Excess Liability Protection With Personal Umbrella Insurance

A single lawsuit can wipe out years of financial progress. At North Point Insurance Group, we see homeowners and business owners face liability claims that far exceed their standard home and auto coverage limits.

Excess liability protection through a personal umbrella policy fills that gap. It’s an affordable way to shield your assets from catastrophic claims that could otherwise devastate your finances.

What Your Umbrella Policy Actually Covers

A personal umbrella policy activates after your underlying home and auto liability limits are exhausted, covering bodily injury, property damage, and personal injury claims that exceed those base limits. Typical umbrella policies start at $1 million in coverage, with many households carrying limits between $1 million and $5 million. If a guest suffers a serious injury on your property and the medical bills, lost wages, and pain-and-suffering damages total $750,000 but your homeowners liability maxes out at $500,000, your umbrella covers the remaining $250,000. Similarly, in an auto accident where you’re found liable for $600,000 in bodily injury damages but your auto policy covers only $300,000, the umbrella steps in for the gap. This layered approach costs roughly $300 to $500 annually for $1 million of coverage according to industry data, making it far cheaper than raising your underlying policy limits to those amounts.

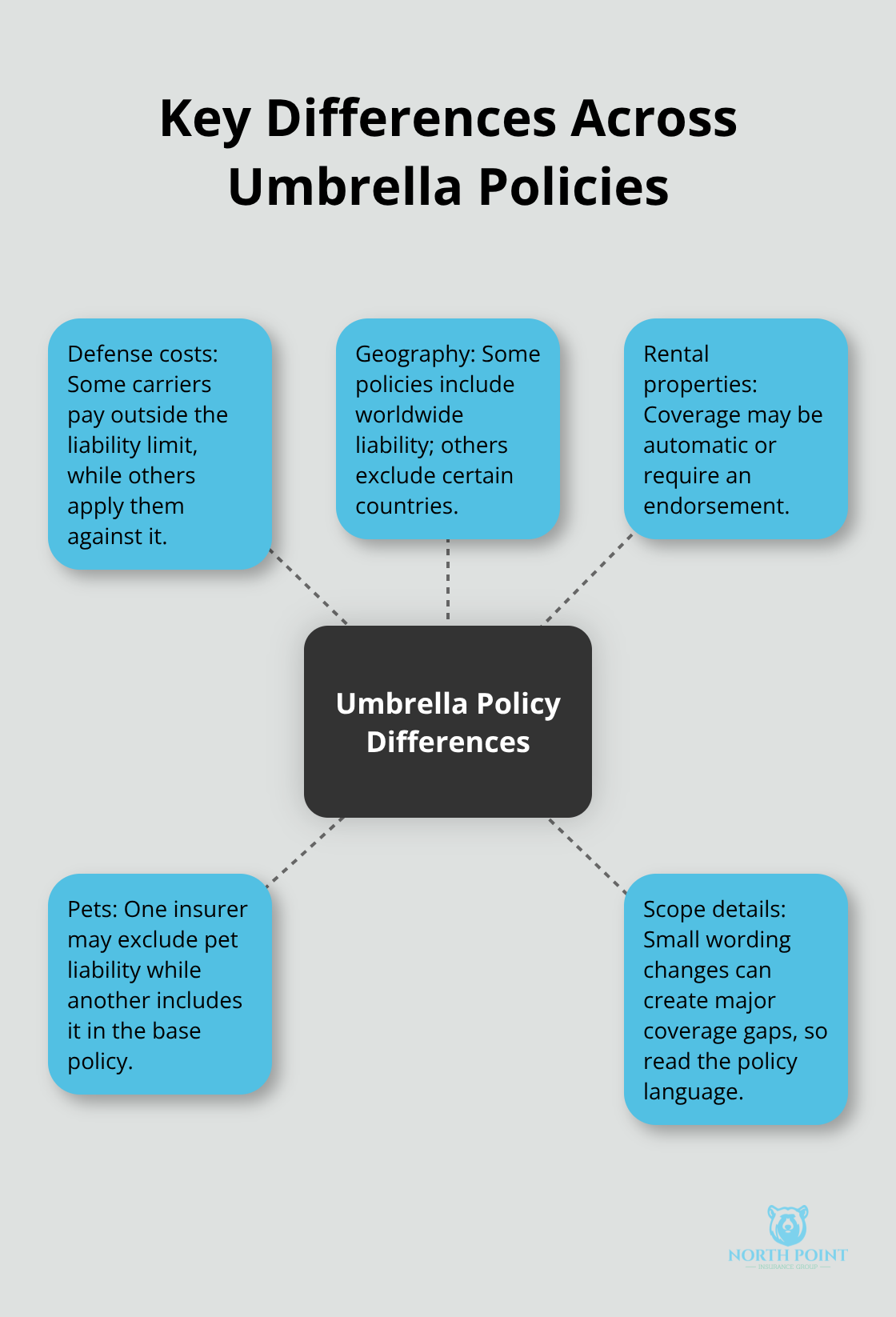

Defense Costs and Legal Fees

Your umbrella policy covers legal defense costs even if a lawsuit against you proves groundless. These expenses add up fast-attorney fees, court costs, and expert witness testimony can easily reach tens of thousands of dollars before any settlement or judgment. The umbrella pays these defense costs in addition to covering the actual liability judgment, protecting both your assets and your cash flow during litigation. Some policies structure defense costs outside the policy limit, meaning a $1 million umbrella provides $1 million for the judgment plus separate coverage for legal fees. Others apply defense costs against your limit, so verify this detail with your agent when comparing quotes.

Personal Injury and Reputation Protection

Beyond physical injuries and property damage, umbrella policies cover personal injury claims including defamation, false arrest, and invasion of privacy. If someone claims you made a false statement that damaged their reputation or business, your umbrella can cover the settlement and legal costs. This coverage extends to statements made online, on social media, or in published materials. Homeowners with pools, rental properties, or who frequently host gatherings face elevated exposure here-a guest injury at a backyard event or a dispute with a tenant can quickly spiral into costly litigation that standard policies won’t fully cover. Understanding what your umbrella actually protects sets the stage for determining how much coverage you truly need.

Why Liability Claims Threaten Your Financial Security

Settlement Amounts Keep Rising

Liability claims are growing larger and hitting faster than most homeowners expect. The Insurance Information Institute reports that average settlement amounts for serious injury claims have climbed substantially over the past decade, with some cases reaching well into six figures or beyond. A single incident-a guest falling on your property, a dog bite, or an accident you cause while driving-can generate medical bills, lost wages, pain and suffering damages, and legal costs that far exceed your standard homeowners or auto coverage.

When serious injuries occur, medical expenses and court judgments accumulate quickly. If you carry a $500,000 homeowners liability limit and face a $750,000 claim, that $250,000 gap comes directly from your savings, investments, or future income. Without umbrella coverage, you remain personally liable for every dollar above your policy limits. The cost difference is striking: raising your homeowners liability from $500,000 to $1 million might add $200 to $300 annually to your premium, while a $1 million umbrella policy costs roughly $300 to $500 per year-often cheaper than increasing underlying limits alone.

Your Assets Face Direct Attack in Lawsuits

Your assets and future earnings become targets in a major lawsuit. The Insurance Information Institute notes that creditors can pursue your bank accounts, investment portfolios, rental property income, and even garnish future wages to satisfy a judgment. Retirement accounts like 401(k)s receive some protection under federal law, but most liquid assets remain vulnerable.

Homeowners with substantial equity, rental properties, investment portfolios, or steady professional income face the highest exposure because they have the most to lose. A $1 million judgment against you doesn’t disappear if you can’t pay it immediately-it becomes a lien on your assets and a claim against your future income for years. Umbrella insurance breaks this chain by covering the excess liability before it touches your net worth.

When Your Net Worth Becomes a Liability Risk

If you own a home worth $600,000, carry investments of $400,000, and earn $150,000 annually, a $1.5 million liability judgment could devastate decades of financial progress in a single verdict. This is why umbrella coverage becomes essential the moment your assets exceed roughly $500,000, and increasingly important as your net worth climbs higher. The question shifts from whether you need protection to how much coverage actually shields your specific situation.

Sizing Your Umbrella to Match Your Real Liability Risk

Start by calculating what you actually stand to lose in a lawsuit. Add up your home equity, investment accounts, rental property value, and annual income. If your home is worth $500,000 with $300,000 in equity remaining, you hold $200,000 in stocks, earn $120,000 annually, and own a rental property valued at $250,000, your total exposure sits around $770,000. This is the floor for your umbrella coverage. The Insurance Information Institute recommends that households with assets exceeding $1 million carry at least $3-5 million in umbrella protection. Your calculation should be conservative-factor in potential future earnings and asset growth over the next five to ten years. A professional earning $150,000 annually could accumulate another $500,000 to $750,000 in wealth over a decade, so your umbrella limit should account for where your net worth is headed, not just where it sits today.

Verify Your Underlying Policy Minimums First

Umbrella policies don’t stand alone. Most insurers require minimum liability limits on your homeowners and auto policies before issuing an umbrella. The National Association of Insurance Commissioners notes that carriers typically demand homeowners liability of at least $300,000 and auto bodily injury coverage of at least $250,000 to $300,000 per person before they’ll sell you a $1 million umbrella. If your current homeowners policy carries only $100,000 in liability or your auto coverage maxes out at $100,000 per person, you’ll need to increase these underlying limits first-and that costs money. Many homeowners discover they must also raise their base policies to qualify after assuming a cheap umbrella solves everything. Calculate the full cost upfront: increasing homeowners liability from $300,000 to $500,000 might add $150 annually, and bumping auto bodily injury from $250,000 to $500,000 might add another $200 to $300 per year. Only after meeting these minimums can you layer on the umbrella. This coordination is non-negotiable because the umbrella only activates after those underlying limits exhaust.

Compare Quotes and Examine Policy Details Carefully

Don’t assume all $1 million umbrellas are identical. Call three to five insurers and request quotes, providing the same information to each: your home value, vehicles owned, driving history, claims history, and desired coverage limit. When quotes arrive, the premiums might range from $280 annually to $450 for the same $1 million limit-that’s a $170 spread worth investigating. Read the policy details carefully. Some carriers include defense costs outside your limit; others apply them against it. Some cover worldwide liability; others exclude certain countries.

Some include rental property coverage automatically; others require an endorsement. One insurer might exclude pet liability entirely while another covers it under the base policy. These gaps matter enormously. A homeowner with a dog that bites someone faces a claim that might not be covered under one carrier’s umbrella but fully protected under another’s. Request the actual policy language or at least a detailed coverage summary, not just the premium. The $50 annual savings on a cheaper umbrella evaporates instantly if that policy excludes a liability scenario you actually face.

Final Thoughts

Excess liability protection through a personal umbrella policy transforms how you defend your financial future. A $1 million umbrella costs roughly $300 to $500 annually, yet shields hundreds of thousands of dollars in home equity, investments, and future earnings from a single lawsuit. Without it, a serious liability claim erases years of financial progress and leaves you personally responsible for judgments that far exceed your standard homeowners and auto coverage.

Start with an honest assessment of what you own and what you stand to lose. Calculate your home equity, investment accounts, rental properties, and projected future income-if that total exceeds $500,000, umbrella coverage moves from optional to essential. Then verify your underlying policy limits meet your insurer’s minimums, compare quotes from multiple carriers, and read the actual policy language to confirm coverage for your specific risks.

Contact North Point Insurance Group to discuss your liability exposure and get a quote. Our independent agents shop multiple carriers to find policies that match your actual liability exposure and financial situation. The cost is minimal, but the protection you gain is invaluable.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.