Young Driver Insurance Georgia: What Families Should Know

Adding a young driver to your family’s auto insurance policy in Georgia comes with sticker shock. At North Point Insurance Group, we’ve helped countless families navigate the costs and coverage decisions that come with insuring a teen behind the wheel.

This guide breaks down why young drivers cost more, how to cut those expenses, and what coverage your family actually needs in Georgia.

Why Young Drivers Cost So Much

Eighteen-year-olds in Georgia pay about $8,189 per year for full-coverage auto insurance, according to Bankrate. That’s nearly triple the state average of $2,909. Insurers see teenage drivers are statistically riskier because young drivers lack the thousands of hours of real-world experience that build judgment behind the wheel. A teen’s brain is still developing the neural pathways that handle split-second decisions in traffic. Insurers price that gap in maturity directly into premiums. The cost difference narrows as drivers age-19-year-olds pay roughly 37% more than their 20-year-old counterparts on individual policies-but the penalty for youth remains steep. This isn’t speculation or worst-case thinking. Bankrate’s data reflects actual premium patterns across Georgia’s insurance market, and the pattern holds across every major carrier.

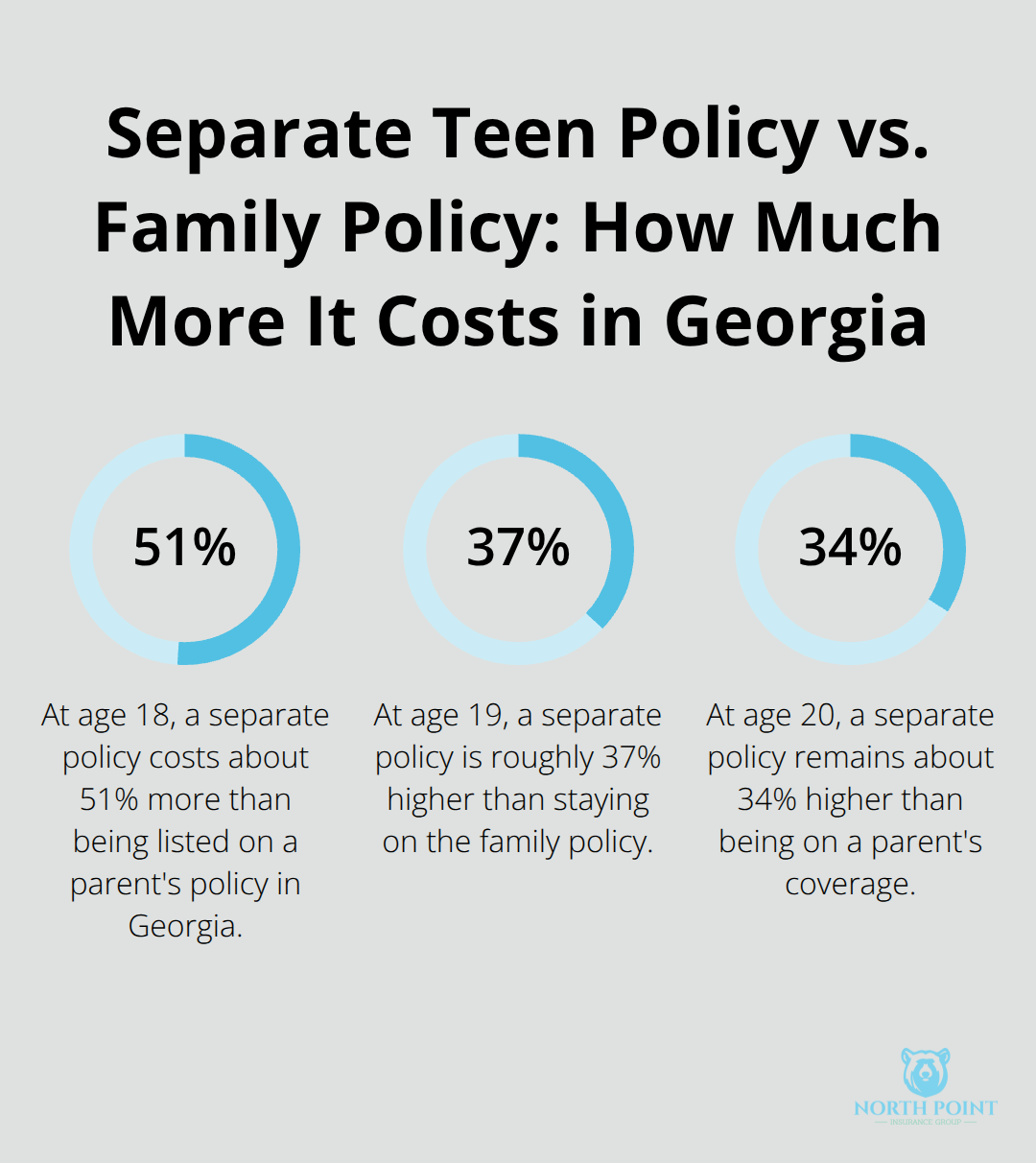

The Independent vs. Dependent Choice Matters Most

The single biggest financial decision isn’t which coverage level to pick-it’s whether your teen stays on your family policy or gets their own. An 18-year-old on a separate policy pays about 51% more than the same driver listed on a parent’s existing coverage. At 19, that gap shrinks to 37% higher. At 20, it’s still 34% higher.

The math is brutal. If your family’s full-coverage premium runs $2,909, adding a teen to that policy costs far less than letting that teen purchase coverage independently. Insurers charge less when a teen shares a policy with an experienced driver, partly because they expect parental oversight to reduce risky behavior. Your own driving record directly affects your teen’s rates too-if you’ve accumulated violations or accidents, your teen might actually pay less on a separate policy, though this scenario is uncommon. The practical takeaway: keep your teen on your policy unless your own driving history is significantly damaged.

Location and Vehicle Type Stack the Costs

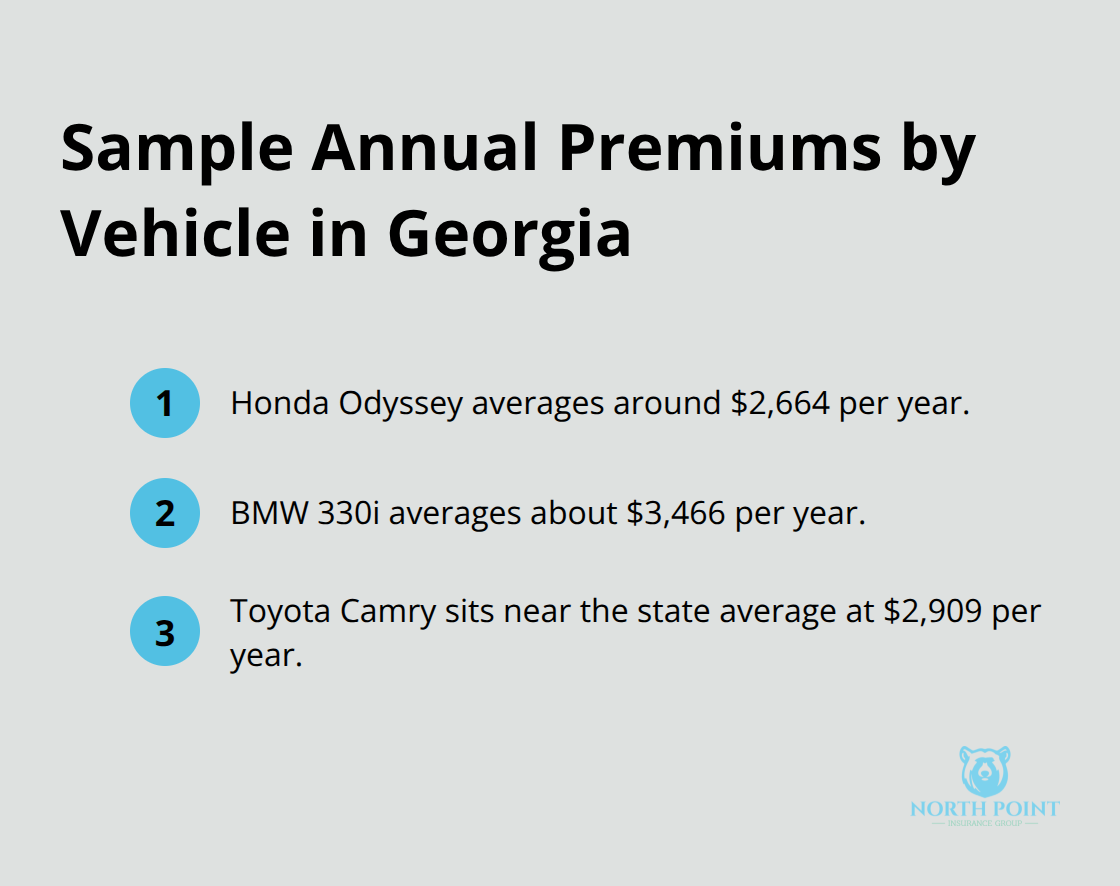

Where you live in Georgia shifts premiums noticeably. Atlanta drivers pay about 18% more than the state average, while Augusta sits roughly 10% below it. That geographic variation matters when you shop for coverage. The vehicle your teen drives matters equally. A Honda Odyssey averages around $2,664 annually in Georgia, while a BMW 330i climbs to $3,466. A Toyota Camry sits near the state average at $2,909.

Insurers price based on repair costs, theft risk, and safety ratings. A used, reliable sedan costs less to insure than a sporty car or an expensive model. This is one area where you have direct control. Selecting a safe, practical vehicle for your teen reduces insurance costs immediately and continues saving money throughout their driving years.

What Happens When You Add a Teen to Your Policy

Adding your teen to your existing policy triggers a rate increase, but the amount depends on several factors working together. Your location, the vehicle your teen will drive, and your own driving record all influence the final number. If you live in Atlanta with a higher-risk vehicle, expect a steeper increase than a family in a rural area with a practical sedan. The good news: this increase is still substantially cheaper than your teen purchasing a separate policy. Most families see their premiums rise by several hundred dollars annually when they add a teen driver, not the thousands that independent teen policies command. Understanding these cost layers helps you make informed decisions about coverage levels and vehicle choices before your teen hits the road.

How to Cut Young Driver Insurance Costs

The premiums we quoted earlier don’t have to be your final answer. Georgia families have multiple levers to pull that meaningfully reduce what they pay for young driver coverage.

Good Grades Deliver Immediate Savings

The good student discount offers the fastest path to lower premiums. Students who earn good grades might qualify for cheaper car insurance, generally reducing total costs by 10 to 25 percent. That discount can apply through age 25 for some insurers, which extends the savings well beyond the first year of driving. Homeschooled teens qualify too-they need to show strong performance on a national standardized test taken within the past 12 months. On an 18-year-old’s $8,189 annual premium, a 25 percent discount saves your family over $2,000 per year. This isn’t a bonus that disappears after one year. The discount persists as long as your teen maintains the GPA threshold, making academic performance directly tied to insurance costs.

Driver Education Counts Double

Completing a driver education course satisfies Georgia’s Joshua’s Law requirements and qualifies teens under 21 for an additional insurance discount. You’re not paying twice-the course counts toward graduation requirements and toward insurance savings simultaneously. The combination of good grades and driver education can stack discounts that total 30 to 40 percent off the base rate, turning an $8,189 premium into something closer to $5,000 annually. This approach addresses the core reason insurers charge more for young drivers: lack of formal training and real-world experience. When your teen completes an approved program, insurers recognize that structured instruction reduces accident risk.

Bundling Multiplies Your Savings

Bundling your auto policy with home or life insurance creates substantial savings. Liberty Mutual reports that customers who bundle auto with home insurance can save over $950, and that’s before any teen-specific discounts apply. Once you add your teen to a bundled policy, the savings compound. Your teen’s presence on the policy triggers a smaller rate increase than if they were insured separately, and the bundling discount applies to the entire package. This strategy works because insurers reward customer loyalty and reduced administrative costs by offering lower rates across multiple policies.

Usage-Based Programs Reward Safe Driving

Usage-based insurance programs like RightTrack reward safe driving behavior with savings up to 30 percent for drivers who maintain low-risk habits. These programs use a mobile app to track acceleration, braking, speeding, and time of day spent driving. If your teen drives responsibly, the app rewards that behavior directly. This approach works because it shifts the focus from age and statistics to actual driving patterns. A 17-year-old who drives cautiously at safe speeds and avoids nighttime highways can earn lower rates than a reckless 25-year-old. The data matters more than the birthday.

Stacking Strategies Creates Real Results

These three strategies-grades, bundling, and telematics monitoring-address the core reason young drivers cost more: perceived risk. When you stack them, you’re no longer fighting the system. You’re proving to insurers that your teen represents lower risk than the average young driver, and your premium reflects that reality. The next step involves understanding which coverage options actually protect your family and which ones you can safely skip in Georgia.

Coverage Options Every Georgia Family Needs

Georgia law mandates minimum liability coverage of $25,000 per person and $50,000 per accident for bodily injury, plus $25,000 for property damage. These minimums exist because they reflect the bare-bones threshold where your family won’t face legal consequences for driving without insurance. They do not reflect the actual cost of a serious accident. A single collision involving your teen can generate medical bills exceeding $100,000, vehicle damage in the tens of thousands, and lost wages that stretch for months. If your teen causes that accident and you only carry the state minimum, you’re personally liable for everything beyond those limits. Your family’s savings, future earnings, and assets become vulnerable.

Why Higher Liability Limits Matter

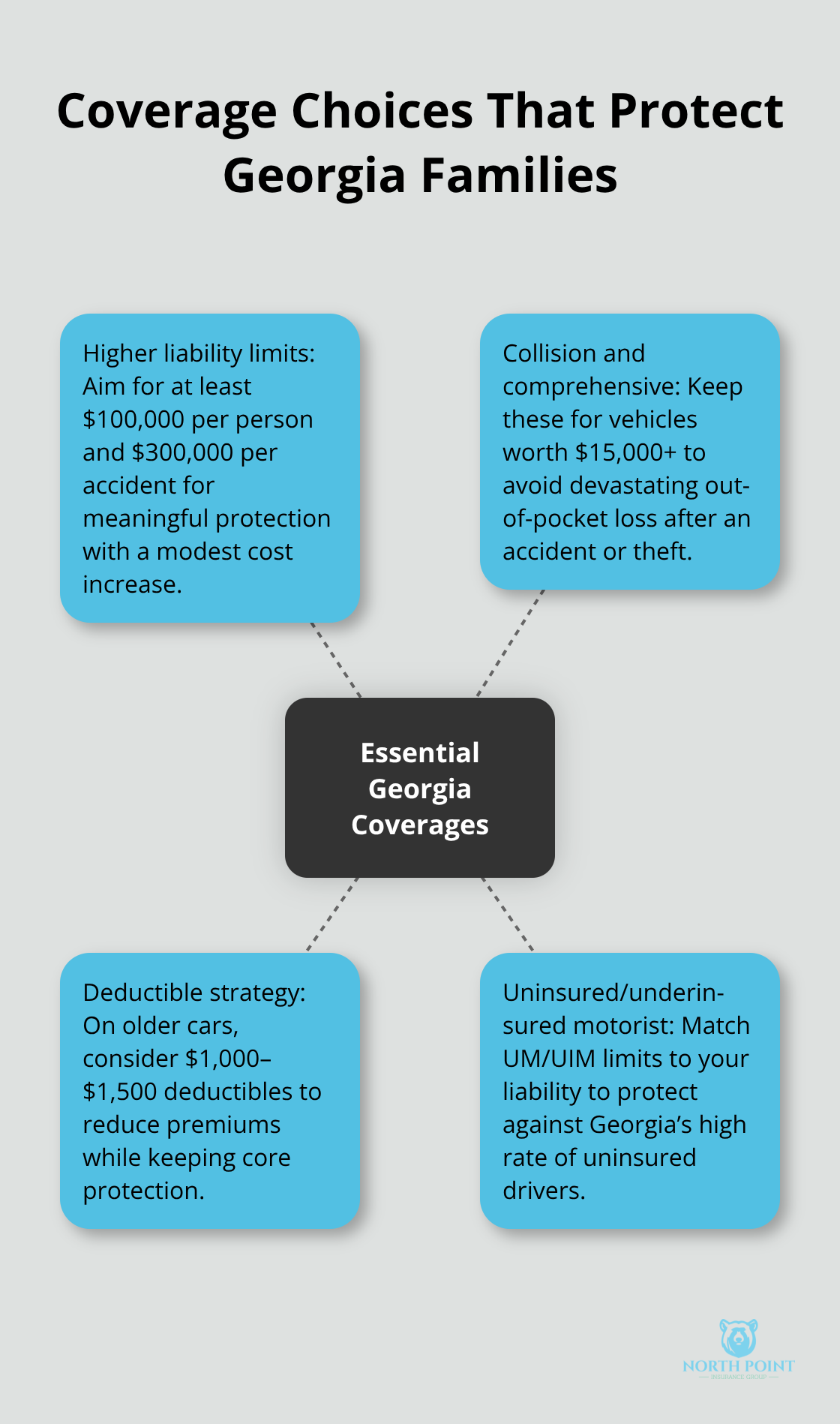

We recommend carrying at least $100,000 per person and $300,000 per accident in liability coverage, particularly when insuring a young driver. That higher threshold costs relatively little more than the minimum but provides genuine protection against financial catastrophe. The difference between $25,000 and $100,000 in liability coverage typically adds $20 to $40 per month to your premium-an affordable safeguard against a worst-case scenario. Young drivers lack the experience to avoid high-impact collisions, making this upgrade essential rather than optional.

Collision and Comprehensive: When They Make Sense

Collision and comprehensive coverage protects your teen’s vehicle rather than other people’s property, which means Georgia law treats them as optional but practicality demands a closer look. Collision covers damage from accidents, while comprehensive handles theft, weather, and vandalism. If your teen drives a vehicle worth $15,000 or more, skipping these coverages creates unnecessary risk. A single accident could total the car, leaving your family without transportation and without the funds to replace it.

If your teen drives a ten-year-old sedan worth $3,000, the math shifts. Carrying comprehensive and collision with a $1,000 deductible might cost more annually than the car’s replacement value, making it economically irrational. Consider your family’s ability to absorb a loss.

If losing the vehicle would create genuine hardship, carry the coverage. If you could replace it from savings without stress, raising the deductible to $1,000 or $1,500 reduces premiums while keeping basic protection intact.

Uninsured Motorist Coverage: Georgia’s Hidden Risk

Uninsured and underinsured motorist coverage deserves particular attention in Georgia because uninsured motorists represent a significant portion of drivers on Georgia roads. If your teen is hit by an uninsured driver, your liability coverage won’t help because the at-fault driver has no policy to pursue. Uninsured motorist coverage steps in, covering medical bills and vehicle damage up to your policy limits.

Underinsured motorist coverage handles situations where the at-fault driver carries insurance but insufficient coverage to pay for your family’s damages. These protections cost minimal additional premium but address a genuine Georgia-specific risk. Adding uninsured motorist coverage with limits matching your liability coverage ensures your teen receives the same protection whether they cause an accident or fall victim to one.

Final Thoughts

Insuring a young driver in Georgia requires you to balance cost control with genuine protection. The strategies we’ve outlined work because they address the real reasons insurers charge more for teen drivers: inexperience, statistical accident rates, and unpredictable decision-making. Keeping your teen on your family policy, stacking discounts for good grades and driver education, bundling your coverage, and monitoring driving habits through usage-based programs transforms young driver insurance Georgia from a financial burden into a manageable expense.

The coverage decisions matter equally. Georgia’s minimum liability limits leave your family exposed to catastrophic financial loss, so raising those limits to $100,000 per person and $300,000 per accident costs relatively little while protecting everything you’ve built. Collision and comprehensive coverage depend on your vehicle’s value and your family’s financial cushion, but uninsured motorist protection is non-negotiable in Georgia given the prevalence of uninsured drivers on the road.

Getting started means you gather quotes from multiple carriers and compare actual rates for your specific situation. Location, vehicle type, driving record, and available discounts all shift the final number, which is why generic estimates miss the mark. Contact us at North Point Insurance Group for a free quote tailored to your family’s situation, and we’ll walk you through the options and show you exactly what your teen’s coverage costs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.