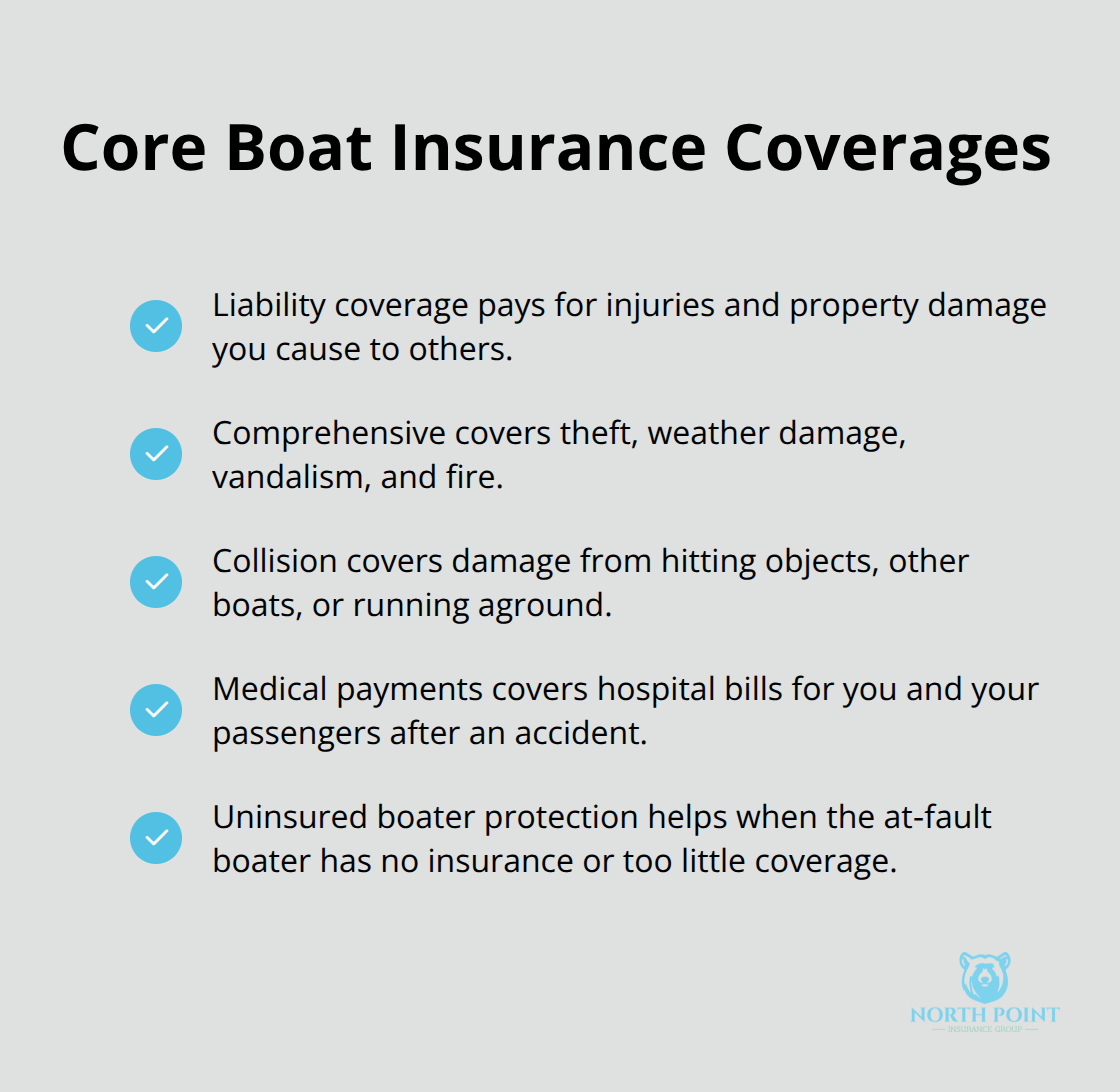

Liability coverage is the foundation of any boat policy in Georgia, and it’s the one coverage type you cannot skip. This covers bodily injury and property damage you cause to other people or their property while operating your vessel. If you hit another boat or injure a passenger, liability coverage pays for their medical bills, lost wages, and repairs-up to your policy limit. A minimum of about $300,000 in liability coverage works for most boat owners, though those with significant assets should consider higher limits. The average Georgia boat insurance policy costs around $344 annually, with liability-only options starting near $100 per year, making basic protection highly affordable.

Physical Damage Coverage Protects Your Investment

Comprehensive and collision coverage protects your own boat from damage. Comprehensive covers theft, weather damage, vandalism, and fire, while collision covers damage from hitting objects, other boats, or running aground. If you’re financing your boat, your lender will require both of these coverages. Even if you own your boat outright, these coverages are worth the cost because repair and replacement expenses for boats can run into tens of thousands of dollars.

Medical Payments and Uninsured Boater Protection

Medical payments coverage handles hospital bills for you and your passengers after an accident, regardless of who caused it-this typically costs very little but fills a critical gap. Uninsured boater protection guards you when the at-fault boater has no insurance or insufficient coverage to pay for your damages, a real risk on Georgia’s crowded lakes like Lanier and Allatoona.

Optional Add-Ons Worth Considering

On-water towing coverage costs about $30 per year and provides jump starts and fuel delivery when you’re stranded, functioning as roadside assistance for your boat. Fishing gear coverage reimburses lost or damaged equipment up to $10,000 with a $1,000 per-item limit, which matters if you carry expensive rods and electronics.

Matching Coverage to Your Situation

The specific combination of these coverages should match your boat’s value, where you operate, and your financial situation-not every boat owner needs every option, but liability and physical damage protection should be non-negotiable. Your boat type, storage location, and how frequently you use your vessel all influence which coverages make the most sense for your circumstances.

What Determines Your Boat Insurance Cost

Boat Specifications Drive Premium Differences

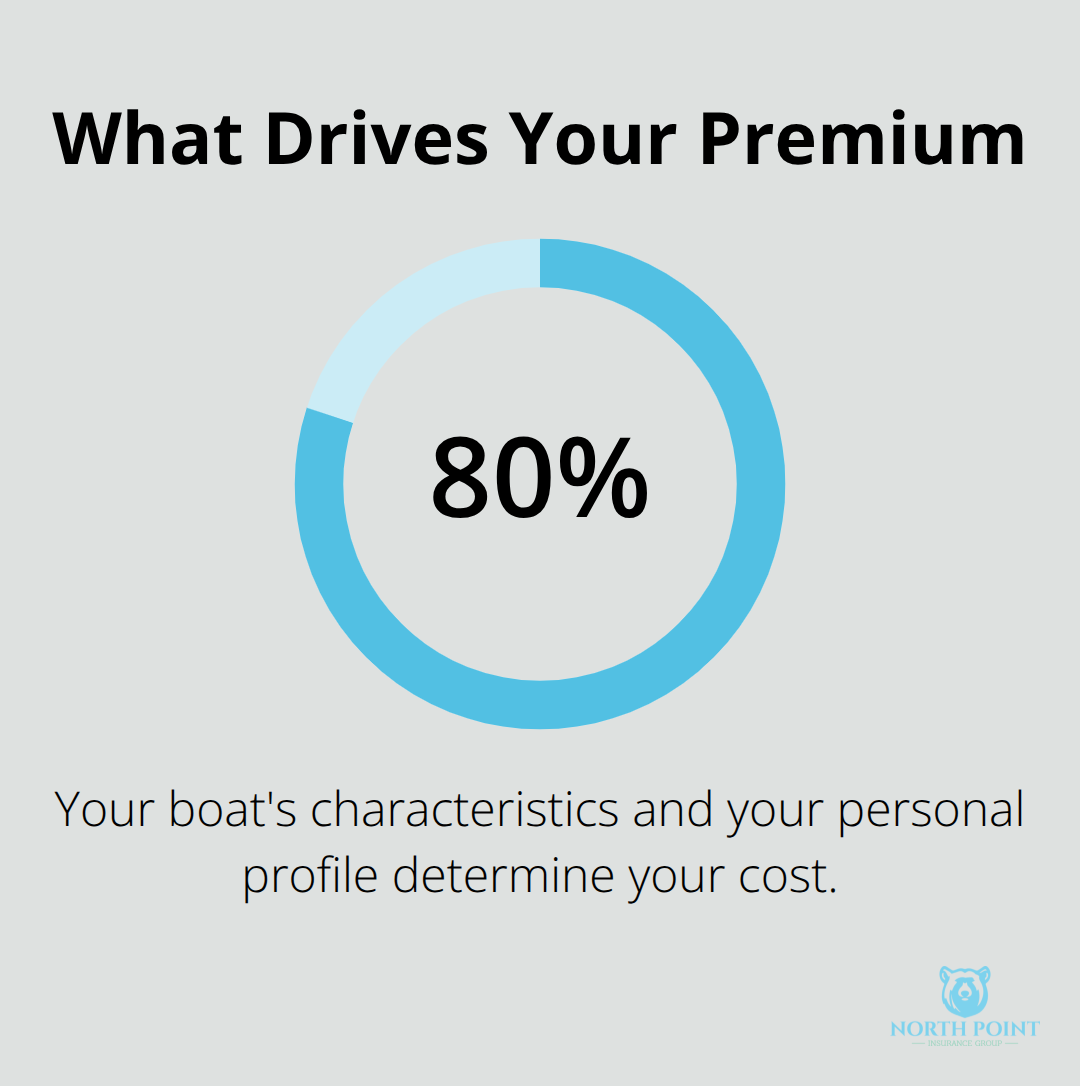

Your boat’s specifications matter far more than most owners realize. A pontoon boat and a bass boat cost completely different amounts to insure, even if they’re the same age and value. Pontoons typically run $200–$350 annually in Georgia, while bass boats range from $250–$450, and personal watercraft can swing wildly from $100–$500 depending on horsepower and engine configuration. Boat age plays a significant role too-older boats typically come with higher insurance premiums because wear and tear over time can lead to mechanical failures or structural issues. Horsepower directly impacts your premium because higher-powered engines increase accident severity and claim costs. Boat value affects your physical damage coverage costs proportionally; a $50,000 vessel will cost far less to insure than a $200,000 cabin cruiser. Your boat’s characteristics and personal profile determine roughly 80% of what you’ll pay, so understanding these factors lets you make strategic decisions about coverage levels and deductibles.

Location and Storage Shape Your Rate

Where you keep your boat and how you use it shapes your premium more than most boat owners expect. Inland boaters on lakes like Lanier and Allatoona pay significantly lower premiums than coastal operators near Savannah or Brunswick because saltwater corrosion and hurricane exposure drive up claim frequency and severity. Dry-stacked storage costs less than wet slips because boats spend less time exposed to weather and water damage. If you operate only on inland waters, specify those navigational limits to your agent-coastal coverage costs more and you won’t need it. Keeping your boat insurance in effect year-round avoids costly gaps in coverage, though winter lay-up offers real savings when you store the boat during December through February.

Your Boating History and Education Matter

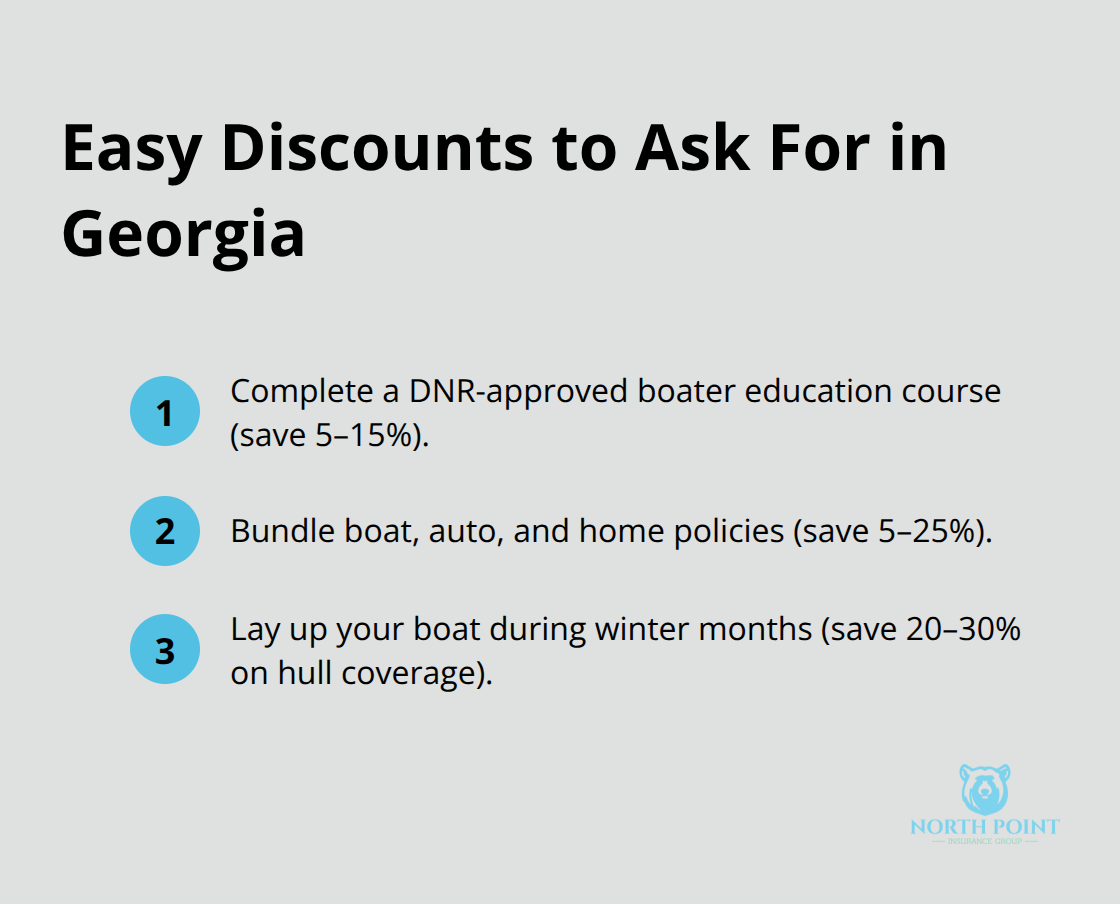

Your boating history matters tremendously-prior claims, accidents, or violations will increase your rate substantially. Someone born after January 1, 1998 must complete a DNR-approved boater education course to legally operate in Georgia, and completing that course typically reduces premiums by 5–15%. Your driving history outside boating also factors in because insurers view it as an indicator of overall risk management. Operating frequency influences cost because boats that sit unused face different risks than those on the water every weekend.

How Operating Patterns Affect Your Premium

The way you actually use your boat determines which coverage options you truly need and what you’ll pay for them. Casual weekend boaters on calm inland lakes face lower risk profiles than those who operate in rough coastal waters or run their boats daily throughout the season. Your agent can help you match your coverage to your actual usage patterns rather than paying for protection you’ll never use. Understanding these cost drivers helps you make informed decisions about which coverages fit your vessel and which ones you can adjust to manage your premium.

How to Match Coverage to Your Actual Boating Life

Your coverage decisions should reflect how you actually use your boat, not how a generic boat owner might use theirs. Start by assessing your risk exposure on the water honestly. If you operate only on calm inland lakes like Lake Lanier during daylight hours on weekends, your risk profile looks completely different from someone who runs a fishing boat daily in coastal waters near Savannah. Inland boaters typically pay $344 annually on average in Georgia, but coastal operators often face 20–30% higher premiums due to saltwater exposure and hurricane risk. The specific waters where you operate should drive your coverage decisions. A boat stored in a dry stack facility faces far lower theft and weather damage risk than one left in a wet slip, so your comprehensive coverage needs shift accordingly. If you finance your boat, your lender will require both collision and comprehensive coverage regardless of your risk assessment, but if you own outright, you have the flexibility to adjust your deductibles based on actual exposure. Someone who takes their boat out twice monthly can often reduce costs by specifying lower annual operating hours to their agent, while someone who runs a charter operation needs completely different protection.

Finding the Right Deductible Level

Your deductible choice directly impacts both your monthly premium and your out-of-pocket risk. Higher deductibles like $2,500 or $5,000 can reduce your annual premium by 15–25%, but you need enough liquid savings to handle that amount if damage occurs. Most casual boaters find a $1,000 deductible strikes the right balance between affordability and manageable risk. If you maintain an excellent boating record with no prior claims and operate only during calm season months, a higher deductible becomes more reasonable. The Ahoy! mobile app offers boaters a $100 annual deductible discount for completing their self-inspection tool, which means you can effectively lower your deductible through proactive maintenance documentation. Your liability coverage limit should match your financial exposure-those with significant assets should carry at least $500,000 in liability rather than the minimum $300,000, because a serious injury claim can easily exceed $300,000 in medical and legal costs. Don’t assume homeowners insurance covers your boat adequately; most policies explicitly exclude liability on watercraft, and physical damage limits for boats are typically too low to matter.

Working with Agents Who Understand Your Boat

An independent agent who specializes in boat insurance can shop multiple carriers to find better rates than you’d find online alone. A quality agent will ask detailed questions about your boat’s horsepower, age, value, and how you operate it-not just sell you a standard policy. They can identify discounts you’d miss on your own: completing a DNR-approved boater education course typically saves 5–15%, bundling boat insurance with auto and homeowners policies saves another 5–25%, and if you lay up your boat during winter months, you can capture 20–30% savings on hull coverage. An agent can also explain policy exclusions that matter-racing, commercial use, and trips beyond your stated navigational limits won’t be covered, so you need to match your limits to your actual plans.

Most importantly, a local agent can issue marina certificates immediately when you need dockage, saving you days of delay compared to online-only carriers.

Final Thoughts

Choosing the right boat policy options Georgia boat owners actually need comes down to matching your coverage to how you use your vessel. You now understand the core coverages available-liability, comprehensive, collision, medical payments, and uninsured boater protection-and you know which factors drive your premium: boat type, horsepower, storage location, and your boating history. The real work happens when you assess your specific situation honestly and decide which coverages fit your risk profile and budget.

Start by gathering your boat’s details: hull ID, year, make, model, horsepower, and where you store it. Be clear about how you actually use your boat-whether you’re a casual weekend boater on Lake Lanier or someone who operates year-round in coastal waters near Savannah. This information lets you have a productive conversation with an agent who can explain your options without pressure and help you identify discounts you’d miss on your own.

Contact North Point Insurance Group today to discuss your boat insurance needs. Our local agents shop multiple carriers to find coverage that protects your investment without wasting money on protection you don’t need, and we can issue marina certificates the same day when you need them.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.