Boat Liability Coverage Georgia: What It Covers

A single accident on Georgia’s waterways can cost you thousands in damages and legal fees. Boat liability coverage in Georgia protects you when you’re found responsible for injuries or property damage caused by your vessel.

At North Point Insurance Group, we’ve seen too many boaters operate without adequate coverage, leaving themselves exposed to serious financial risk. Understanding what your policy covers is the first step toward protecting your boating activities and your wallet.

What Your Boat Liability Coverage Actually Pays For

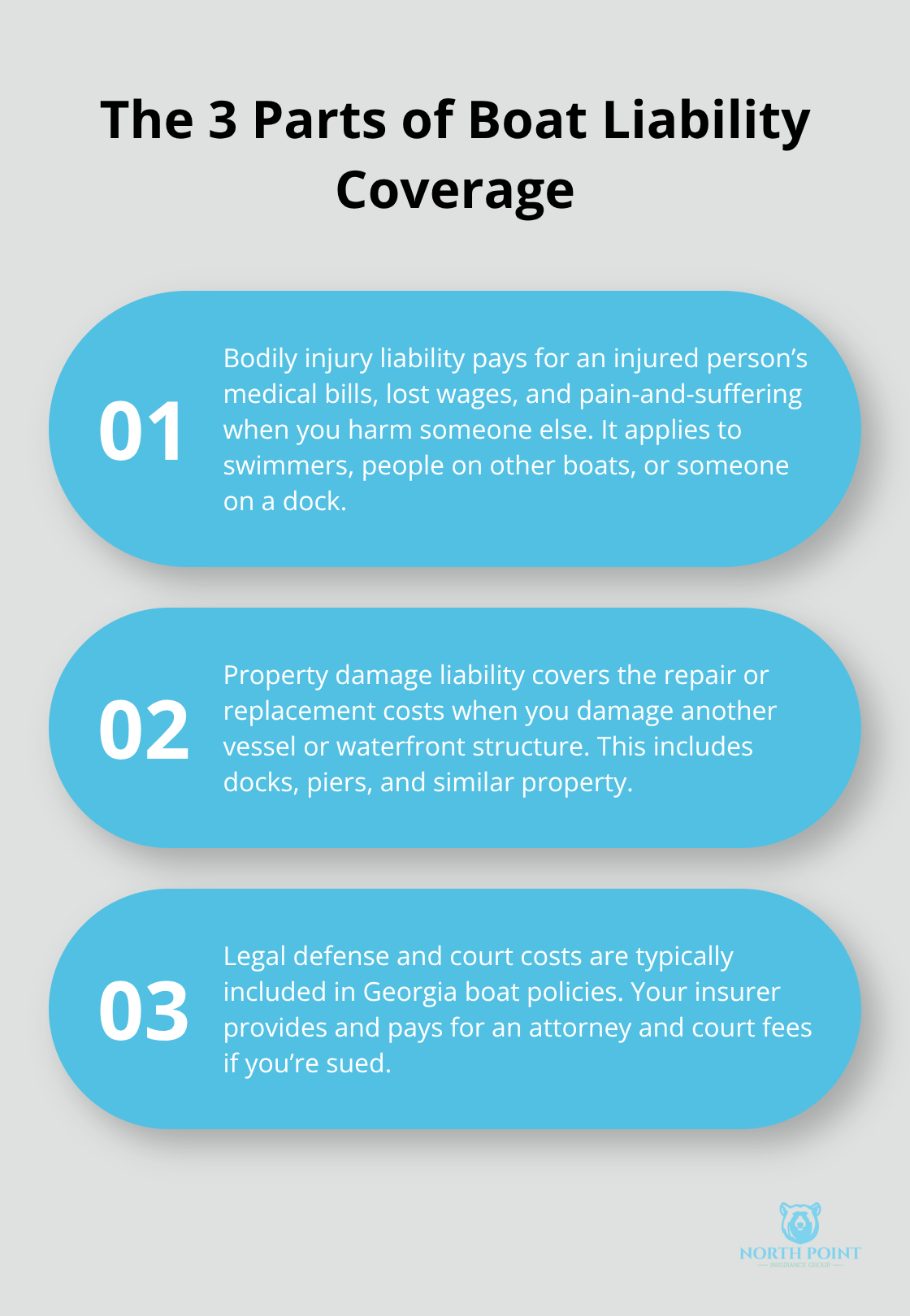

Boat liability coverage protects you when you cause injury or damage to someone else on the water. It breaks down into three key components that work together to cover your financial exposure. Bodily injury liability covers medical expenses, lost wages, and pain-and-suffering claims when you injure another person-whether that’s a swimmer, a passenger on another boat, or someone on a dock.

Property damage liability handles the cost of repairs or replacement when you damage another vessel, dock, pier, or waterfront structure. Legal defense and court costs are automatically included in most Georgia boat policies, meaning your insurer pays for your attorney and court fees if you’re sued. This protects you from paying thousands out of pocket just to defend yourself.

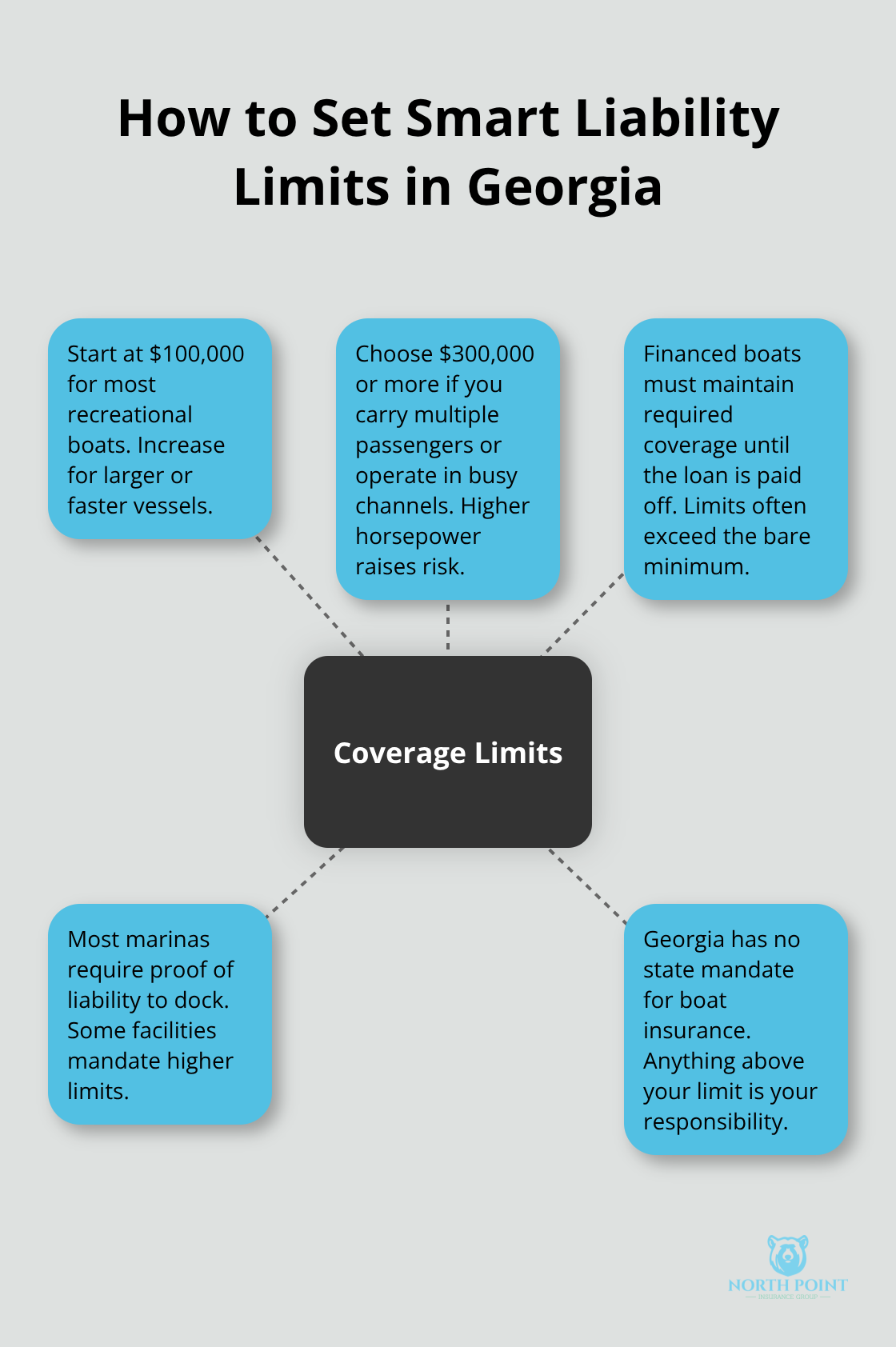

According to Progressive, boat liability coverage in Georgia can start as low as $100 per year for liability-only policies, though the actual amount you need depends on your boat’s size, horsepower, and how you use it. A common professional recommendation is to carry at least $100,000 in liability coverage, with higher limits for faster or larger vessels that pose greater risk. If you finance your boat through a lender, they typically require you to maintain liability coverage until the loan is paid off, so check your loan documents to confirm minimum limits.

How Much Coverage Actually Protects You

The liability limit you choose directly determines how much your insurer will pay for claims against you. Anything beyond that limit becomes your personal responsibility. If you cause an accident that results in $150,000 in damages but your policy only covers $100,000, you’re liable for the remaining $50,000 out of your own pocket.

This is why you should assess your boat’s value and your boating habits before you select limits. A 25-foot center console with a 300 HP engine poses far more risk than a small pontoon, and your coverage should reflect that difference. Most marinas in Georgia require proof of liability coverage as a condition for docking, so you’ll need adequate limits to meet their requirements when you moor your boat.

Why Medical Payments Coverage Matters Separately

Medical payments coverage differs from bodily injury liability because it covers your passengers and yourself regardless of fault. It pays up to your policy limit for injuries sustained on board. If your passenger hits their head on a low cabin ceiling or sustains an injury during a water-skiing accident, medical payments coverage pays their medical bills without requiring them to prove you were negligent.

This coverage is inexpensive to add and prevents disputes with injured passengers over who was responsible. It makes a practical addition to any Georgia boat policy. Your passengers receive treatment quickly, and you avoid potential legal conflicts that could arise from unclear liability.

Understanding Your Real Financial Exposure

The gap between what you think you’re covered for and what you actually are covered for creates serious financial risk. Many boat owners underestimate the cost of a single accident-a collision with another vessel, injuries to multiple swimmers, or damage to a waterfront structure can easily exceed $100,000. Your policy limits should match the worst-case scenario you could realistically face on Georgia’s waterways, not just the minimum amount a lender requires.

When you select your coverage limits, consider the boats and property you typically encounter, the number of passengers you carry, and the speed at which you operate. Higher limits cost more upfront but protect you from catastrophic out-of-pocket expenses. Now that you understand what liability coverage actually covers, the next step is to examine Georgia’s specific boating laws and what they require of boat owners.

Georgia’s Boat Liability Requirements and What Happens Without Them

Why Georgia’s Lack of a State Mandate Matters

Georgia does not mandate boat liability insurance by state law, which surprises many boat owners who assume coverage is legally required. This legal gap does not mean you can operate without protection. If you finance your boat through a lender, they will require comprehensive and collision coverage until the loan is paid off, and most require liability limits as well. Marinas across Georgia also condition docking on proof of liability coverage, so you cannot simply ignore this requirement and expect to use public or private launch facilities. The real consequence of Georgia’s lack of a state mandate is that boat owners must take personal responsibility for carrying adequate limits-no legal floor exists to catch you if you decide to underinsure yourself.

Direct Financial Consequences of Inadequate Coverage

Penalties for operating without adequate coverage come indirectly but hit hard. If you cause an accident and lack sufficient liability limits, courts will hold you personally liable for damages beyond your policy. A single collision involving injuries to multiple people or damage to an expensive vessel can generate claims of $200,000 to $500,000 or more. Operating a personal watercraft (PWC) in Georgia without meeting federal U.S. Coast Guard standards exposes you to regulatory violations and potential confiscation of your vessel. Without insurance, you face full liability, and creditors can pursue wage garnishment and asset seizure for years, leaving you to pay all costs out of pocket.

Recommended Coverage Limits for Georgia Boaters

We recommend carrying at least $100,000 in liability limits for most recreational boats, with $300,000 or higher for faster vessels or boats with multiple passengers. This threshold aligns with professional standards and marina requirements across Georgia’s coastal and inland waterways. Your limits should reflect your boat’s horsepower, value, and how frequently you carry passengers-a 50 HP pontoon with occasional family use needs less coverage than a 300 HP center console you operate regularly in busy waters. The liability limit you select directly determines how much your insurer will pay for claims against you, and anything beyond that limit becomes your personal responsibility.

How Marina Requirements Shape Your Coverage Decisions

Most marinas in Georgia require proof of liability coverage as a condition for docking, so you will need adequate limits to meet their requirements when you moor your boat. These marina requirements typically align with the $100,000 minimum for standard recreational vessels, though some facilities with high-value boats or busy waterways may demand higher limits. Lenders also impose their own requirements, which often exceed state minimums and reflect the lender’s risk assessment of your specific vessel. Understanding these external requirements helps you avoid the frustration of purchasing a policy only to find it falls short of what your marina or lender demands. With Georgia’s boating landscape shaped by lender and marina requirements rather than state law, the next section examines the real-world scenarios where liability claims actually occur on Georgia’s waterways.

When Boat Accidents Happen on Georgia’s Waters

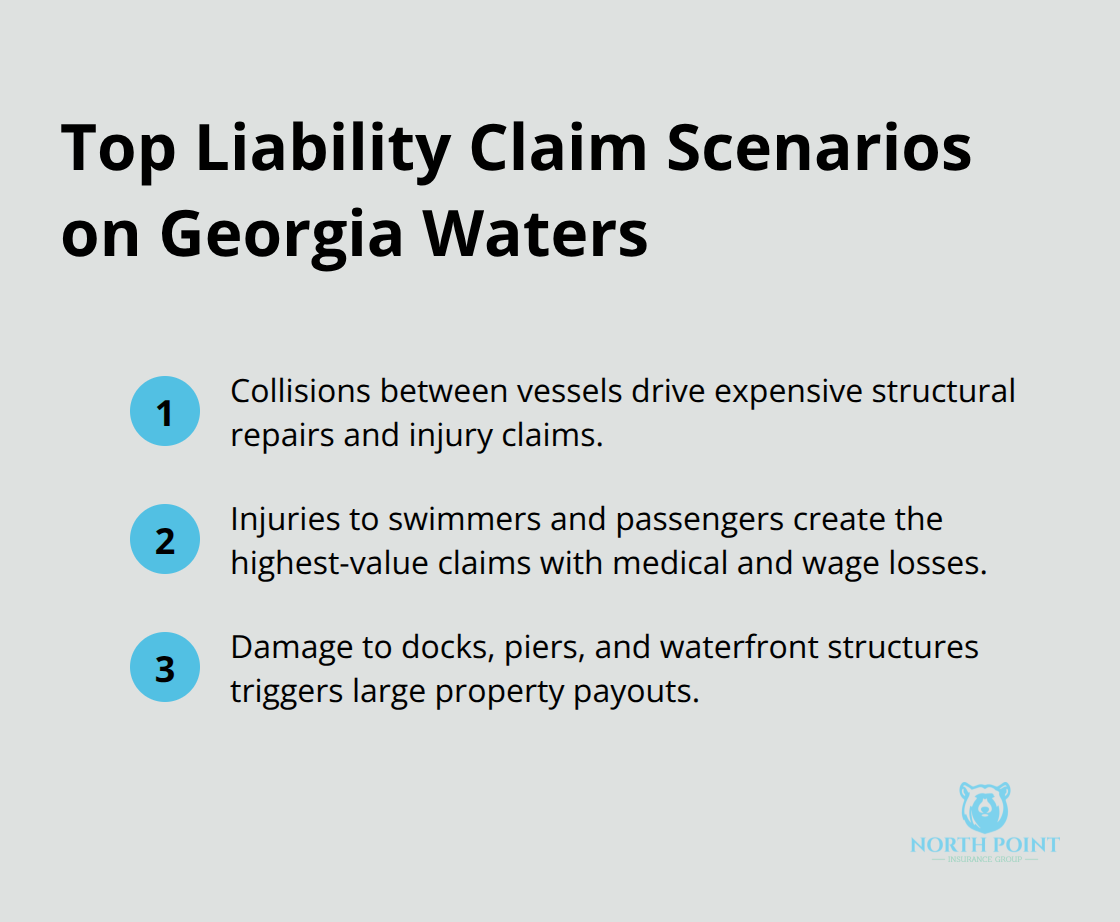

Collisions Between Vessels Cost Far More Than You Think

Boat collisions represent the most common liability claim on Georgia’s waterways, and the financial consequences escalate quickly depending on vessel size and speed. A collision between two center console boats at 20 mph generates impact forces that cause structural damage exceeding $15,000 to $40,000 per vessel, plus medical expenses if anyone sustains injury. If you operate a 300 HP boat and strike a smaller vessel piloted by someone with minimal boating experience, courts often assign higher liability to the more powerful operator, regardless of who technically caused the accident. Your liability coverage must account for the worst-case scenario-a multi-vessel pileup in a busy channel or a high-speed collision with an expensive yacht. Many Georgia boaters underestimate these costs and carry limits far below what a single accident demands, leaving themselves exposed to six-figure out-of-pocket expenses.

Injuries to Swimmers and Passengers Generate the Highest Claims

Injuries to swimmers and passengers create the highest-value claims because they involve medical expenses, lost wages, and pain-and-suffering awards that accumulate rapidly. A swimmer struck by your boat can sustain catastrophic injuries-spinal damage, amputation, or death-that generate settlements or judgments reaching millions of dollars. If you tow someone on a water ski or tube and they fall, your liability extends to their medical treatment and any permanent disability that results. Passengers aboard your vessel also fall under your liability exposure; if a guest is thrown during a sharp turn or struck by equipment, you become responsible for their injuries. Progressive reports that Georgia boat policies average about $428.57 annually, but this cost varies dramatically based on the coverage limits you select-a policy with $300,000 in limits costs significantly more than one with $100,000, yet the difference in annual premium is often just $50 to $100, making higher limits a practical investment.

Damage to Docks, Piers, and Waterfront Infrastructure

Damage to docks, piers, and waterfront structures represents a third major claim category that boat owners frequently overlook. When you misjudge your approach and strike a dock or pier, repair costs range from $5,000 for minor damage to $50,000 or more if you damage structural pilings or electrical systems. If your boat strikes a neighbor’s dock and causes injuries to someone standing on it, your liability expands to include both property damage and bodily injury claims simultaneously.

Marina facilities with fuel pumps, electrical pedestals, or swimming areas amplify your exposure because damage to shared infrastructure affects multiple users, and the marina itself may pursue claims for lost business during repairs.

Why Higher Limits Protect Your Financial Future

Try selecting liability limits of at least $300,000 if you carry passengers regularly or operate in busy channels, with $500,000 preferred for faster boats. This threshold protects you from the financial devastation that accompanies serious injuries or damage to expensive waterfront property, and the annual premium increase is modest compared to the catastrophic risk you eliminate. Watercraft insurance in Georgia protects your boat and your financial future when accidents happen on the water, with hull coverage and collision protection defending against major losses. The difference between a $100,000 policy and a $300,000 policy amounts to roughly $50 to $100 per year-a small price for protection that covers realistic accident scenarios on Georgia’s waterways. Your boat’s horsepower, the number of passengers you typically carry, and the waters where you operate should all influence your final decision on coverage limits.

Final Thoughts

Boat liability coverage in Georgia protects you from financial devastation when accidents happen on the water, yet many boat owners carry limits far below what realistic accident scenarios demand. The three core components of your policy-bodily injury liability, property damage liability, and legal defense costs-work together to cover your exposure when you injure someone or damage property. Medical payments coverage adds an extra layer by protecting your passengers regardless of fault, preventing disputes and ensuring quick treatment after an accident.

Georgia’s lack of a state insurance mandate creates a false sense of security for many boaters, but your lender and marina will impose their own requirements, and courts will hold you personally liable for any damages exceeding your policy limits. A $100,000 liability limit represents the bare minimum for most recreational boats, but faster vessels or boats carrying multiple passengers should carry $300,000 or higher-the annual premium difference between these limits is modest (typically $50 to $100), yet the financial protection difference is enormous. Real-world scenarios on Georgia’s waterways prove that serious accidents generate claims far exceeding what underinsured boaters expect, with collisions, injuries, and property damage easily reaching $200,000 to $500,000 or more.

Contact North Point Insurance Group today to get a quote and ensure your boat liability coverage in Georgia reflects the real dangers you face on the water. Our local agents understand Georgia’s boating landscape and can help you select coverage limits that match your actual risk. We shop multiple carriers to find competitive pricing without sacrificing protection.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.